/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Dell Technologies (DELL) has seen its stock almost double this year amid strong demand for artificial intelligence (AI) servers. The AI infrastructure boom has reached an inflection point with agentic AI gaining popularity. AI is no longer just for generating content; it can now drive outcomes.

Amid this, Dell’s AI-optimized servers, powered by Nvidia (NVDA) and Advanced Micro Devices (AMD) chips, have experienced explosive demand. On top of that, Dell’s rival, Super Micro (SMCI), is facing problems of its own, with one of the company’s co-founders being charged with smuggling Nvidia chips to China.

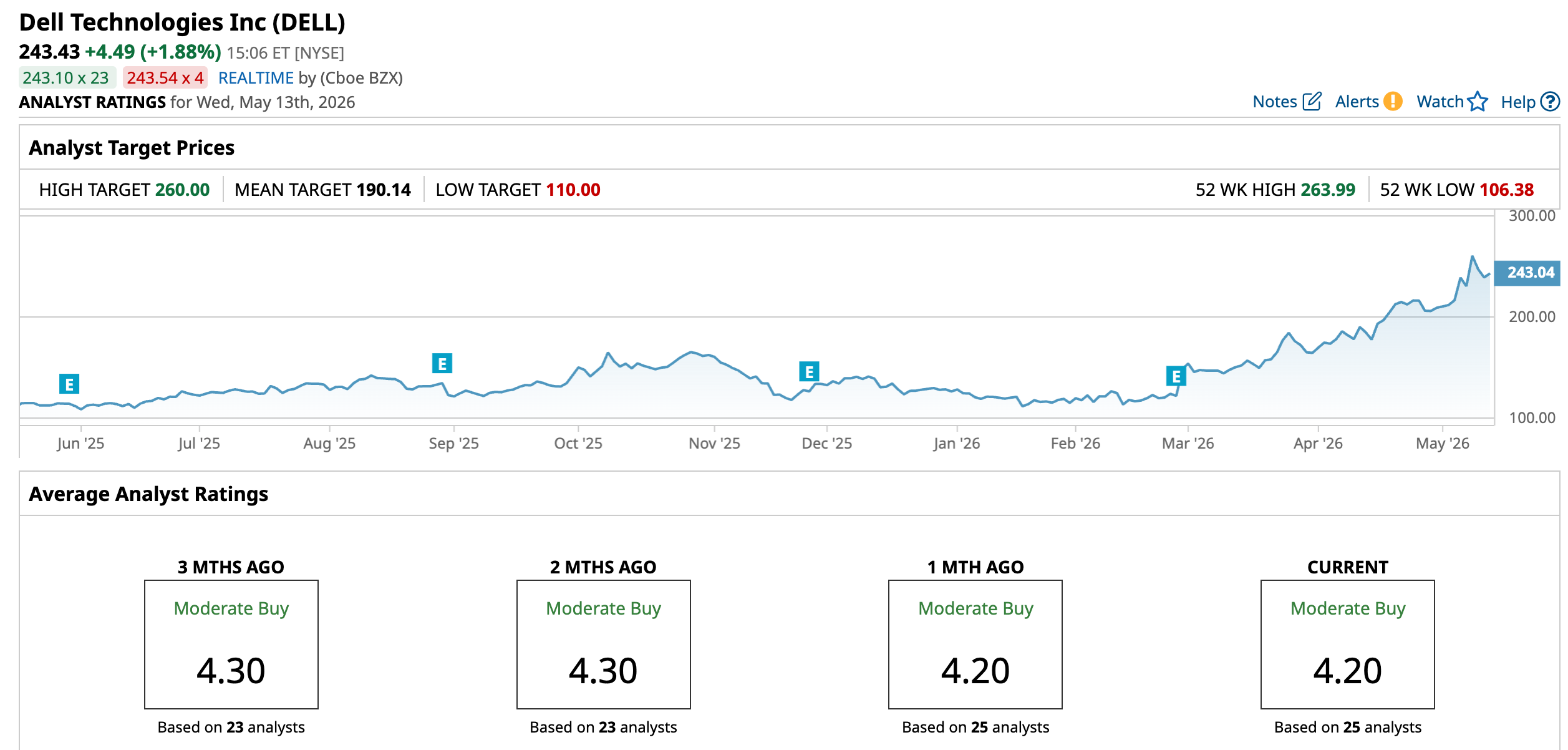

However, Dell’s stock dropped 5.2% intraday on May 11 and another 3.3% on May 12, as UBS analysts downgraded the stock from “Buy” to “Neutral.” Analyst David Vogt believes that accelerating server demand is already priced in by investors, potentially leading to a flattening of the stock’s trajectory. UBS raised its price target on Dell from $167 to $243, but the new target implies only a modest 1.7% upside from the last closing price.

However, a new catalyst might be on the horizon with Q1 earnings approaching. Hence, we take a closer look at Dell at this juncture.

About Dell Stock

What started as a dorm-room startup in the 1980s by Michael Dell has grown into a major multinational technology company, with a market capitalization of $154.3 billion. Headquartered in Round Rock, Texas, Dell operates in two distinct segments. First, the Client Solutions Group (CSG) offers desktops, notebooks, and peripherals, including XPS and Inspiron. The latest addition to its CSG portfolio is AI-enabled PCs with built-in neural processing units (NPUs) that support platforms like Copilot+ and AI inference.

Second, Dell’s Infrastructure Solutions Group (ISG) segment offers servers, storage and networking via PowerEdge. Dell has also struck partnerships to further its AI ambitions. Notable among them is the Dell AI Factory with Nvidia.

The explosive demand for AI servers amid rapid AI infrastructure buildouts has driven Dell’s stock to surge. Over the past 52 weeks, the stock has gained 126.39%, while it has been up 93.96% year-to-date. It reached a 52-week high of $263.99 on May 8, but is down 7.7% from that level.

