/Seagate%20Technology%20Holdings%20Plc%20office-by%20JHVEPhoto%20via%20Shutterstock.jpg)

As investors are prioritizing AI data center components, memory integrated circuits might be in for a windfall. BNP Paribas Equity Research senior analyst Karl Ackerman believes that components in short supply, such as memory ICs and optical components, are relatively better positioned demand-wise.

Although Ackerman remains bullish on the sector, he prefers hard disk drives (HDDs) due to their durable supply-and-demand dynamics. In that regard, BNP Paribas expects Seagate Technology Holdings plc (STX) to experience a faster margin expansion than its peers due to the adoption of its 40TB HAMR products in the second half of this year. Its EPS (on a diluted basis) is projected by Wall Street analysts to grow 94.6% year-over-year (YOY) to $3.25 for the third quarter of FY26 (to be reported on May 5, after the market closes).

In light of this, we take a deeper look at Seagate now.

About Seagate Stock

Seagate is a leading provider of data storage solutions, offering HDDs and solid-state drives (SSDs). The company has a vertically integrated model that covers research and development, design, manufacturing in facilities, and worldwide distribution to serve hyperscale data centers, cloud providers, enterprises, and consumers. The company emphasizes innovation in areal density for AI-driven data lakes.

The explosive demand for high-capacity HDDs in AI data centers and cloud infrastructure has led to a significant surge in Seagate’s stock, as hyperscalers, which are essentially major tech firms, focus on massive storage needed to train large language models (LLMs). Based in Singapore, the company has a market capitalization of $113.3 billion.

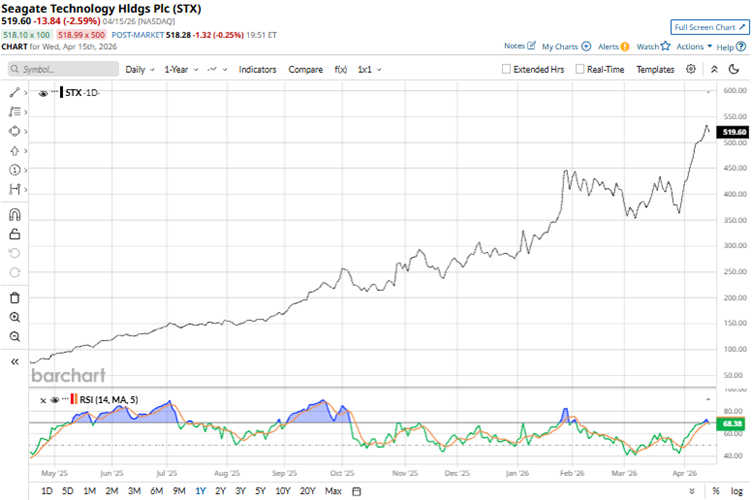

Over the past 52 weeks, Seagate’s stock has gained a whopping 612.96%, while it is up 129.69% over the past six months. Moreover, this year, the stock is up 88.52%. Seagate’s shares reached a 52-week high of $534.23 on Apr. 14, and are down only 2.2% from that level.

Seagate’s 14-day RSI of 68.23 indicates that the stock is closer to the overbought territory. On a forward-adjusted basis, its price-to-earnings ratio of 39.73 times is higher than the industry average of 23.04 times.

The Memory Landscape

The rapid AI buildout has created a shortage of memory chips, leading to an unprecedented surge in their prices. Memory prices might remain elevated throughout this year and the next, especially given high demand from hyperscalers. In fact, according to one estimate, memory will account for roughly 30% of total hyperscaler capex this year, reflecting a huge jump from approximately 8% in 2023 and 2024.

Seagate’s chief commercial officer, Ban-Seng Teh, believes that memory price hikes will remain the “new normal” for the next few years as the AI boom pushes the industry to a supercycle. While the company has “definitely seen higher costs” due to rising DRAM prices, it is also riding the wave of surging demand for data storage.

Last year, Seagate stated that it is working on developing a 100-terabyte hard drive by 2030. This year, it has taken a step towards that goal as it revealed its next-generation Mozaic 4+ platform, the industry’s only heat-assisted magnetic recording (HAMR)-based storage platform deployed at scale. The platform supports up to 44TB of capacity. This positions Seagate as a prime candidate to capitalize on the AI supercycle.

Seagate Q2 Earnings Crush Expectations on Surging AI Data Center Demand

Seagate’s second-quarter results for fiscal 2026 (quarter ended Jan. 2) came in hotter than expected, driven by persistent demand from data centers and the continued ramp of its HAMR-based Mozaic products. The company’s revenue increased 21.5% YOY to $2.83 billion, beating the $2.75 billion Street analysts had expected.

