/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

Salesforce (CRM) founder and CEO Marc Benioff isn’t buying the “SaaS is dead” narrative. With CRM stock down 41% from its 52-week high, that’s quite a rich position for the CEO to take. The disruption from artificial intelligence (AI) isn’t just hurting Salesforce — it is bringing the whole software sector down, with the iShares Expanded Tech-Software Sector ETF (IGV) down more than 20% so far this year.

In an interview with The Wall Street Journal, Benioff said, “the opportunity has never been greater.” Instead of surrendering to the thesis that AI will kill the need for its services, Salesforce is integrating AI into its offerings to better serve customers. Salesforce also works closely with OpenAI and Anthropic, but the firm’s own investors are now asking some tough questions. Will the company be able to improve its customer-issue handling to an extent that will require no human intervention, or is its AI just good for basic tasks? Additonally, will Salesforce be able to handle the loss of revenue when its AI becomes so good that companies don’t need to buy as many seats as before?

Salesforce has already switched to a hybrid subscription model that now charges for consumption in addition to seat licenses. This will lower the revenue hit the company may have to take by offering AI products. But the market clearly isn’t sold on the notion that Salesforce will offer good enough AI to sustain its past dominance. Benioff did point out data security and compliance as two competitive advantages, giving the firm a moat of sorts. In the age of AI, though, this might not be the strength the CEO thinks it is.

About Salesforce Stock

Salesforce is a global enterprise software company. The company provides customer relationship management (CRM) and cloud-based business applications across sales, service, marketing, commerce, and data analytics. Its Customer 360 platform, powered by data tools and trusted AI, enables organizations to unify customer data and drive personalized engagement.

Salesforce has underperformed the S&P 500 ($SPX) over the past 52 weeks. The index has gained around 32% while CRM stock has declined by approximately 31% during the same period. The weakness has also continued into the current year, with CRM stock down roughly 35% year-to-date (YTD). In contrast, despite temporary dips due to geopolitical uncertainty, the broader market has recovered and is now up more than 3% YTD.

The valuation discount available on CRM stock is staggering. It now trades at a forward price-to-earnings (P/E) ratio of 19.2 times, which is will below its five-year average. This is also below the IT sector median forward P/E of 23 times. On a forward price-to-cash flow basis, the discount is similar compared to the five-year average. This is a stock that is doing everything it can to actively dominate the AI era, with the CEO coming out and assuring investors that the firm is doing all it can. Yes, there may be risks — but at this valuation, the risks could well be worth the reward.

Interestingly, insiders have been buying CRM stock in the last few months. Most recently, two directors bought roughly $500,000 worth of shares each on March 18 and March 19. Director Mason Morfit also bought $25 million worth of shares back in December when the stock was over $260. This was when the company was pivoting to AI. Morfit hasn’t sold since, which should give investors a lot of confidence when buying at discounted levels.

Agentforce Drives Salesforce’s Revenue Growth

Salesforce posted its fourth-quarter fiscal 2026 results on Feb. 25. Revenue for the quarter came in at $11.2 billion, up 12% compared to the same period last year. Full-year revenue totaled $41.5 billion, reflecting 10% year-over-year (YOY) growth. Agentforce annual recurring revenue (ARR) reached $800 million, showing strong growth of 169% YOY. Informatica Cloud ARR was $1.1 billion. Salesforce expanded its share repurchase program to $50 billion, as well as increased its quarterly dividend to $0.44 per share.

Heading into 2027, the company projects Q1 revenue to be in a range between $11.03 billion and $11.08 billion. The current remaining performance obligation (RPO) is estimated to grow by approximately 14% YOY. Management expects fiscal 2027 revenue to be $45.8 billion to $46.2 billion, which suggests 10% to 11% YOY growth. Non-GAAP operating margin is forecast at 34.3% while GAAP operating margin is at 20.9%.

What Are Analysts Saying About Salesforce Stock?

On April 16, Truist analyst Terry Tillman reaffirmed a “Buy” rating on CRM stock along with a $280 price target, which implies 61% potential upside from the current levels. BTIG also recently maintained a “Buy” rating on shares. The firm’s price target of $255 offers 47% potential upside from here.

