/CPU%20Chip.jpg)

Prominent investment bank Cantor Fitzgerald is very bullish on Applied Materials (AMAT) heading into its fiscal second-quarter results, which the company is slated to report today. Further, many other analysts are also upbeat on the name, Applied Materials' financial results nearly always beat analysts' average estimates in recent years, and semiconductor stocks, including AMAT, have a great deal of momentum at this time. Finally and importantly, the valuation of AMAT stock is reasonably low and attractive compared to many other names in the space.

In light of all of these points, AMAT appears to be worth buying ahead of its results, particularly for growth investors who are looking to increase their exposure to the semiconductor space amid the AI boom.

About AMAT

The company's systems are used to make semiconductors and “Applied leads the world in manufacturing semiconductors and display equipment," according to AMAT. The firm's products have also allowed chips to be enhanced amid the AI boom.

The shares have a trailing price-to-earnings ratio of 46x and a market capitalization of $342 billion.

Cantor Fitzgerald and Many of Its Peers Are Upbeat on AMAT

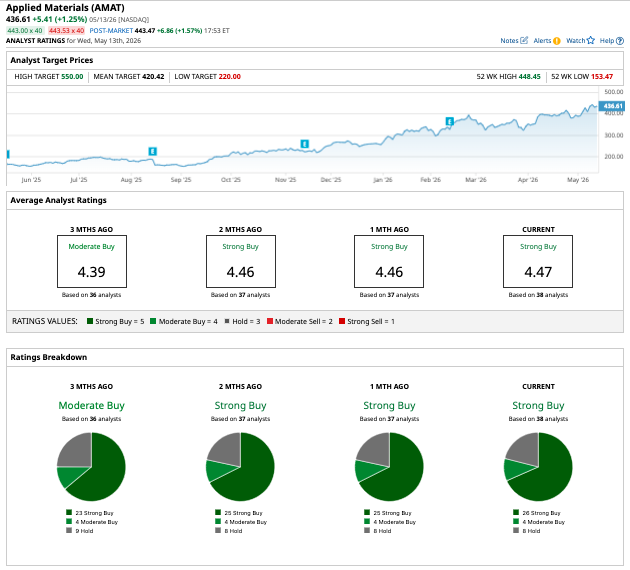

Predicting that Applied Materials would report stronger-than-expected financial results and raise its guidance, Cantor analyst C.J. Muse raised his price target on the shares to $550 from $500. Muse indicated that the company's customers have plans to purchase all of the products that it can provide “into 2028,” and he thinks that AMAT's 2026 earnings per share can reach $13.50, well above analysts' current average estimate of $12.13. The analyst expects AMAT to continue benefiting from strong sector trends “at least through” 2028, and he kept an “Overweight” rating on the shares.

Meanwhile, out of 38 analysts who cover the name, 26 have a “Strong Buy” on it and four rate it as a “Moderate Buy,” while only eight have a “Hold” rating on the shares. As a result, AMAT has a “Strong Buy” rating on Barchart.

AMAT Usually Beats the Average Estimates and Is Already Benefiting from Strong Momentum

The company's EPS totals have surpassed analysts' average estimates in its last nine earnings reports, and its revenue has beaten the mean estimate in eight of the last nine reports, including the last three quarterly results.

AMAT stock also has a great deal of positive momentum. As of the close on May 13, the shares had climbed 10.3% in the last month, 23% in the preceding three months, and 70% in 2026.

Amid the AI revolution, which is largely based on chips creating and maintaining AI, semiconductor stocks in general are on a big roll. As of the close on May 13, the PHLX Semiconductor Index ($SOX) had soared 70% in 2026.

And unsurprisingly, with the AI boom expected to continue for at least the next several years, Applied Materials' subsector, the semiconductor process equipment (SPE) space, is expected to grow rather quickly over the longer term. According to one estimate, the value of the global SPE space will expand from $102.4 million in 2025 to $156 million. That would represent a compound annual growth rate of 7.4%.

The Valuation of AMAT Is Relatively Low for the Semiconductor Space

Applied Materials is changing hands at a forward P/E ratio of 39.81x. That's much lower than many names in the sector, such as Intel (INTC) and AMD (AMD), whose forward P/E ratios are 205x and 76x, respectively.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.