With a market cap of $59.3 billion, Realty Income Corporation (O) is a publicly traded real estate investment trust (REIT) that owns income-generating commercial properties. The San Diego, California-based company operates a vast portfolio of freestanding properties across the U.S. and Europe, leased primarily to stable, high-quality tenants in sectors like retail, industrial, and logistics.

O stock has surged 10.3% over the past year, while the broader S&P 500 Index ($SPX) has increased 28.3%. However, O has shown solid momentum in 2026, rising 12.3%, outpacing the benchmark’s 4.2% climb.

The stock has surpassed the State Street Real Estate Select Sector SPDR Fund’s (XLRE) 6.2% rally over the past 52 weeks and 8.2% year-to-date rise.

On Apr. 14, Realty Income shares rose marginally after the company announced its 670th consecutive monthly dividend, reinforcing its long-standing income track record. The company declared a dividend of $0.2705 per share (annualized to $3.246 per share), payable on May 15, 2026, to shareholders of record as of April 30, 2026.

For FY2026, which ends in December, analysts expect Realty Income’s AFFO per share to grow 4% year-over-year to $4.45. The company’s earnings surprise history is mixed. It beat or met the consensus estimates in three of the last four quarters while missing on another occasion.

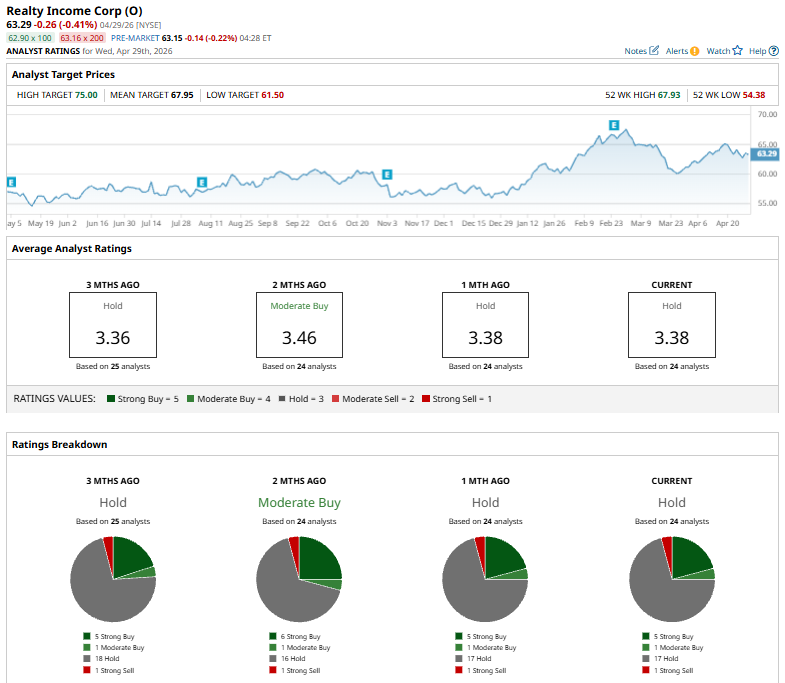

Among the 24 analysts covering the stock, the consensus rating is a “Hold.” That’s based on five “Strong Buy” ratings, one “Moderate Buy,” 17 “Holds,” and one “Strong Sell.”

This configuration is bearish than two months ago when the stock had an overall “Moderate Buy” rating.

On April 21, Richard Hightower of Barclays raised his price target on Realty Income Corporation to $68 from $65, while maintaining an “Equal-Weight” rating. In his note, Hightower characterized the current operating backdrop as a “Goldilocks” environment for the group, supportive but not overheated. Barclays expects this setup to drive increased capital markets activity, with more equity issuance announcements and higher acquisition guidance across net lease REITs.

Its mean price target of $67.95 represents a premium of 7.4% from the current market prices. The Street-high price target of $75 implies a potential upside of 18.5% from the current price.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)