In addition, Seagate realized margin expansion. Its non-GAAP gross margin grew from 35.5% in Q2 FY25 to 42.2% in Q2 FY26, while non-GAAP operating margin surged from 23.1% to 31.9%. The company’s non-GAAP EPS surged by a solid 53.2% YOY to $3.11, surpassing the $2.83 figure that analysts had expected.

Also, Seagate retired $500 million Exchangeable Senior Notes due 2028 during Q2, indicating that its balance sheet remains healthy. The company ended the quarter with $1 billion in cash and cash equivalents.

Wall Street analysts expect Seagate’s bottom line to grow robustly. For the current fiscal year, profit is expected to increase by 66.8% annually to $12.11 per diluted share, followed by a 57.1% growth to $19.03 in the next fiscal year.

Analysts Are Bullish On Seagate’s Stock

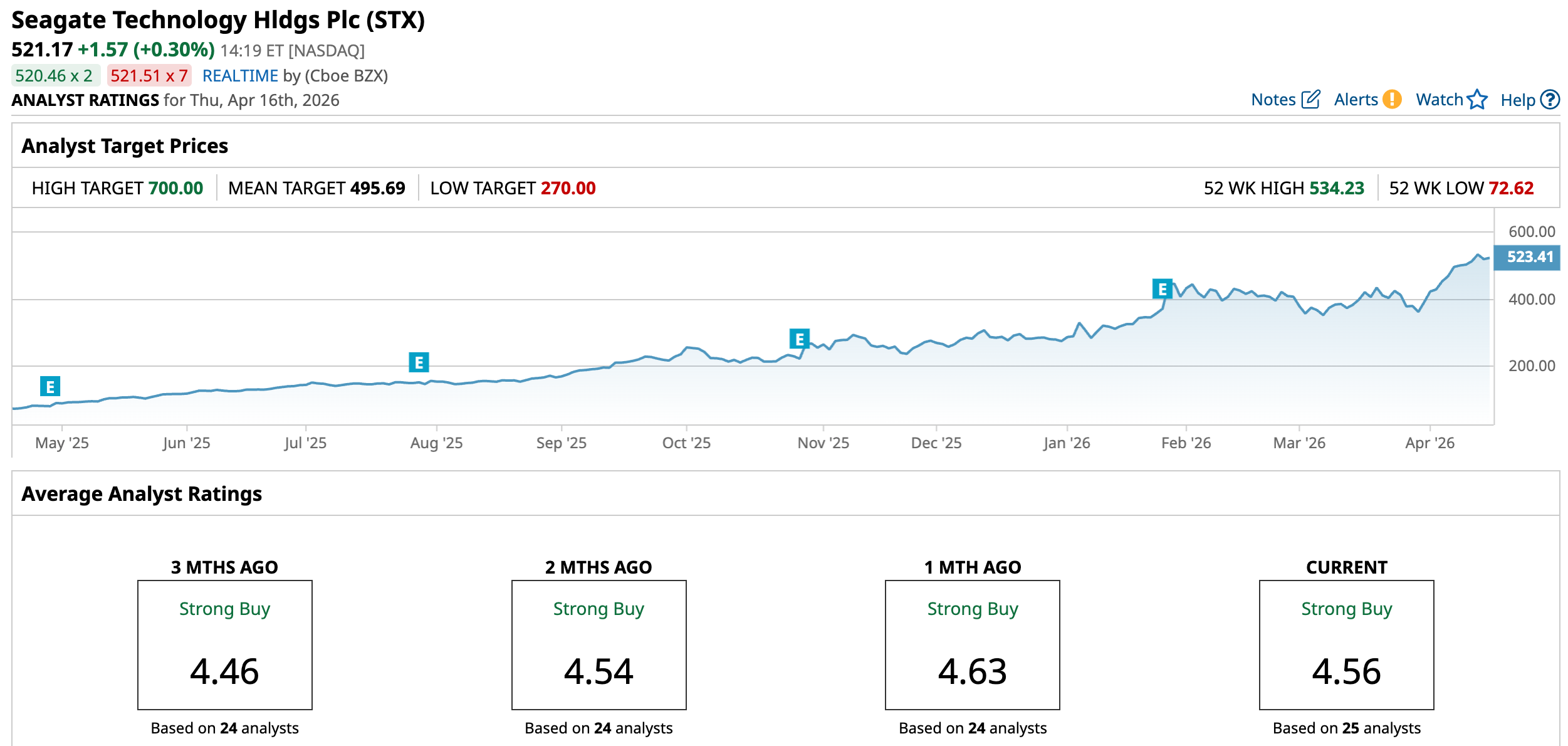

This month, analysts at Citigroup maintained a “Buy” rating on Seagate’s stock and raised the price target from $480 to $595. Analyst Asiya Merchant sees a solid demand backdrop for storage providers as AI demand accelerates.

