/Apple%20Inc%20Tim%20Cook-by%20John%20Gress%20Media%20Inc%20via%20Shutterstock.jpg)

It was easy to pick Apple (AAPL) as the top pick for 2026 at the beginning of the year. The company was finally bringing in an AI addition to Siri while riding a strong product cycle and consumer demand for its products. No one, however, could have predicted that just weeks into the second quarter of the year, the company would decide to change the man who was the number one at the Cupertino-based firm since 2011.

Tim Cook’s departure is surprising, not because he was clearly great at his job, but because if it was based on the lack of AI achievements, it came far too late. Apple’s underwhelming innovation in artificial intelligence was noticed by everyone in 2024. First, the launch was delayed. Then it was said that China won’t have access to Apple intelligence features due to local laws requiring AI models to be based in China. At the same time, Chinese phonemakers were openly flaunting their AI achievements that were far ahead of what Apple was planning. Apple’s innovation edge had disappeared.

For many months, commentators reminded everyone that Apple was in the habit of perfecting its technologies before launching them. It didn’t matter if the company was late as long as it was the best. Today, we know that the company wasn’t just late but also isn’t the best anymore, at least when it comes to AI features.

What’s done is done, though. John Ternus will take over from Sept. 1, ending Cook’s 15-year tenure. Ternus currently serves as the senior vice president of hardware engineering. He has played an integral role in Apple’s design achievements over the years. However, this now begs the question of whether he is being brought in to begin Apple’s AI revolution or if the company has given up on changing that? It would be foolish to rule him out so early, but there is no doubt that Apple’s failures have given competitors an opening, and Ternus has his work cut out for him.

About Apple Stock

Apple operates as a manufacturer, marketer, and designer of PCs, smartphones, wearables, tablets, and accessories globally. Its product lineup includes iPhones, Macs, iPads, wearables, home devices, and accessories. Moreover, the company also provides different subscription-based services, such as Apple Fitness+, Apple Music, Apple Card, Apple Pay, and others. Apple serves the enterprise, education, and government markets, as well as consumers and small and midsized businesses.

Unlike last year, Apple has underperformed the S&P 500 ($SPX) so far this year. The stock delivered returns of around 37% over the last year, while the broader index gained roughly 33%. Year-to-date (YTD), AAPL stock is just about flat, while the S&P 500 is at about 4%. It takes a lot to move the needle on such a large company. At a $4 trillion valuation, stocks move slowly, and Apple is no exception.

iPhone Boosts Revenue Growth

The company reported its first-quarter FY 2026 on January 29. Apple generated $143.8 billion in revenue for the quarter. This represents a 16% year-over-year (YoY) growth. Growth was primarily driven by the iPhone lineup, with revenue reaching $85.3 billion. This reflects a 23% YoY increase, supported by strong demand for the iPhone 17 series. Services also delivered solid performance, generating $30 billion in revenue, up 14% year over year. The company saw record performance in areas like advertising, music, cloud services, and payment services. Earnings came in at $2.84, and net income reached $42.1 billion.

For the March quarter, the iPhone maker expects total revenue to grow from 13% to 16% YoY. The outlook also factors in continued constraints from limited iPhone supply. Services revenue is likely to grow at a rate similar to the December quarter. Gross margin is forecasted in the range of 48% and 49%. According to the management, the outlook reflects ongoing supply challenges, particularly related to iPhone production. The company reports its next quarterly earnings on April 30.

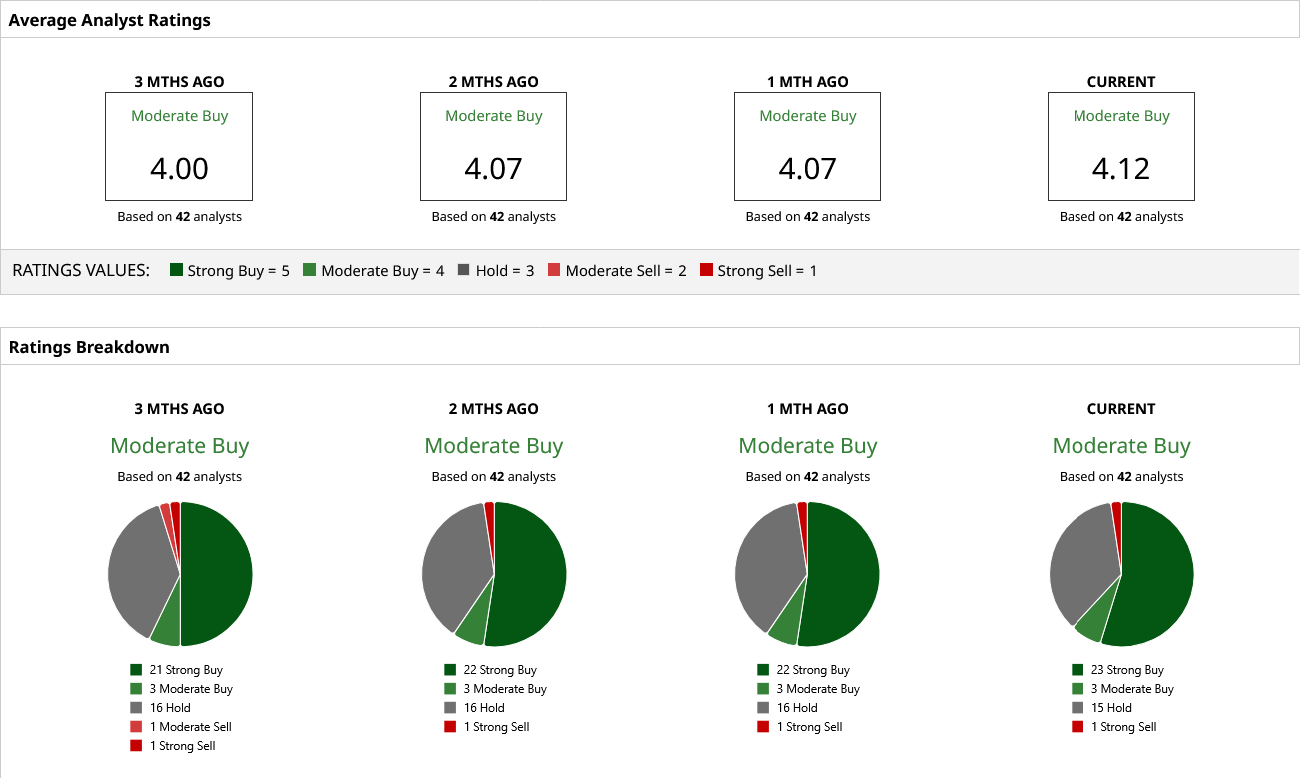

What Are Analysts Saying About AAPL Stock?

Ahead of the company’s earnings report on April 30, analysts revised their ratings and price targets on AAPL stock. Wedbush Securities released a report on April 21 in which analyst Daniel Ives maintained a “Buy” rating on the shares with a price target of $350. A day earlier, Morgan Stanley raised its price target on the stock from $305 to $315, reflecting the same bullish stance on Apple from last month.

A consensus “Moderate Buy” rating from 42 Wall Street analysts covering Apple highlights strong analyst support. The most bullish price target of $350 implies 28% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.