/Apple%20Inc%20Tim%20Cook-by%20John%20Gress%20Media%20Inc%20via%20Shutterstock.jpg)

Apple (AAPL) has officially announced that Tim Cook will step down as CEO and transition into executive chairman, with John Ternus taking over the reins on Sept. 1, 2026. Despite strong financials, Apple's stock has barely moved in 2026, down 2% year-to-date (YTD), underperforming the tech-heavy Nasdaq Composite ($NASX) gain of 6.8%, as concerns grow over its slow pace in artificial intelligence (AI) and product innovation.

Adding to the uncertainty, leadership changes are rarely welcomed by markets, raising the stakes even further for what comes next.

Can a new CEO revive AAPL stock?

The AI Gap: Apple vs. Big Tech Rivals

Under Tim Cook’s tenure, Apple expanded its ecosystem, built a massive services business, and delivered steady financial growth. This leadership change will mark the end of a 15-year era that transformed Apple into a roughly $4 trillion giant. Apple continues to dominate in premium hardware, but its innovation, especially in AI, has lagged. It has struggled to keep pace with competitors' AI developments.

According to Reuters, industry analysts believe that Apple has taken a more cautious approach with AI by embedding AI into its existing products rather than launching transformative AI-first platforms. Meanwhile, its peers like Microsoft (MSFT) and Alphabet (GOOG) (GOOGL) are aggressively building generative AI ecosystems, reshaping productivity software, search, and cloud computing. John Ternus, currently Apple’s senior vice president of hardware engineering, is not an outsider. He has spent over two decades with Apple, helping build core products like the iPhone, iPad, and Mac. His appointment signals continuity but also raises doubts about whether Apple is willing to take the kind of risks needed to catch up in AI. This is most likely why the market did not react positively to the news.

Apple Is Still a Cash Machine

Apple’s financial engine remains incredibly strong. The company reported 16% year-over-year (YoY) growth in revenue to $143.8 billion in the first quarter of fiscal 2026, with EPS increasing 19% to $2.84. Gross margin expanded to 48.2%, reflecting both pricing power and a favorable product mix. The iPhone continues to power Apple’s growth engine, with sales up 23% to $85.3 billion, driven by strong demand for the iPhone 17 lineup and expanding market share across key regions.

In Apple’s service business, high-margin segments like cloud, payments, advertising, and subscriptions continue to scale rapidly, generating $30 billion in revenue, up 14% YoY. Apple’s ecosystem remains its greatest competitive advantage. It also ended the quarter with a robust balance sheet with $145 billion in cash and marketable securities, while also returning $32 billion to shareholders through dividends and buybacks.

Growth Without Innovation

Undoubtedly, Apple has executed flawlessly in its existing business under Cook’s leadership. However, now AI is reshaping what the next phase of growth will look like, and this is where the company is falling behind.

Take the iPhone, for example, which continues to be a dominating factor of Apple’s sales. But it only benefits from extraordinary customer loyalty. According to Accio research, iPhone’s retention rate stands around 92%, one of the highest in the industry. Apple also controls over 60% of the global premium smartphone segment, which reflects its pricing power and brand prestige. However, over the past few years, there has been more hype and fewer upgrades in the new iPhone models. Consumers upgrade not just for features but because the iPhone has become a status symbol and an entry point into Apple’s tightly integrated ecosystem.

Even its much-anticipated AI upgrades to Siri have lagged competitors. Voice assistants driven by large language models (LLMs) are becoming increasingly useful, yet Siri continues to struggle with complex, contextual tasks. This gap is becoming more obvious and damaging for Apple. This indicates that Apple can continue growing even when its products rarely evolve.

From an investor's perspective, I believe Apple remains a powerhouse and will continue to do so under Ternus' leadership. However, to reinvent itself and get ahead in the AI race will require bold vision and not just execution.

The Verdict: Can Apple Reinvent Itself Again Under the New CEO?

The new CEO will inherit both a powerhouse and a challenge. AI is an innovation race. And Apple's next chapter will depend not on how well it protects what it has built, but on whether it can create something entirely new to get ahead in the AI race. Investors willing to bet on this might want to accumulate AAPL stock on the dip now, as it is down 8% from its 52-week high of $288.62.

