/Computer%20memory%20by%20Zoomik%20via%20Shutterstock.jpg)

Imagine a company that owned stakes in another company whose shares have increased by more than 3,500% in the past year. Now, come back to reality and realize that they have divested their entire stake in that company, and as a token gesture, are increasing their dividend by 20%. It reeks of a rotten deal, right?

Well, what if their own company's shares are up 882.4% in the same period and they also have a vital role to play in the very-hot memory space in the AI buildout? Things look a bit rosier, don't they?

About Western Digital

Best known for owning the memory sensation Sandisk (SNDK), restricting Western Digital's (WDC) credentials to just that would be an injustice. Founded in 1970, it is a global leader in data storage technologies, primarily producing hard disk drives (HDDs) and storage systems for data centers, the cloud, and enterprise customers.

Valued at a market cap of $146.3 billion, the WDC stock is up 169% on a YTD basis. Notably, the company increased its quarterly dividend to $0.15 per share from $0.125 per share, a bump of 20%. The dividend will be on June 17 to shareholders of record on June 5.

But is this the only reason to add WDC stock to an investor's portfolio? Certainly not, and here's why.

Upbeat Q4

One of the compelling reasons to own WDC stock should be its most recent results for Q3 2026, marked by a beat on both revenue and earnings.

Revenues were up 45% from the prior year to $3.34 billion. Along with that, the company's gross margins crossed the 50% threshold for the first time. Coming in at 50.2%, it was a full 1040 bps up from the year-ago period's 39.8%. Meanwhile, earnings almost doubled to $2.72 per share in the same period, comfortably outpacing the consensus estimate of $2.40 per share. Notably, this was the fifth consecutive quarter of earnings beat from the company.

For Q4 2026, Western Digital has forecasted revenues and earnings to be $3.65 billion and $3.25 per share, implying year-over-year (YoY) growth rates of 39.8% and 95.6%, respectively. However, both are slightly lower than the Street expectations. While Street forecasts for revenues in Q4 are $3.68 billion, EPS expectations are for $3.27.

Coming back to Q3 again, net cash from operating activities jumped to $1.1 billion from $508 million in the prior year, as the company closed the quarter with a cash balance of $2.05 billion. Short-term debt on the company's books was lower at $1.58 billion.

Yet, the share price rally has come at a cost, in the form of the stock's valuations. WDC stock is trading at a forward P/E, P/S, and P/CF of 43.50, 11.38, and 46.72, all below the sector medians of 24.05, 3.22, and 18.41, respectively.

HDD Edge

Despite such lofty valuations and heightened competition from the likes of Sandisk, Micron (MU), and Seagate (STX), what is leading to more demand for WDC stock? Well, it's primarily because of its HDDs.

The simplest answer to why hyperscalers keep buying HDDs at scale comes down to one metric that never lies in the data center world: cost per terabyte. Between Q2 2025 and Q1 2026, the price gap between enterprise SSDs and HDDs exploded. A 30TB TLC enterprise SSD that cost roughly $3,062 in Q2 2025 climbed to nearly $11,000 by Q1 2026, a 257% jump, while HDD pricing rose only about 35% in the same period. The cost differential between SSD and HDD capacity went from 6.2x to a staggering 16.4x. For a hyperscaler storing hundreds of exabytes, that kind of cost asymmetry is simply not manageable at scale.

But where do HDDs score over DRAM and NAND, the two bellwethers of the AI memory cycle? Well, DRAM, while extraordinarily fast, serves an entirely different purpose in the storage hierarchy—it is volatile, meaning data disappears when power is cut, and it costs multiples more per gigabyte than even NAND. It is the right tool for active computation, not for storing the cold or warm data that constitutes the overwhelming majority of what actually sits in a hyperscale data center.

On the other hand, NAND's endurance limitations are also a real concern for cold archival workloads, where HDDs have decades of proven reliability. NAND flash costs track bits per wafer while HDD costs track areal density per platter, and since both technologies are advancing at similar rates, the total cost of ownership gap is more structural rather than cyclical. Thus, for hyperscalers drowning in massive AI capex, HDDs provide a relatively cheaper way to address their memory needs.

Further, Western Digital's market position in the HDD market gives it another edge. Together with Seagate, WDC controls over 80% of the global HDD market. And WDC's nearline HDD market share is estimated at around 42%, with the company's 32TB and 40TB UltraSMR drives described as the industry standard for hyperscale warm storage. UltraSMR overlaps data tracks like roof shingles to increase capacity by up to 20% without increasing physical drive size, which is a meaningful efficiency gain when customers are procuring at a petabyte scale. OptiNAND, another WDC innovation, embeds flash storage inside the hard drive to enhance the performance and reliability of the magnetic recording process itself.

