Energy investors have spent years watching OPEC and OPEC+ act like the market’s unofficial thermostat—cutting production when crude prices fell too far and opening the taps when prices overheated. That balancing act just took a hit.

The United Arab Emirates’ surprise decision to quit OPEC/OPEC+ rattled oil markets because it raises a bigger question: what happens if the cartel starts losing control of supply discipline altogether?

Crude traders answered quickly. West Texas Intermediate crude climbed above $100 per barrel following the announcement as investors priced in greater uncertainty around future production coordination. That matters because volatility—not just high prices—is where certain oil producers thrive.

And one company stands out as an immediate beneficiary: Diamondback Energy (FANG).

Unlike global supermajors juggling refining, chemicals, and overseas politics, Diamondback is a pure-play Permian Basin producer with one primary job—pump low-cost oil profitably. In a world where oil spikes suddenly and supply discipline weakens, that simplicity becomes an advantage.

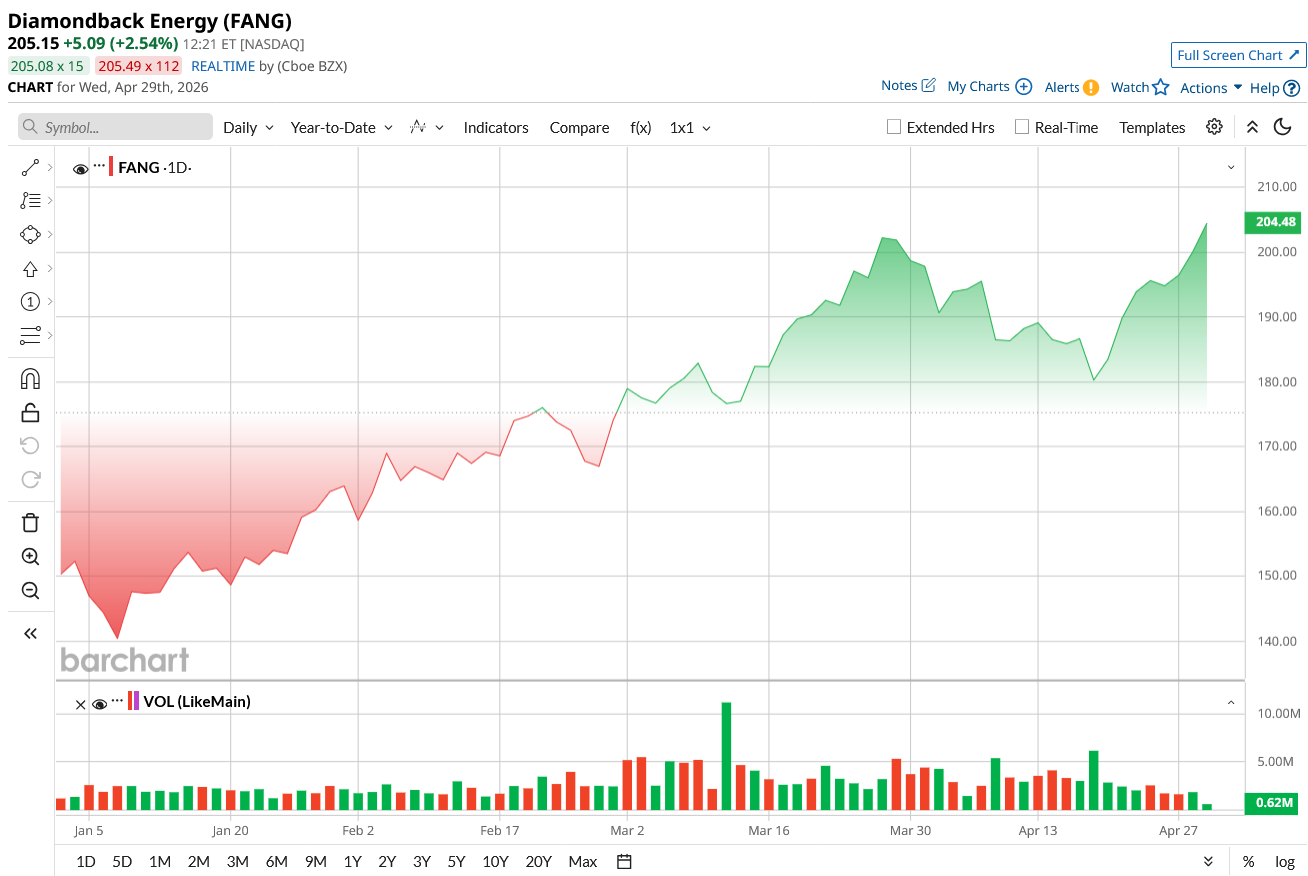

FANG Is Already Beating the Market

Before the UAE announcement, Diamondback was already outperforming.