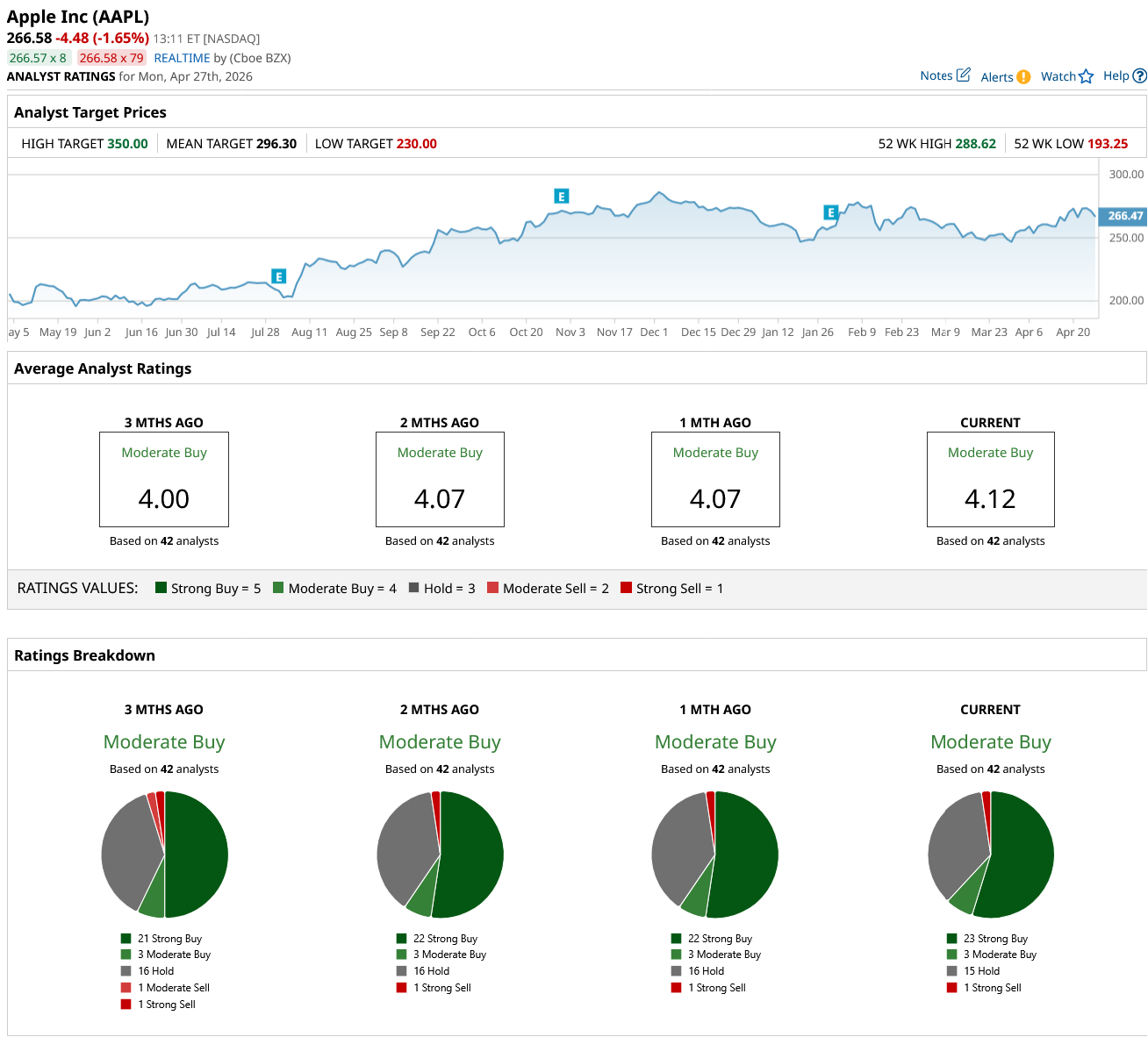

On Wall Street, AAPL stock holds a consensus “Moderate Buy” rating. Of the 42 analysts covering the stock, 23 offer a “Strong Buy” rating, three have a “Moderate Buy,” one gives a “Strong Sell,” and 15 analysts offer a “Hold” rating. Apple’s average target price of $296.30 suggests it has a potential upside of 11% from current levels. The Street-high estimate of $350 implies that shares can rally as much as 31% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)