/Microsoft%20Corporation%20logo%20on%20phone-by%20rafapress%20via%20Shuterstock.jpg)

The tech earnings season has begun, and Microsoft (MSFT) is set to report its second quarter of fiscal 2026 earnings on April 29. There was a time when owning MSFT stock happened without a shadow of a doubt. As a legacy tech player backed by a strong balance sheet, recurring revenue, and consistent earnings growth, MSFT was believed to be a “buy-and-forget” stock. But today, investors are questioning whether AI-driven tech stocks are overvalued and rotating out of them to more defensive sectors.

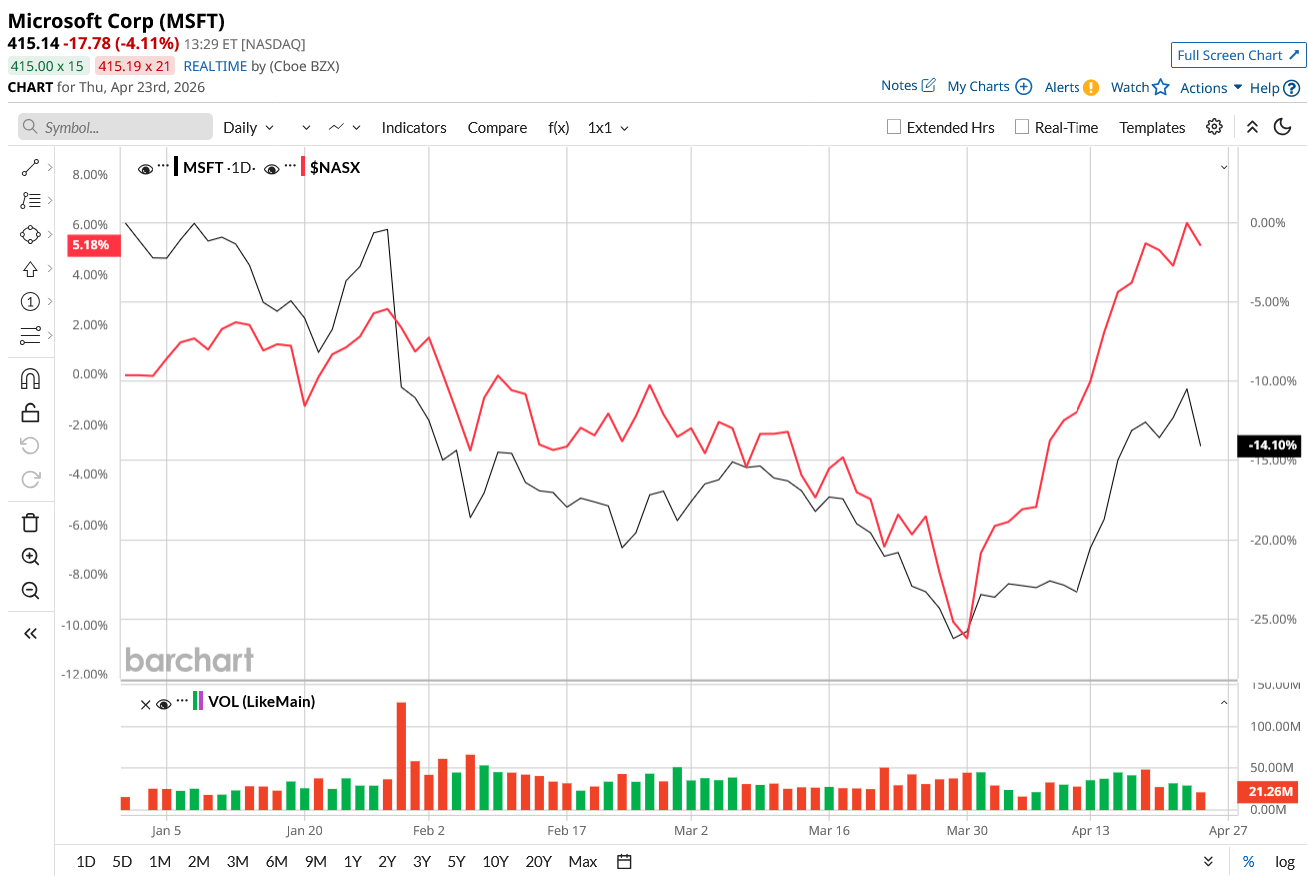

Like most tech stocks this year, Microsoft's stock hasn’t been immune to the shift in the market sentiment. The stock is down 14% year-to-date (YTD), compared to the tech-heavy Nasdaq Composite ($NASX) gain of 6%, but its fundamentals remain rock solid. Led by artificial intelligence (AI), its cloud business continues to scale at an impressive pace, and the tech titan shows no sign of slowing.

So, what should investors look out for in Microsoft's Q2 earnings?

Cloud and AI Momentum Is Driving Microsoft’s Story

Microsoft’s cloud and AI businesses are driving its growth story. Its cloud segment grew 26% year-over-year (YoY) to $50 billion in revenue in the first quarter of fiscal 2026. The credit goes to Azure, Microsoft’s cloud platform, which continues to benefit from enterprise migration and the surge in AI workloads. Notably, Azure and related services reached nearly a 39% increase in revenue in Q1. The Intelligent Cloud segment, overall, generated $32.9 billion in revenue, up 29% from the year-ago quarter. Management stressed that demand is still outpacing supply, implying that growth may continue in the short term.