Dell is currently trading at a cheaper valuation than its peers. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 18.46 times is lower than the industry average of 24.20 times.

Dell Crushes Q4 with AI Server Surge, Revenue Beats on Infrastructure Boom

Dell’s fourth-quarter for fiscal 2026 (quarter ended Jan. 30) results were better than expected, despite memory prices rising on the back of a shortage. The company’s net revenue increased 39% year-over-year (YOY) to a record $33.38 billion, which was better than the $31.73 billion that Wall Street analysts had expected.

The growth was primarily driven by the ISG segment, which grew 73% YOY to $19.60 billion, as revenue from AI-optimized servers climbed by a whopping 342% to $8.95 billion. The CSG segment has fallen short, as its net revenue grew only 14% YOY to $13.49 billion.

And this translated into profitability gains. Non-GAAP operating income grew 32% from the prior-year period to $3.54 billion. Non-GAAP EPS increased 45% to $3.89, surpassing the $3.53 that analysts had expected.

Fiscal 2026 as a whole was a record-breaking year for Dell. Revenue climbed 19% annually to a record $113.54 billion. The company closed more than $64 billion in AI-optimized server orders and shipped more than $25 billion. Strong execution drove record annual cash flow of $11.71 billion.

Dell Eyes AI Server Boom, Issued Robust FY27 Outlook

There’s greater visibility, as the company closed FY2026 with a record backlog of $43 billion. Eyeing a larger customer base amid the AI server boom, Dell projected robust 23% YOY growth in its FY2027 revenue (at the midpoint) to a range of $138 billion to $142 billion. AI-optimized server revenue is expected to reach roughly $50 billion, up 103% YOY. The company’s non-GAAP EPS is projected to grow to $12.90 at the midpoint, up 25%.

Wall Street analysts are robustly optimistic about Dell’s future earnings. For the current fiscal year, EPS is projected to surge 28.7% annually to $11.90, followed by a 12.4% growth to $13.37 in the next fiscal year. Moreover, analysts expect the company’s EPS to grow by 112.1% YOY to $2.99 for the first quarter of fiscal 2027 (to be reported on May 28, after the market closes).

What Do Analysts Think About Dell Stock?