And what WDC is coming up with is genuinely ambitious. WDC has begun sampling 50TB+ drives using HAMR, with a stated goal of reaching 100TB per drive by 2029. HAMR shipments are forecast to grow at a 16.98% CAGR through 2031 as both WDC and Seagate move toward 50TB-plus capacity milestones, though WDC enters that race with better supply chain relationships and a manufacturing approach that has already proven it can ramp reliably. The company is also sold out of HDD capacity for 2026, which reflects the depth and duration of the long-term agreements it has signed with hyperscalers, effectively locking in revenue visibility that most hardware companies aspire to.

Analyst Opinion of WDC Stock

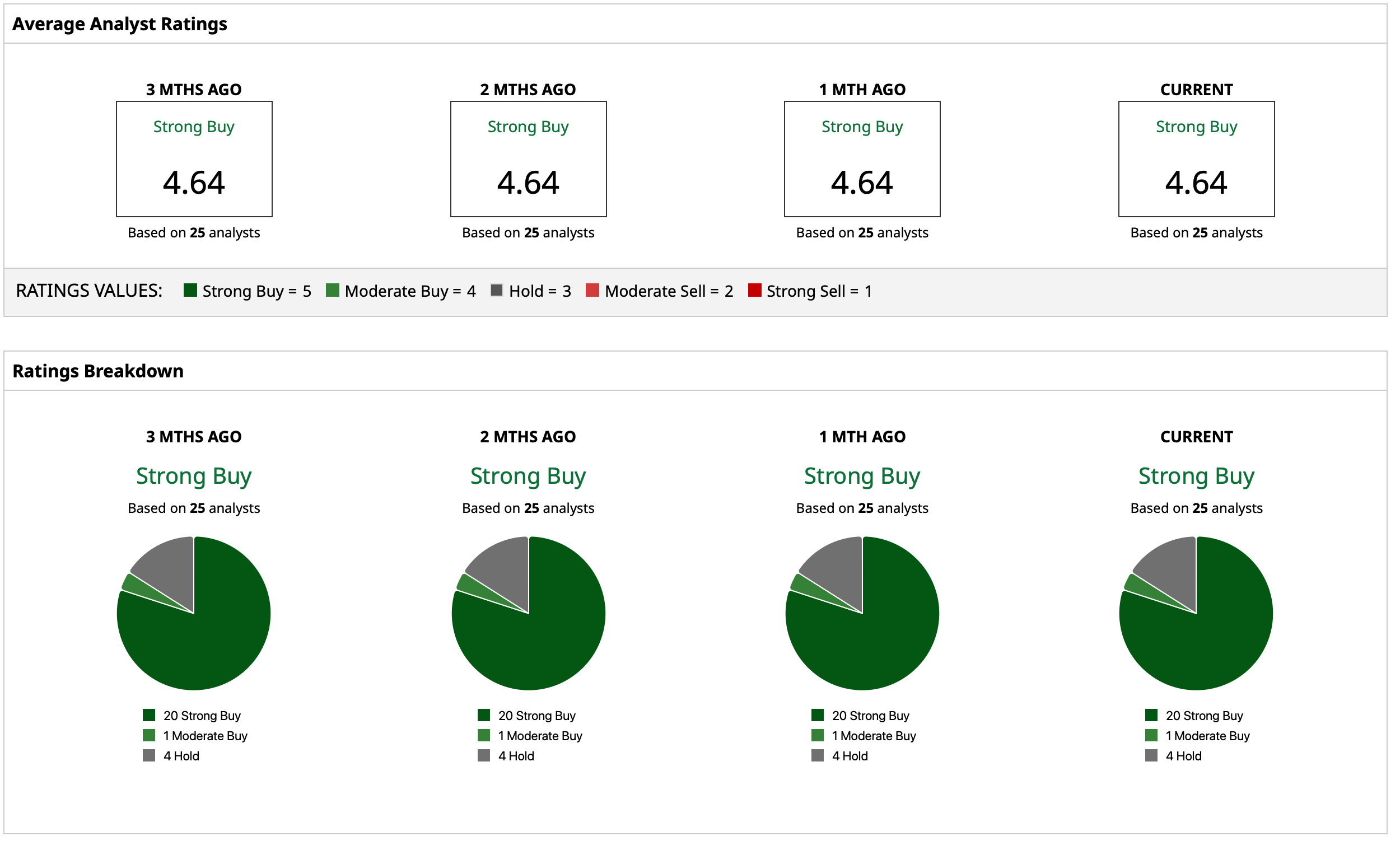

Thus, analysts remain bullish about WDC stock, attributing to it a consensus “Strong Buy” rating. While the mean target price of $476.59 gives only about a 3% upside, the high target price of $540 denotes an upside potential of about 17% from current levels. Out of 25 analysts covering the stock, 20 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)