In the first quarter, revenue climbed to over $80 billion, while adjusted earnings surged 24% to $4.14 per share. However, margins are feeling slightly pressured due to rising AI expenditures. The company spent $37.5 billion in capital expenditures during the quarter, with about two-thirds of that going toward short-lived assets like GPUs and CPUs.

Additionally, Microsoft reported $6.7 billion in finance leases tied primarily to large data center investments and $29.9 billion in cash paid for property and equipment. Gross margin stood at 68%, slightly down YoY owing to continued investments in AI capacity and increased usage of AI-powered services. Despite the expenditures, the company generated free cash flow worth $5.9 billion.

AI is not just an add-on for Microsoft’s products. The company has now deeply embedded AI across its entire stack, creating a vertically integrated advantage. For the second quarter, management expects revenue growth of 15% to 17%, to $80.65 billion to $81.75 billion. Intelligent Cloud revenue could increase by 27% to 29%, with Azure growing by 37% to 38%. With competition in AI intensifying, this quarter will reveal whether Microsoft can scale capacity fast enough to meet demand without sacrificing profitability.

Analysts forecast Microsoft’s earnings to increase by 22% in fiscal 2026 to $16.66 per share. At around 22x forward 2027 earnings, Microsoft sits at a reasonable valuation, considering expected earnings growth of 13.4% in fiscal 2027.