Morgan Stanley analysts also added the stock to a “Top Pick” list, while maintaining an “Overweight” rating and raising the price target to $582 from $468. Analyst Erik Woodring stated that recent checks indicate that HDD demand is still increasing, and supply shortages could continue through 2028.

Last month, JPMorgan analysts initiated coverage of Seagate with an “Overweight” rating and a $525 price target, based on a 22 times multiple of its 2027 EPS estimate. While this implies a healthy upside, it is considered conservative relative to the roughly 25 times average multiple for AI-levered suppliers. So, there could be further upsides if cloud spending visibility improves and pricing is stronger than expected.

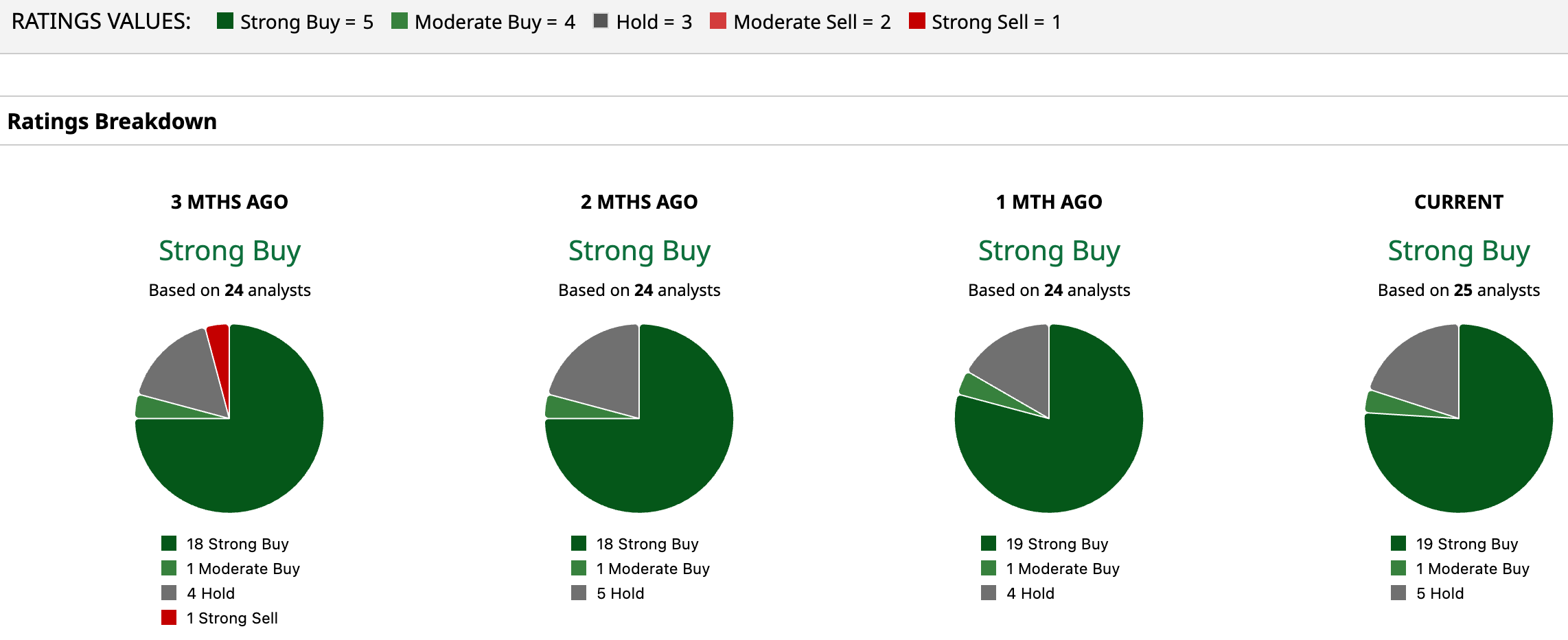

Seagate is receiving a lot of praise on Wall Street, with analysts awarding the stock an overall “Strong Buy” rating. Of the 25 analysts rating the stock, 19 have rated it a “Strong Buy,” one a “Moderate Buy,” and five a “Hold.” The consensus price target of $495.69 represents a 3.2% downside from current levels. However, the Street-high price target of $700 indicates a 34.3% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)