/Fidelity%20National%20Information%20Services%2C%20Inc_%20logo%20on%20phone-by%20IgorGolovniov%20via%20Shutterstock.jpg)

With a market cap of $24.4 billion, Fidelity National Information Services, Inc. (FIS) provides banking, payment, risk management, and capital market solutions to financial institutions, businesses, and developers worldwide. It operates through its Banking Solutions and Capital Market Solutions segments, offering innovative digital and financial services.

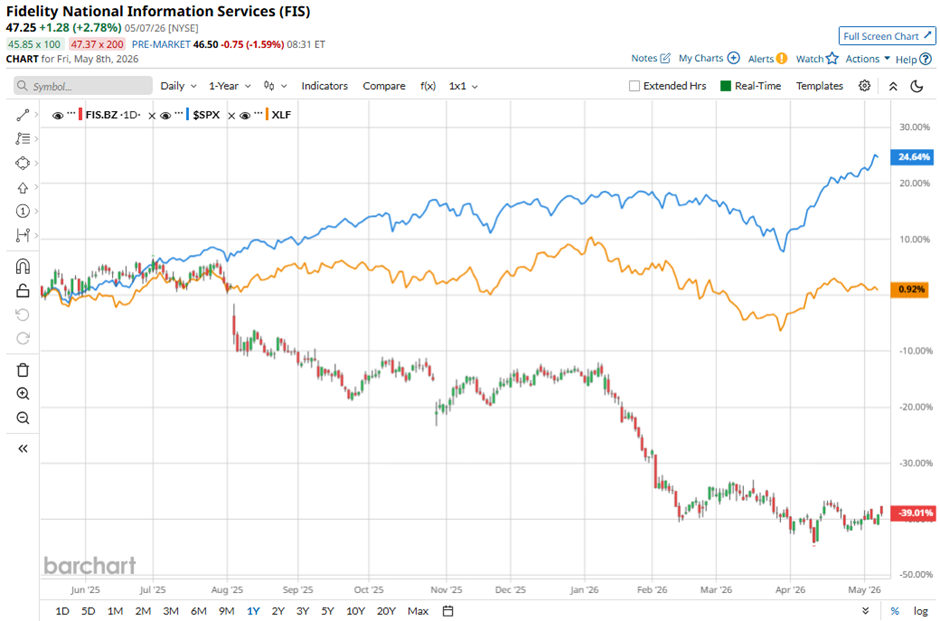

Shares of the Jacksonville, Florida-based company have lagged behind the broader market over the past 52 weeks. FIS stock has dropped 39.9% over this time frame, while the broader S&P 500 Index ($SPX) has returned 30.3%. Moreover, shares of the company are down 29.6% on a YTD basis, compared to SPX’s 7.2% gain.

Focusing more closely, shares of the financial technology company have underperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 3.6% rise over the past 52 weeks.

Shares of Fidelity National fell 6.7% on May 8 despite reporting stronger-than-expected Q1 2026 adjusted EPS of $1.36 and revenue rose 30% year-over-year to $3.29 billion, as investors reacted negatively to the company’s weaker forward guidance. Its full-year 2026 revenue forecast of $13.77 billion - $13.85 billion fell well below Wall Street expectations. The company also guided Q2 revenue to $3.37 billion - $3.39 billion and adjusted EPS to $1.45 - $1.49, both slightly below analyst estimates, which overshadowed strong operating performance including 36% adjusted EBITDA growth and a 111% jump in free cash flow to $474 million.

For the fiscal year ending in December 2026, analysts expect Fidelity National Information Services’ EPS to grow 9% year-over-year to $6.27. The company’s earnings surprise history is mixed. It beat or met the consensus estimates in three of the last four quarters while missing on another occasion.

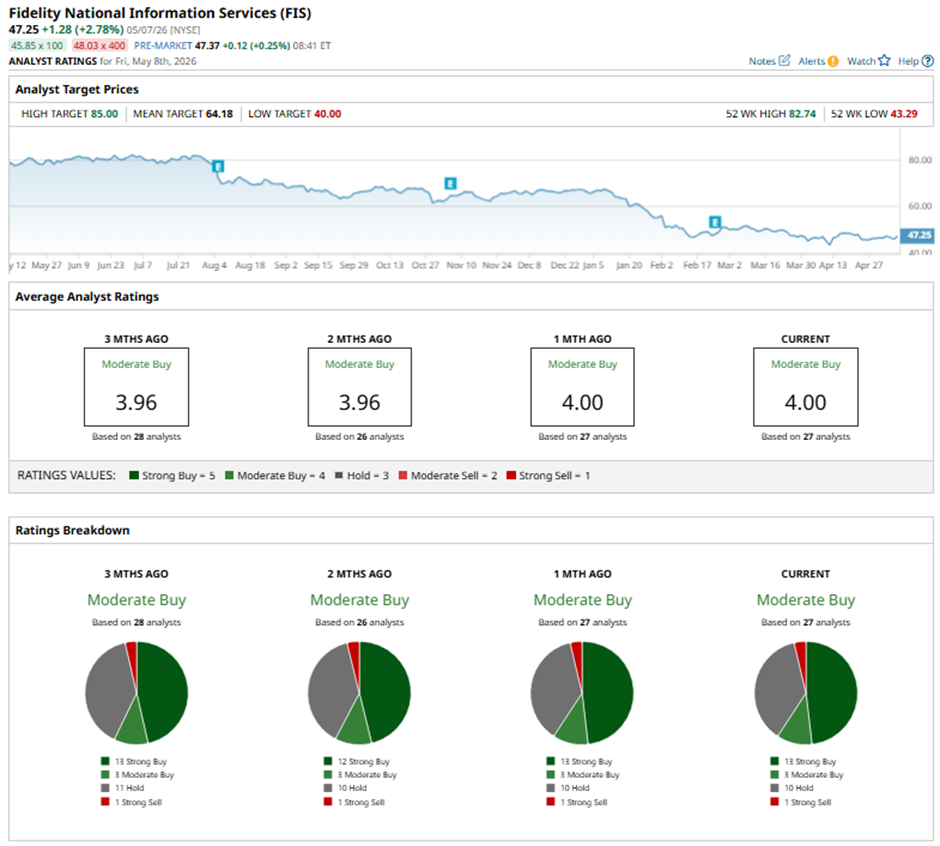

Among the 27 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, three “Moderate Buys,” 10 “Holds,” and one “Strong Sell.”

On May 6, Dan Dolev of Mizuho Securities reiterated a “Buy” rating on Fidelity National Information Services and maintained a price target of $83.

The mean price target of $64.18 represents a 35.8% premium to FIS’ current price levels. The Street-high price target of $85 suggests a 79.9% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)