Buy, Hold, or Sell: The Verdict Before Q2

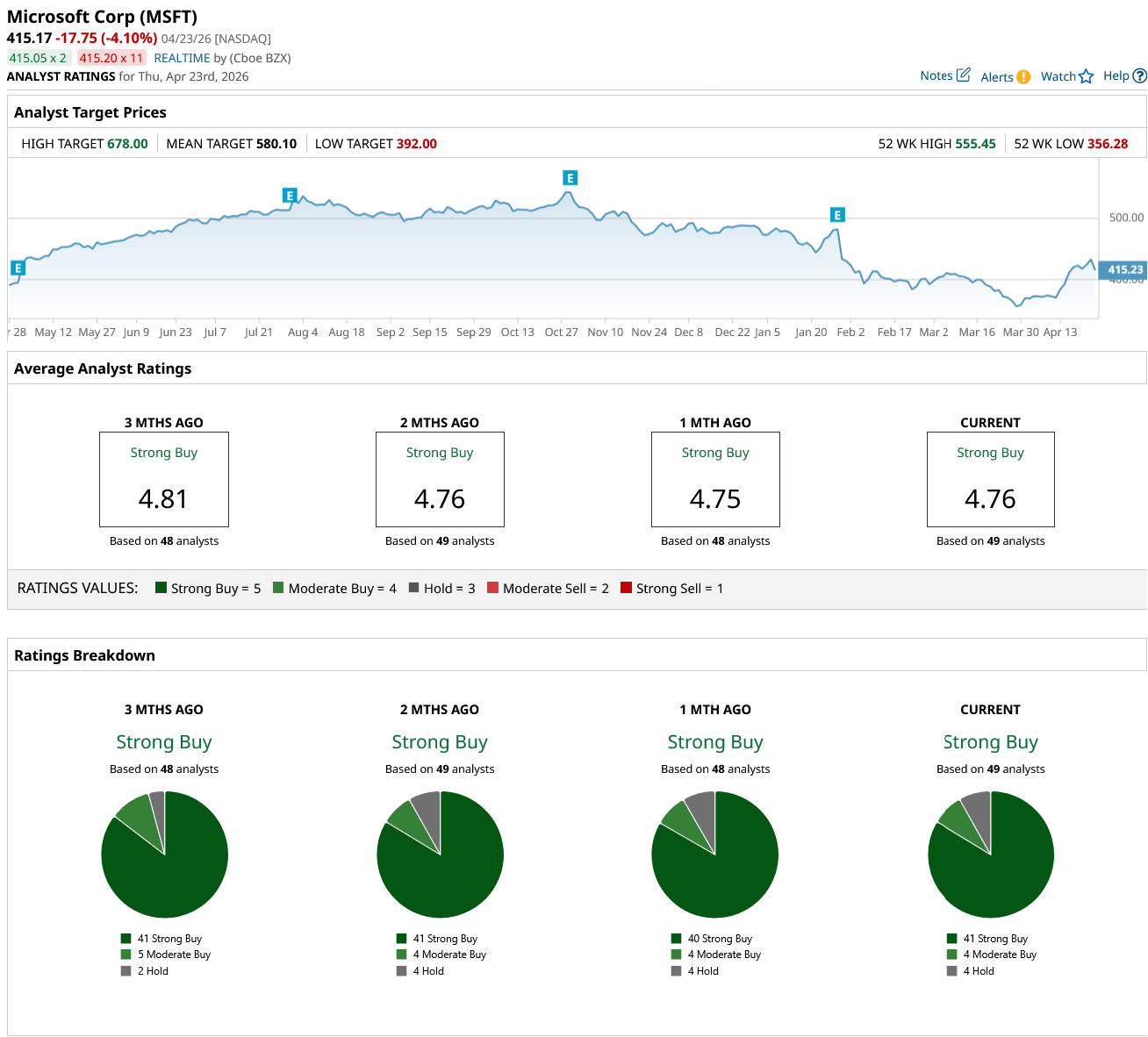

Overall, MSFT stock holds a consensus “Strong Buy” rating on Wall Street. Of the 49 analysts covering the stock, 41 rate it a “Strong Buy,” four say it is a “Moderate Buy,” and four recommend a “Hold.” The average target price of $580.10 suggests MSFT stock could climb by 40% from current levels. Plus, its high price estimate of $678 implies an upside potential of 63% over the next year.

In my opinion, if you are a long-term investor, MSFT is not the kind of stock you sell even though it is down almost 25% from its 52-week high of $555.45. Most of the AI stocks took a hit this year owing to broader market sentiment rather than any major change in their fundamentals. In fact, Microsoft stock is a better buy on the dip now.

Microsoft is a legacy tech player who has maintained steady growth over the years even when AI was not in the picture. I believe Microsoft can sustain its AI-fueled momentum even in this cautious market environment and remains an excellent hold for the next decade.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)