According to Barchart’s performance data, FANG stock has returned 36% year-to-date (YTD), compared to roughly 4% for the S&P 500 ($SPX) over the same stretch.

That outperformance tells investors something important: the market was already rewarding companies with direct leverage to rising crude prices before this geopolitical development arrived.

Here’s how Diamondback stacks up:

The reason it has kept pace is straightforward. Diamondback has heavier direct exposure to crude prices than integrated oil giants. When WTI rises sharply, cash flow expansion tends to show up faster in FANG’s results.

That’s because higher oil prices flow through to the bottom line more directly. And unlike some smaller shale drillers, Diamondback enters this environment from a position of strength. The company generated billions in free cash flow over the past year, maintained disciplined capital spending, and continued returning capital to shareholders through dividends and buybacks.

Granted, higher oil prices help almost every producer. But not every producer can capitalize equally.

Why Diamondback Could Benefit More Than Its Rivals

The UAE’s departure matters because it weakens the perception of coordinated supply management. If OPEC members begin prioritizing individual production goals over cartel quotas, oil markets could become more volatile for years.

Surprisingly, that environment tends to favor efficient U.S. shale operators.

Diamondback’s Permian acreage remains among the lowest-cost production regions in North America. That gives the company flexibility many rivals lack. It can remain profitable at lower crude prices while also generating outsized cash flow during spikes like the current move above $100 oil.

FANG Offers a Competitive Valuation

Diamondback trades at a forward earnings multiple below many broader market sectors despite its strong cash generation and commodity leverage. Meanwhile, its shareholder returns remain competitive through both variable dividends and repurchase activity.

Here’s what the numbers tell us:

| Company | Forward P/E | Dividend Yield | Primary Strength |

| Diamondback Energy | 11.7x | 2.% | Low-cost shale exposure |

| Exxon Mobil | 15.x | 2.7% | Integrated operations |

| Chevron | 14.8x | 3.7% | Global production scale |

Regardless of how you look at it, FANG offers sharper torque to rising crude prices than its larger peers.

That comes with risk, of course. If oil prices retreat sharply or global demand weakens, Diamondback’s earnings can contract faster than those of diversified majors. But today’s setup is not centered on weak demand—it is centered on supply uncertainty.

And supply uncertainty is usually bullish for shale cash flows.

What Analysts Think About FANG

Wall Street remains constructive on Diamondback despite the stock’s recent rally.

According to Barchart's analyst ratings data, FANG currently carries a “Strong Buy” consensus rating based on 32 analyst opinions. There are 24 "Strong Buy" ratings, three "Moderate Buy," ratings and five "Hold" ratings.

The average analyst mean price target sits near $220.45 per share, while the high target reaches roughly $266 and the low target stands near $174.

Based on its current trading levels, $205.15, that implies FANG stock is:

- Roughly 7% upside to the consensus target.

- More than 30% upside to the highest target.

- About 15% downside to the low target.

That spread reflects the reality of commodity investing. Oil stocks are rarely valued in a straight line because crude prices themselves are volatile.

Still, analysts believe Diamondback remains positioned to benefit if elevated oil prices persist through 2026.

Bottom Line

In short, the UAE’s decision to leave OPEC/OPEC+ may prove to be one of the most important oil market developments in years because it weakens the coordinated supply structure investors and producers have relied on for decades.

For Diamondback Energy, that disruption could become an opportunity.

The company combines low-cost Permian production, strong free cash flow generation, and direct leverage to rising crude prices at a moment when WTI has already climbed above $100 per barrel. When all is said and done, that combination gives FANG sharper upside potential than many larger integrated rivals if oil volatility remains elevated.

That said, investors should remember this remains a commodity-driven business. If crude prices reverse, sentiment can shift quickly.

But in today’s market—where supply uncertainty suddenly matters more than demand softness—Diamondback Energy looks positioned to benefit first.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)