Valued at $210.3 billion by market cap, T-Mobile US, Inc. (TMUS) is one of the largest wireless telecommunications companies in the United States, providing mobile phone, broadband, and wireless communication services to consumers and businesses. Headquartered in Bellevue, Washington, the company operates a nationwide 4G LTE and 5G network and serves tens of millions of subscribers across the country.

Shares of TMUS have underperformed the broader market over the past year. TMUS has declined 23.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31.4%. In 2026, TMUS stock is down 4.9%, compared to the SPX’s 7.6% rise on a YTD basis.

Narrowing the focus, TMUS has also trailed the State Street Communication Services Select Sector SPDR ETF (XLC). The exchange-traded fund has gained about 20.2% over the past year and has dipped marginally on a YTD basis.

On Apr. 28, T-Mobile announced its FY2026 Q1 earnings, and its shares rose 2.2%. Total revenue climbed 10.6% year over year to $23.11 billion, fueled by an 11.3% increase in service revenue and a 15% surge in postpaid service revenue. The company also added 217,000 postpaid accounts, marking 6% annual growth and underscoring continued customer momentum. However, diluted EPS declined 12% year over year to $2.27.

For the current fiscal year, ending in December 2026, analysts expect TMUS’ EPS to grow 4.6% to $10.63 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

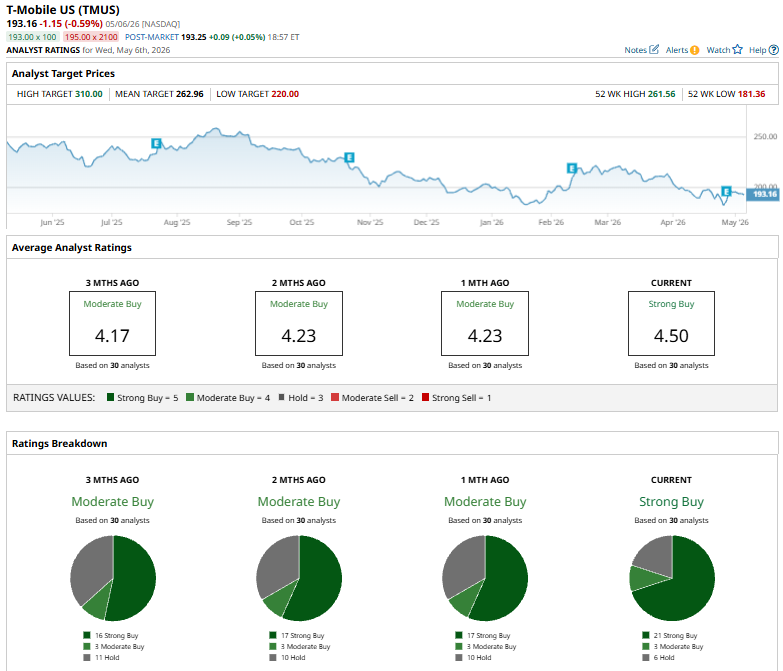

Among the 30 analysts covering TMUS stock, the consensus is a “Moderate Buy.” That’s based on 21 “Strong Buy” ratings, three “Moderate Buys,” and six “Holds.”

This configuration is less bearish than one month ago, with 17 analysts suggesting a “Strong Buy.”

On Apr. 29, JPMorgan lowered its price target on T-Mobile to $275 from $300 but maintained an “Overweight” rating on the stock. The firm highlighted the company’s strong Q1 performance, particularly better-than-expected postpaid account net additions, and said current share levels offer an attractive valuation and a compelling entry point for investors.

The mean price target of $262.96 represents a 36.1% premium to TMUS’ current price levels. The Street-high price target of $310 suggests an ambitious upside potential of 60.5%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)