/Baxter%20International%20Inc_%20logo%20and%20chart-by%20IgorGolovniov%20via%20Shutterstock.jpg)

Deerfield, Illinois-based Baxter International Inc. (BAX) provides a broad portfolio of essential healthcare products used in hospitals, clinics, and patient homes. Valued at a market cap of $8.9 billion, the company continues to leverage its massive global footprint and "Fab-Right" localized manufacturing strategy to drive digital health innovation, specifically through AI-driven predictive monitoring and autonomous infusion technologies.

This healthcare company has notably underperformed the broader market over the past 52 weeks. Shares of BAX have declined 45.9% over this time frame, while the broader S&P 500 Index ($SPX) has gained 29%. Moreover, on a YTD basis, the stock is down 13%, compared to SPX’s 5.6% rise.

Looking closer, BAX has also lagged the State Street Health Care Select Sector SPDR ETF (XLV), which gained 4.5% over the past 52 weeks and declined 6.5% on a YTD basis.

On Apr. 30, shares of BAX surged 4% after its better-than-expected Q1 earnings release. The company reported revenue of $2.7 billion, up 2.9% year-over-year, driven by solid growth in international markets that was partially offset by weaker U.S. sales. Its topline figure exceeded consensus estimates by 3.8%. Meanwhile, its adjusted EPS came in at $0.36, down 34.5% from the prior-year quarter, but still ahead of analyst expectations of $0.31.

For the current fiscal year, ending in December, analysts expect BAX’s EPS to decline 15.9% year over year to $1.91. The company’s earnings surprise history is mixed. It topped the consensus estimates in two of the last four quarters, while missing on two other occasions.

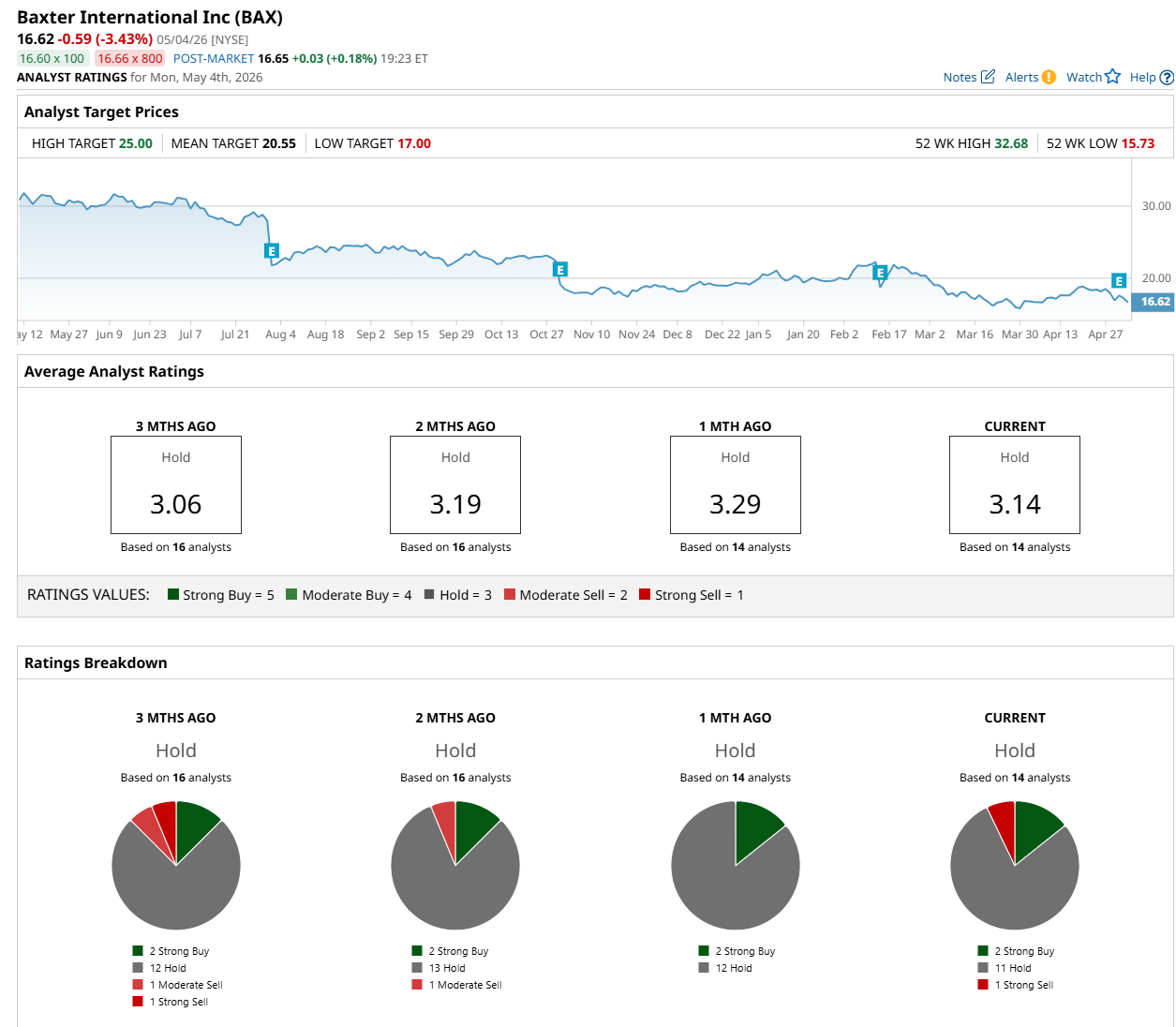

Among the 14 analysts covering the stock, the consensus rating is a "Hold,” which is based on two “Strong Buy,” 11 “Hold,” and one “Strong Sell” rating.

The configuration is more bearish than a month ago, with no analyst suggesting a "Strong Sell” rating.

On May 4, Barclays PLC (BCS) maintained an “Overweight” rating on BAX and raised its price target to $27, the Street-high price target, indicating a 62.5% potential upside from the current price levels.

The mean price target of $20.55 suggests a 23.6% premium to its current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)