/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Intel (INTC) is not the same stock it was a year ago. The company once looked like a symbol of missed chances and manufacturing delays. Now, it sits at the center of the AI infrastructure boom, with investors betting that its comeback story still has room to run.

That is why a recent comment from KKM Financial CEO Jeff Kilburg is getting so much attention. Even after Intel has surged sharply, Kilburg said there is still “no reason to take profits.” For a stock that has already delivered a huge run, that kind of call stands out. It also shows just how divided Wall Street remains on whether Intel has already priced in the good news.

Intel’s Massive Run Is Rewriting the Narrative

Intel has become one of the most talked-about names in semiconductors this year. The company is no longer being judged only as a legacy chipmaker. Investors are now looking at it as a possible winner in AI servers, advanced manufacturing, and foundry services.

Intel stock keeps hitting new highs after the blowout quarterly earnings, which pushed the stock more than 28% in a single session. That makes Intel shares up 297% over the past 12 months and roughly 120.5% year-to-date (YTD). Intel’s rally is driven by plenty of catalysts, such as the U.S. government backing, a major AI partnership with Nvidia (NVDA), expanding ties with Alphabet (GOOG) (GOOGL), a breakthrough Tesla (TSLA) foundry deal, and strong earnings showing surging server CPU demand.

After the bull run, Intel is no longer cheap. The stock trades at an Enterprise value-to-sales (TTM) multiple of 8.42 times, which is more than double the sector median. Its forward price-to-earnings ratio is 79.04 times, far above the semiconductor group average of 23.86 times.

At the same time, the market is clearly expecting a much stronger future. Intel’s long-term forward earnings-per-share growth estimate is in triple digits, compared with a sector median near 16%. In other words, investors are paying for a major earnings rebound, not for the past.

Intel’s Business Is Still Large, But Growth Is Improving

Intel’s first-quarter 2026 report gave investors more reasons to stay interested. Revenue came in at $13.58 billion, up 7.2% from a year earlier and about $1.4 billion above management’s own January outlook.

The strongest performance came from Data Center and AI, which generated $5.05 billion in revenue, up 22% year-over-year (YOY). Client Computing Group brought in $7.73 billion, a 1% increase. Intel Foundry Services posted $5.42 billion in revenue, up 16% from a year ago.

Profitability also improved. EPS came in at $0.17, well ahead of the $0.13 posted a year earlier and above the penny that many analysts had expected.

There were still some rough edges. Adjusted free cash flow came in at -$2 billion as Intel kept spending heavily on manufacturing capacity. But the company ended the quarter with about $32.8 billion in cash and equivalents, which gives it plenty of room to keep funding its turnaround.

CEO Lip-Bu Tan said demand is still outrunning supply, especially for Xeon server CPUs. That suggests the business is not just getting a one-time boost but is seeing broad, ongoing demand. This is a strong signal that Intel’s core businesses are seeing sustained momentum rather than a short-lived spike. The most important part of the Intel story are next steps.

Management Is Pushing a Real Turnaround Plan

The company guided second-quarter revenue to a range of $13.8 billion to $14.8 billion and EPS to $0.20. Both numbers came in above analyst expectations.

Beyond that, Intel’s foundry ambitions are starting to gain credibility. Tesla recently announced plans to use Intel’s next-generation 14A manufacturing process for its TeraFab AI chip project in Austin, Texas. Also, Intel deepened its collaboration with Google, further tying its future to AI infrastructure.

For investors, that matters because it suggests Intel is moving from a turnaround narrative to a broader strategic role in next-generation computing.

