/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Investors in Micron Technology (MU) have ridden a rollercoaster that would test even seasoned nerves. The stock surged to an all-time high earlier this year as buyers chased a historic memory shortage, only to reverse sharply. Now, it has clawed its way back, proving momentum rarely travels in straight lines.

On Wednesday, April 22, MU stock reclaimed its swagger, hitting a fresh 52-week high of $491.98 while jumping 8.5% intraday. Markets cheered relentless demand for high-bandwidth memory (HBM) chips and latched onto hopes of easing Middle East tensions, injecting both fundamental strength and macro optimism into the rally.

Micron’s rally rests on a simple imbalance that demand overwhelms supply. The company has admitted that it can satisfy only half to two-thirds of HBM demand over the medium term. The shortfall forces prices higher, tightens supply chains, and hands pricing power back to producers, an enviable position in a capital-intensive industry.

Moreover, Micron expects the HBM market to expand from $35 billion in 2025 to $100 billion by 2028. The near tripling in three years stretches supply capabilities and suggests the shortage will linger. In effect, scarcity becomes a feature, not a bug, sustaining elevated pricing.

Even so, the narrative carries a geopolitical footnote. If tensions involving Iran fail to de-escalate into a durable agreement, disruptions in oil transit could dent risk appetite. Tech stocks, particularly high-beta names like MU, often feel the first tremors when macro uncertainty resurfaces. So let us see what stance to take with MU stock.

About Micron Stock

Best known for its memory chips, Micron designs and manufactures dynamic random-access memory (DRAM), NAND flash memory, and storage solutions that accelerate data centers, personal computers (PCs), smartphones, and intelligent machines.

Commanding a market cap of $549.8 billion, it converts silicon into speed, capacity, and efficiency across cloud, mobile, automotive, and industrial ecosystems, and uses its software, tools, and platforms to translate performance into reliable, scalable computing outcomes.

The stock’s performance reads like a highlight reel. Shares of the Boise, Idaho-based company have soared 561.3% over the past 52 weeks. The rally continued in 2026 as well, with the stock climbing 69% year-to-date (YTD), with another 20.7% gain in just the last three months.

From a valuation standpoint, MU stock is currently trading at 7.79 times forward adjusted earnings. The figure is trading below both the industry average and its own five-year average multiple, indicating a discount. The pricing signals a relatively wise entry point in the stock.

Micron also returns modest cash to shareholders. It pays an annual dividend of $0.60 per share, yielding 0.13%. On March 18, management raised the quarterly payout by 30% to $0.15 per share, rewarding shareholders of record as of March 30, with payments distributed on April 15.

Micron Surpasses Q2 Earnings

Micron posted a blockbuster fiscal 2026 second quarter on March 18, driving revenue up 196.3% year-over-year (YOY) to $23.9 billion and surpassing the $19.9 billion Street estimate. The company powered this surge through record DRAM, NAND, and high-bandwidth memory performance, fueled by strong artificial intelligence (AI) demand and firmer pricing.

Profitability scaled even faster. Non-GAAP operating income jumped 719.9% to $16.5 billion, while net income climbed 686.4% to $14 billion. Non-GAAP EPS also skyrocketed 682.1% to $12.20, crushing the Street’s forecast of $8.80. Adjusted free cash flow hit $6.9 billion, translating accounting strength into tangible liquidity.

Micron exited the quarter with $16.7 billion in cash and investments, giving it ample firepower. Looking forward, management plans to spend over $25 billion this fiscal year, primarily on capacity expansion, while construction spending is set to rise by over $10 billion YOY in fiscal year 2027.

Management projects fiscal Q3 2026 non-GAAP revenue of approximately $33.5 billion, nearly equal to its total revenue for the prior fiscal year, with a potential variance of $750 million on either side. And, they expect non-GAAP EPS of about $19.15, with a possible swing of $0.40.

