With a market cap of $20.8 billion, Snap-on Incorporated (SNA) is a global leader in manufacturing and marketing tools, equipment, diagnostics, repair information, and systems solutions for professional users across a wide range of industries. It offers tools, diagnostics, shop equipment, engineered solutions, and financing programs, serving industries such as automotive, aerospace, agriculture, construction, government, and power generation.

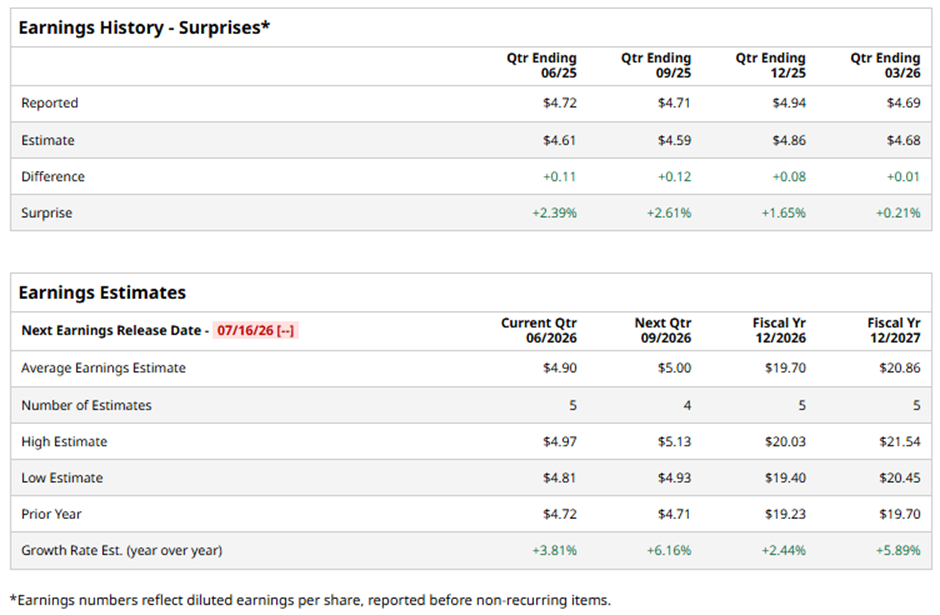

The Kenosha, Wisconsin-based company is expected to announce its fiscal Q2 2026 results soon. Ahead of this event, analysts forecast Snap-on to report an EPS of $4.90, up 3.8% from $4.72 in the year-ago quarter. It has surpassed Wall Street's earnings estimates in the last four quarters.

For fiscal 2026, analysts predict the tool and diagnostic equipment maker to report an EPS of $19.70, a rise of 2.4% from $19.23 in fiscal 2025. Moreover, EPS is anticipated to increase 5.9% year-over-year to $20.86 in fiscal 2027.

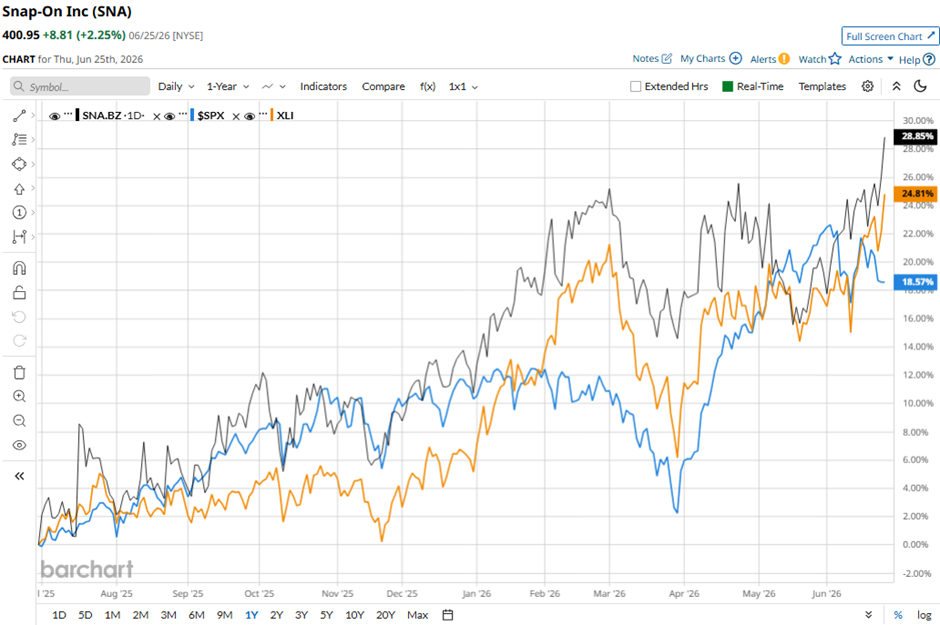

Shares of Snap-on have soared 30.5% over the past 52 weeks, outperforming both the S&P 500 Index's ($SPX) 20.8% gain and the State Street Industrial Select Sector SPDR ETF's (XLI) 28.1% return over the same period.

Shares of Snap-on rose 2.2% on Apr. 23 after the company reported stronger-than-expected Q1 2026 results, with net sales increasing 5.8% year-over-year to $1.21 billion, including 3.4% organic sales growth, while EPS rose to $4.69. Investors were encouraged by robust performance in the Commercial & Industrial Group, where sales climbed 10.8% to $381 million driven by critical industries and specialty torque demand, and by the Snap-on Tools Group, where sales increased 5% to $486 million and operating margin expanded 160 basis points to 21.6%.

The stock also benefited from management’s optimistic outlook, highlighting improving momentum in U.S. tools activity, resilience across key markets despite global uncertainty, and continued investment in growth opportunities across automotive repair and critical industries.

Analysts' consensus view on SNA stock is moderately optimistic, with a "Moderate Buy" rating overall. Among 11 analysts covering the stock, four suggest a "Strong Buy," one gives a "Moderate Buy," five recommend a "Hold," and one has a "Moderate Sell." As of writing, it is trading above the average analyst price target of $400.83.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)