/RTX%20Corp%20website%20on%20phone%20and%20logo-by%20T_Schneider%20via%20Shutterstock.jpg)

With a market cap of $233.5 billion, RTX Corporation (RTX) is a prominent aerospace and defense company serving commercial, military, and government customers. The Virginia-based company operates through its three operating segments: Collins Aerospace, Pratt & Whitney, and Raytheon.

Shares of the defense titan have significantly outperformed the broader market over the past 52 weeks. RTX stock has jumped 40.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 29.1%. However, RTX shares are down 4.2% on a YTD basis, compared to SPX’s 4.3% rise.

Focusing more closely, shares of the aerospace and defense company have outpaced the State Street Industrial Select Sector SPDR ETF’s (XLI) 32.1% return over the past 52 weeks.

On Apr. 21, RTX delivered FY2026 Q1 earnings. Its sales improved 9% year over year to about $22.1 billion, driven by broad-based growth across all three business segments. It posted an adjusted EPS of $1.78, up 21% year over year, supported by margin expansion and higher segment operating profit. The company also generated an operating cash flow of roughly $1.9 billion and reported a robust backlog of $271 billion, underscoring strong demand across both commercial aerospace and defense markets. Despite solid results, its shares dipped 4.4% amid risks tied to Pratt & Whitney’s GTF engine issues, particularly aircraft-on-ground concerns, ongoing supply chain constraints and cost pressures across the aerospace sector.

For the fiscal year ending in December 2026, analysts expect RTX’s adjusted EPS to grow 9.5% year over year to $6.89. The company's earnings surprise history is promising. It topped the consensus estimates in the last four quarters.

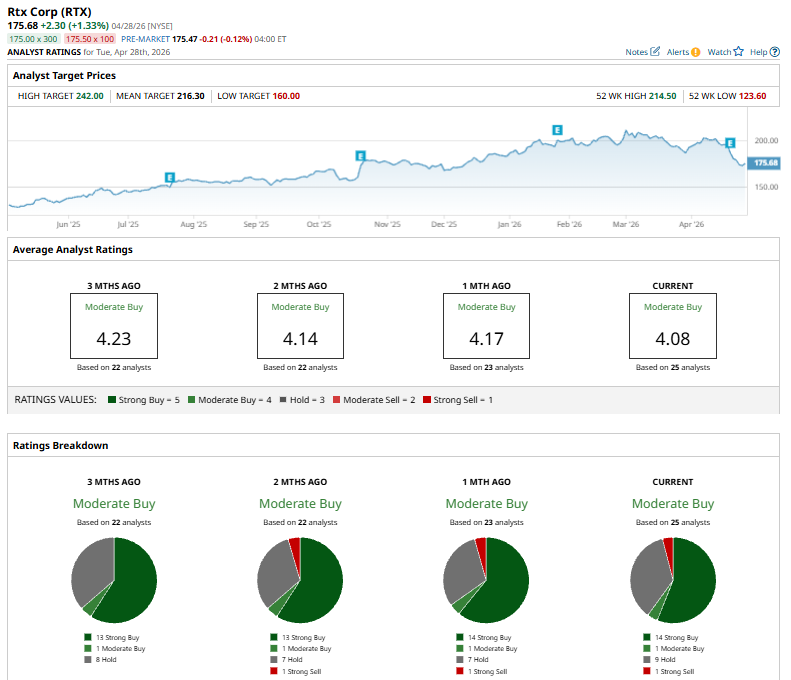

Among the 25 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 14 “Strong Buy” ratings, one “Moderate Buy,” nine “Holds,” and one “Strong Sell.”

The current configuration is bullish than two months ago when the stock had 13 “Strong Buy” suggestions.

On Apr. 22, UBS lowered its price target on RTX Corporation to $199 from $209 while maintaining a “Neutral” rating. The firm noted that RTX delivered a third consecutive quarter of EBIT beats across all segments, underscoring strong execution across its core businesses.

Its mean price target of $216.30 implies a premium of 23.1% from the current market prices. The Street-high price target of $242 suggests a 37.8% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)