Recently, analysts at Mizuho kept a bullish “Outperform” rating on the stock and raised the price target from $260 to $300. The analysts cited rising agentic AI workloads, which should create a sustainable demand for servers. However, for long-term investors, this raises the question of whether the upside is already priced in. Last month, Citi analysts also raised the price target from $180 to $235 while maintaining a “Buy” rating on Dell’s stock, citing strong order visibility driven by AI server momentum and improving storage execution. Analysts consider Dell's H2 2026 guidance appropriately cautious.

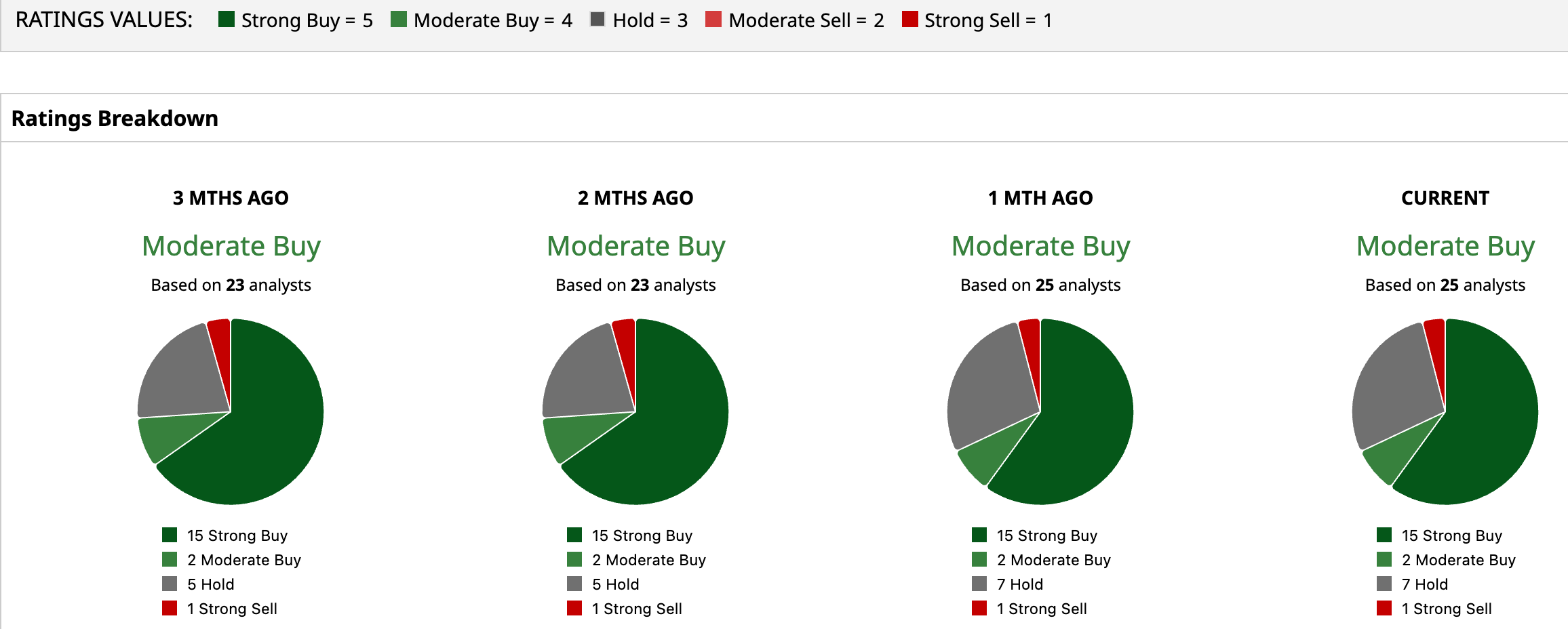

Dell Technologies remains a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 25 analysts rating the stock, 15 analysts have given it a “Strong Buy” rating, two analysts gave a “Moderate Buy,” while seven analysts are taking the middle-of-the-road approach with a “Hold” rating, and one analyst recommended “Strong Sell.” The consensus price target of $190.14 represents a 21.9% downside from current levels, while the Street-high price of $260 could see DELL going 6.8% higher from here.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Space/Rocket%20takes%20off%20by%20Alones%20via%20Shutterstock.jpg)