/Dominos%20Pizza%20Inc%20storefront%20by-KathyDewar%20via%20iStock.jpg)

Headquartered in Ann Arbor, Michigan, Domino's Pizza, Inc. (DPZ) is one of the world's largest pizza restaurant chains, operating through a network of company-owned and franchised stores across more than 90 markets. With a market cap of $9.5 billion, the company specializes in pizza delivery and carryout services, offering a menu that includes pizzas, chicken, sandwiches, pasta, breads, desserts, and beverages.

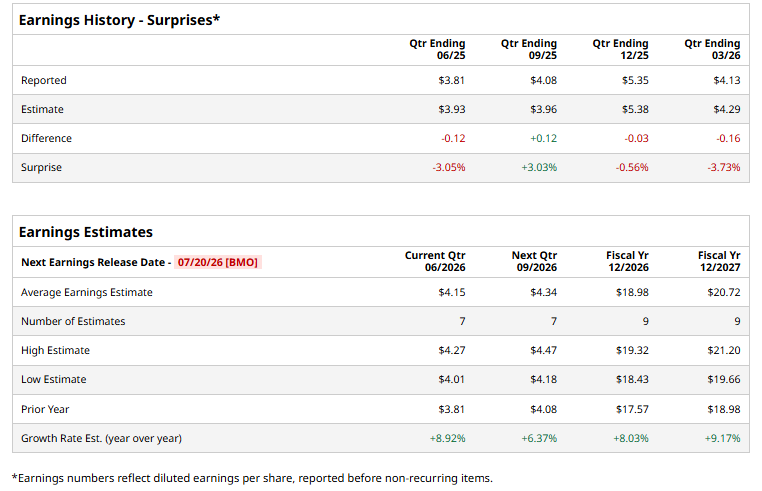

The global pizza chain titan is expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Monday, July 20.

Ahead of the event, analysts expect DPZ to report a profit of $4.15 per share on a diluted basis, up 8.9% from $3.81 per share in the year-ago quarter. Sadly, the company has exceeded the consensus estimates in only one of the last four quarters while missing the forecast on three other occasions.

For the current year, analysts expect DPZ to report EPS of $18.98, up 8% from $17.57 in fiscal 2025. Its EPS is expected to rise 9.2% year over year to $20.72 in fiscal 2027.

DPZ stock has significantly underperformed the S&P 500 Index’s ($SPX) 20.8% gains over the past 52 weeks, with shares down 37% during this period. Similarly, it underperformed the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 6.4% rise over the same time frame.

On June 23, Domino's shares fell 3.2% after the company announced that CEO Russell Weiner will retire, with President and COO Joe Jordan set to succeed him on Oct. 1. The leadership change prompted several analysts, including JPMorgan, BTIG, RBC Capital, and Baird, to lower their price targets, citing slowing pizza sales, increasing competition, and expectations that the new CEO is unlikely to resolve the company's near-term challenges.

Analysts’ consensus opinion on DPZ stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 29 analysts covering the stock, 15 advise a “Strong Buy” rating, 12 give a “Hold,” and two recommend a “Strong Sell.” DPZ’s average analyst price target is $399.14, indicating a notable potential upside of 39.8% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.