Analysts largely agree with the trajectory. They forecast Q3 fiscal year 2026 EPS of $18.97, implying a staggering 996.5% YOY increase. For the full fiscal year 2026, estimates call for EPS of $57.71, up 651.4% from the prior year, followed by another 69.4% rise to $97.77 in fiscal year 2027.

What Do Analysts Expect for Micron Stock?

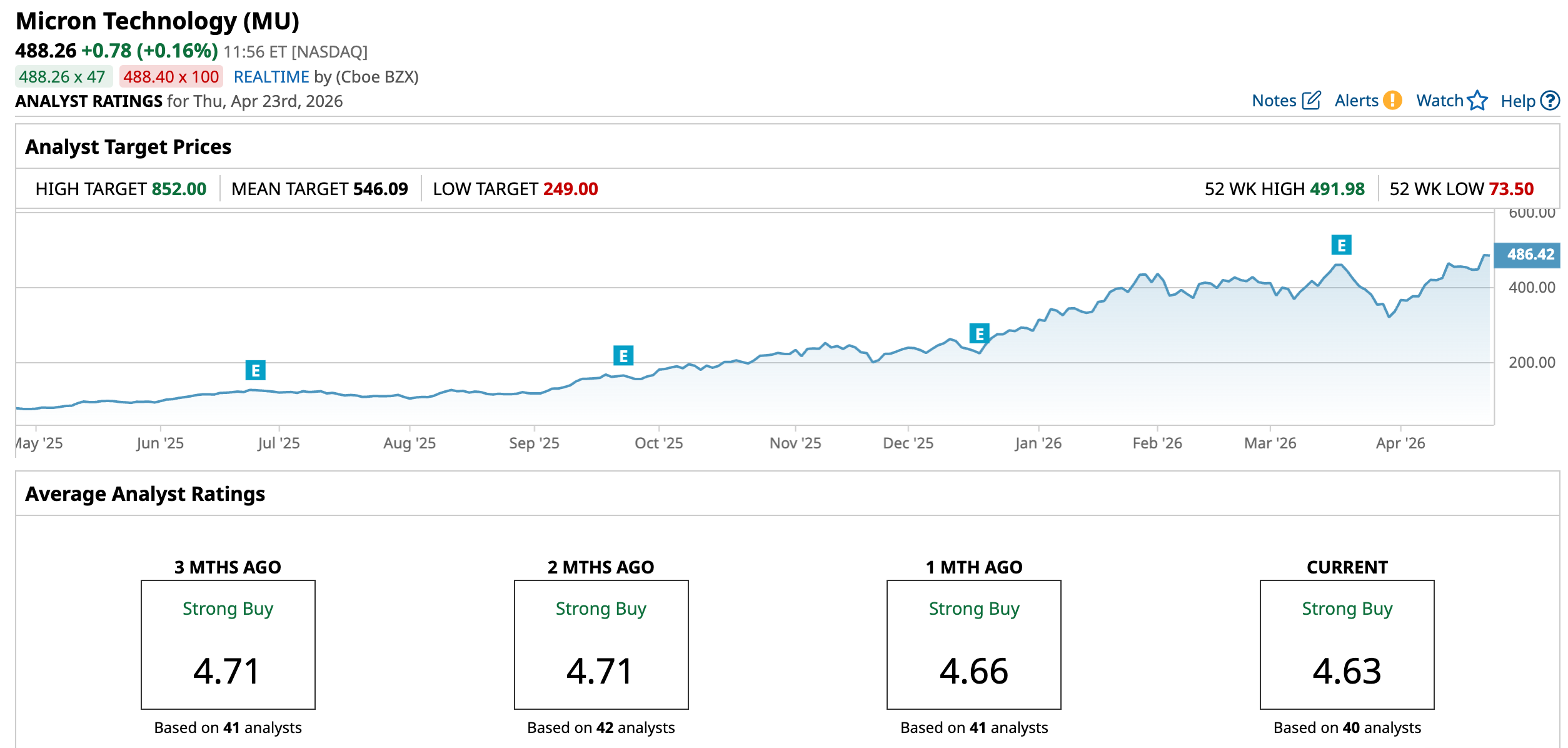

On the Street, sentiment leans decisively bullish. Cantor Fitzgerald has maintained an “Overweight” rating with a $700 price target, expecting strong fundamentals to offset concerns around AI spending. Additionally, the firm highlights prolonged semiconductor equipment shortages as a tailwind for pricing power.