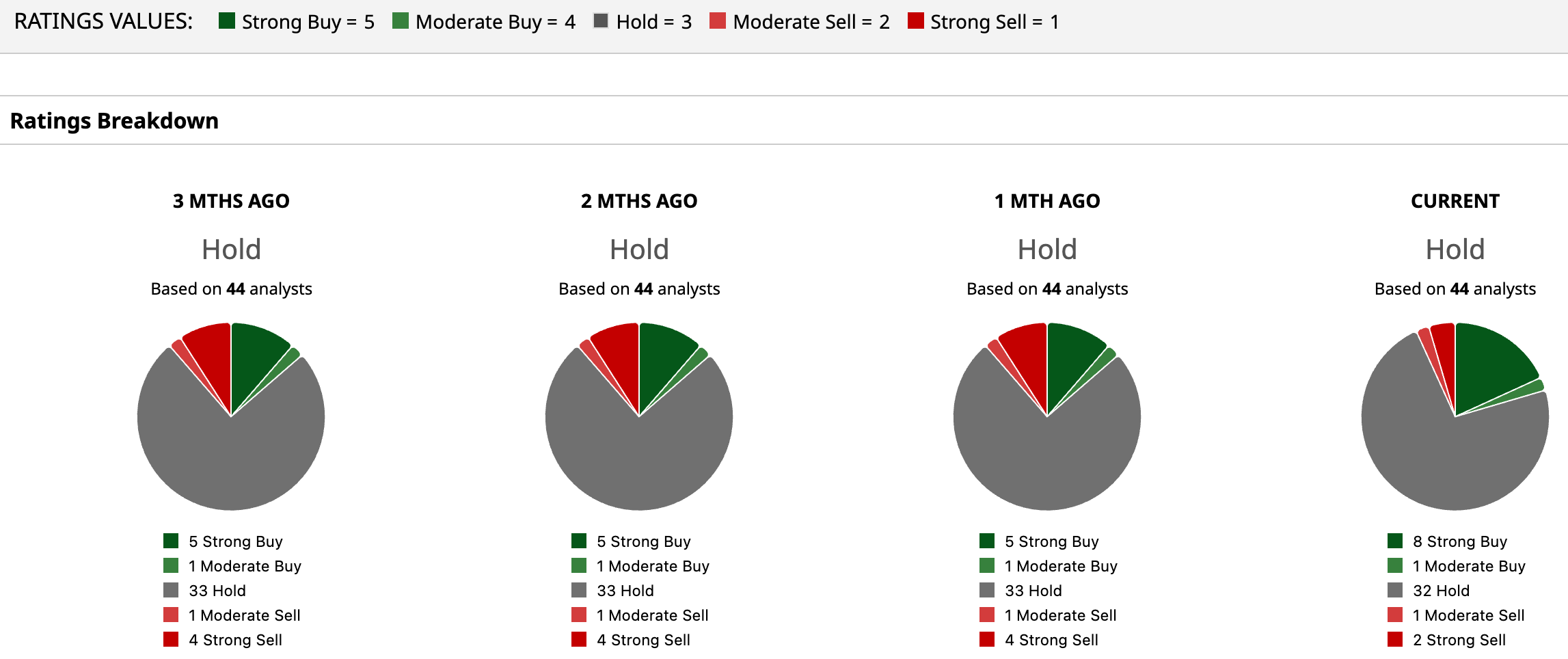

What Do Analysts Think of INTC Stock?

After the blowout earnings, several analysts have rushed to raise Intel Price targets. For example, Evercore analyst Mark Lipacis upgraded the stock to “Outperform” and raised his price target to a Street-high $111 from $45, saying the market may be underestimating Intel’s earnings power a few years out. Citi’s Atif Malik also upgraded the stock to “Buy” and set a $95 target, citing stronger AI-driven CPU demand. Roth Capital followed with a “Buy” rating and a $100 target.

Not everyone is as enthusiastic. Barclays lifted its price target to $65 but kept an “Equal Weight” rating, arguing the stock already reflects a lot of the turnaround story.

According to the latest data, the consensus rating remains “Hold," with 44 analysts reporting.

So, for now, Intel is one of the market’s most debated names. The rally has been huge, but so has the shift in fundamentals. That is why Kilburg’s “no reason to take profits” comment is getting so much attention. The bulls think the story is still early. The skeptics think the easy money has already been made.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)