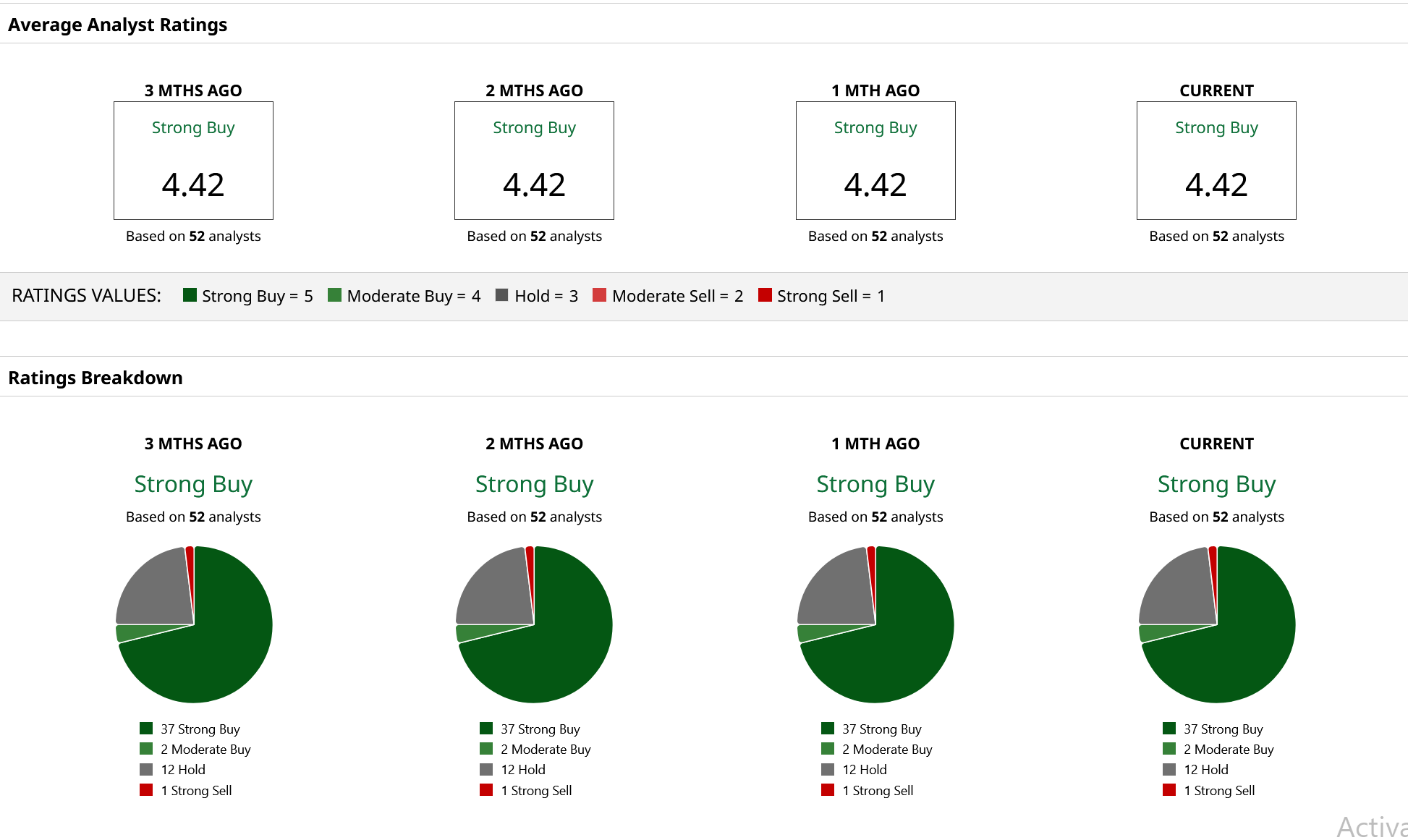

According to 52 Wall Street analysts covering the stock, CRM enjoys a consensus “Strong Buy” rating. The stock obviously hasn't responded as enthusiastically to these ratings as one would like, but that's where the opportunity lies. Based on analyst estimates, Salesforce stock has a mean price target of $276.43, reflecting approximately 60% possible upside from current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)