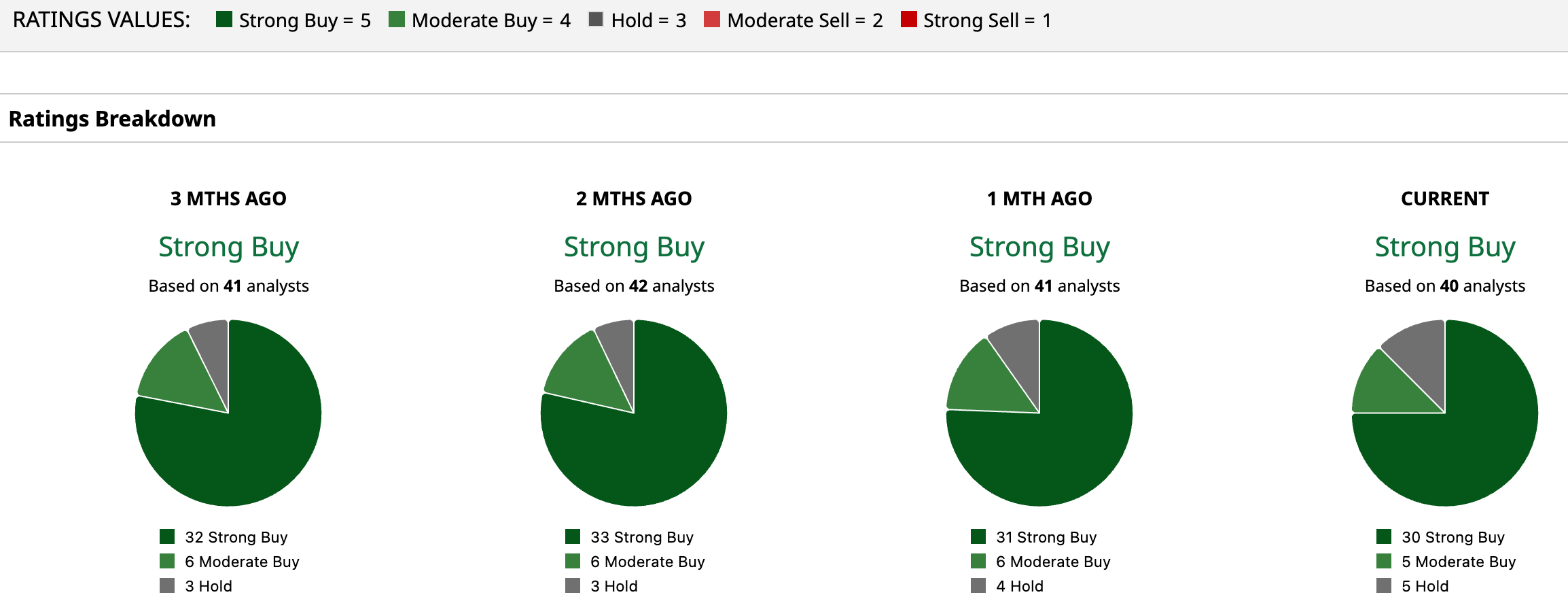

Currently, Wall Street has assigned MU stock an overall rating of “Strong Buy.” Among 40 analysts covering the stock, 30 rate it a “Strong Buy,” five have issued a “Moderate Buy,” while five recommend “Hold.”

To that end, the average price target of $546.09 implies potential upside of 11.8%. Meanwhile, the Street-high target of $852 points to a possible gain of 74.5% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)