/Microchip%20Technology%2C%20Inc_%20HQ%20sign-by%20Michael%20Vi%20via%20Shutterstock.jpg)

Arizona-based Microchip Technology Incorporated (MCHP) is a leading semiconductor company that designs and manufactures embedded control solutions used across industrial, automotive, aerospace, communications, consumer electronics, and data center markets. With a market capitalization of $53.6 billion, the company is best known for its microcontrollers, analog chips, connectivity products, memory solutions, and embedded processors.

Shares of the semiconductor manufacturer have outperformed the broader market over the past year. MCHP stock has jumped 79% over the past 52 weeks and 55.4% on a year-to-date basis. In comparison, the S&P 500 Index ($SPX) has returned 31% over the past year and 8.3% in 2026.

Narrowing the focus, MCHP has also outperformed the State Street Technology Select Sector SPDR ETF (XLK), which rose 63.5% over the past 52 weeks and delivered 23.6% returns this year.

On May 7, Microchip Technology released its FY2026 Q4 earnings, and its shares dipped 1.3%. It posted revenue of $1.31 billion, up 35.1% year over year, beating Wall Street expectations. Non-GAAP earnings came in at $0.57 per share, well above analysts’ estimates. Non-GAAP gross margin expanded to 61.6%, supported by higher production volumes and improving factory utilization as customer inventories normalized.

For the fiscal year ending in March 2027, analysts expect MCHP to report a 84.5% year over year growth in adjusted EPS to $2.14. The company has a mixed earnings surprise history. It has surpassed and met the Street’s bottom-line estimates in three of the past four quarters, while missing on one occasion.

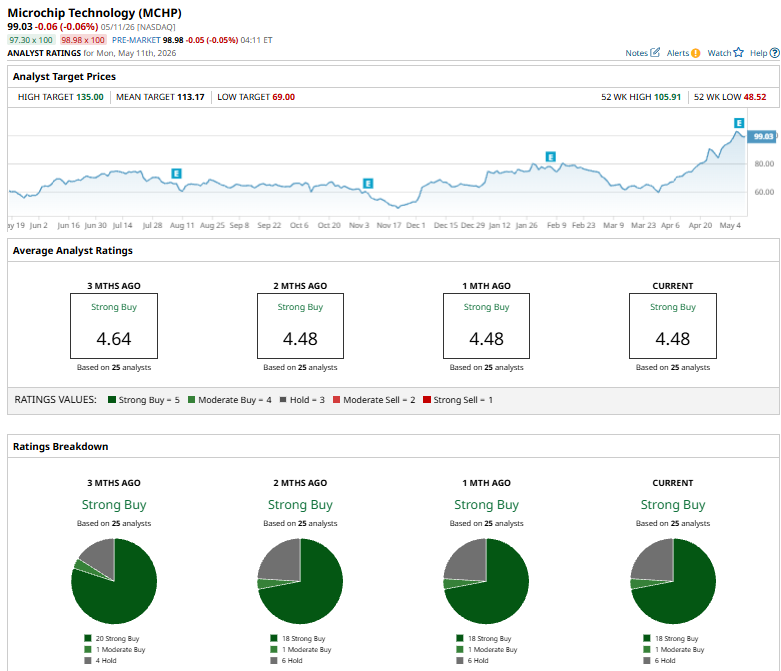

MCHP has a consensus “Strong Buy” rating overall. Of the 25 analysts covering the stock, opinions include 18 “Strong Buys,” one “Moderate Buy,” and six “Holds.”

This configuration is bearish than three months ago when the stock had 20 “Strong Buy” suggestions.

On May 11, Barclays raised its price target on Microchip Technology from $80 to $105 while maintaining an “Equal Weight” rating on the stock.

Its mean price target of $113.17 implies a premium of 14.3% from the prevailing market prices and the Street-high price target of $135 indicates an upswing potential of 36.3% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)