Artificial intelligence (AI) infrastructure names have been front and center for investors over the past year, and IREN Limited (IREN) has been one of the biggest winners of this trend. Once known primarily as a Bitcoin miner, the company made a bold pivot into AI infrastructure, and the market loved it. Backed by its existing crypto mining setup, IREN was able to quickly transition into building high-powered, server-filled data centers, fueling a massive triple-digit rally in its stock.

The real game-changer came last year when Microsoft (MSFT) signed a jaw-dropping $9.7 billion multi-year AI cloud deal with the company. That agreement, which includes deploying 76,000 Nvidia (NVDA) GB300 GPU units at its Texas campus, firmly put IREN on the AI map. And the company isn’t slowing down. Just last month, it added another 50,000 Nvidia B300 GPU units to its pipeline, taking its total planned capacity to more than 150,000 GPUs, an aggressive move that signals serious ambition.

But the story isn’t all smooth sailing. The hype around the stock has cooled this year, dragged down by dilution concerns and growing pains as the company shifts away from Bitcoin mining. Revenue has also come under pressure during this transition, raising questions about how quickly the AI business can scale. Shares are now down 38.5% from their 52-week high of $76.87, reached in November last year after the company’s headline-making deal with Microsoft.

Even so, IREN’s monster rally over the past year is hard to ignore. But after such a big move, is there more upside ahead, or has the easy rally already played out?

About IREN Stock

Australia-based IREN Limited sits at the intersection of energy and computing, running high-performance data centers powered by renewable energy. What began as a Bitcoin mining operation is now evolving into something broader, as the company leans into AI cloud services. By offering GPU-driven infrastructure for artificial intelligence, machine learning, and high-performance computing (HPC), IREN is gradually repositioning itself to serve large-scale, compute-heavy workloads beyond crypto.

Currently valued at a market capitalization of about $14.3 billion, IREN has delivered a run that’s hard to ignore. Even with a double-digit decline from its 52-week peak, the stock is still up an explosive 716.5% over the past year, dramatically outperforming the S&P 500 Index ($SPX), which rose a far more modest 28.8% over the same stretch. And while the momentum has slowed this year, IREN is still holding onto gains of 24.3% in 2026, continuing to outpace the broader market’s marginal return year-to-date (YTD).

IREN’s Q2 Earnings Show a Business in Transition

IREN’s fiscal 2026 second-quarter results, released on Feb. 5, told a classic transition story of strong on vision and weak on near-term numbers, enough to keep investors divided. On the surface, the headline figures disappointed. Revenue came in at $184.7 million, missing expectations by 16.5% and falling 23% sequentially. The pressure came from exactly where you’d expect. Bitcoin mining is slowing, while the AI business is still ramping and not yet large enough to fully offset the decline.

That imbalance hit profitability hard. The company swung to a net loss of $155.4 million from a $384.6 million profit in the prior quarter, while the per-share loss of $0.44 came in far wider than the expected $0.09 loss. A closer look at the segments reinforces the shift underway. Bitcoin revenue fell 28.2% sequentially to $167.4 million, while AI Cloud revenue surged 136.9% to $17.3 million, still small in absolute terms but growing rapidly.

In many ways, the quarter captures a business in motion, with legacy revenues fading as new growth engines begin to take shape. Importantly, the long-term picture remains backed by strong visibility. The company has already locked in $2.3 billion in annualized recurring revenue (ARR), largely tied to its $9.7 billion agreement with Microsoft. On the funding side, IREN has secured $3.6 billion in GPU-specific financing at rates below 6%, along with $1.9 billion in prepayments from Microsoft, effectively covering about 95% of the capital required for its expansion.

Liquidity also remains a key strength, with cash and cash equivalents standing at $2.8 billion as of Jan. 31, 2026. Altogether, while the near-term numbers highlight execution challenges, they also underscore a company deep in transition, trading short-term pressure for what it hopes will be long-term AI-driven growth.

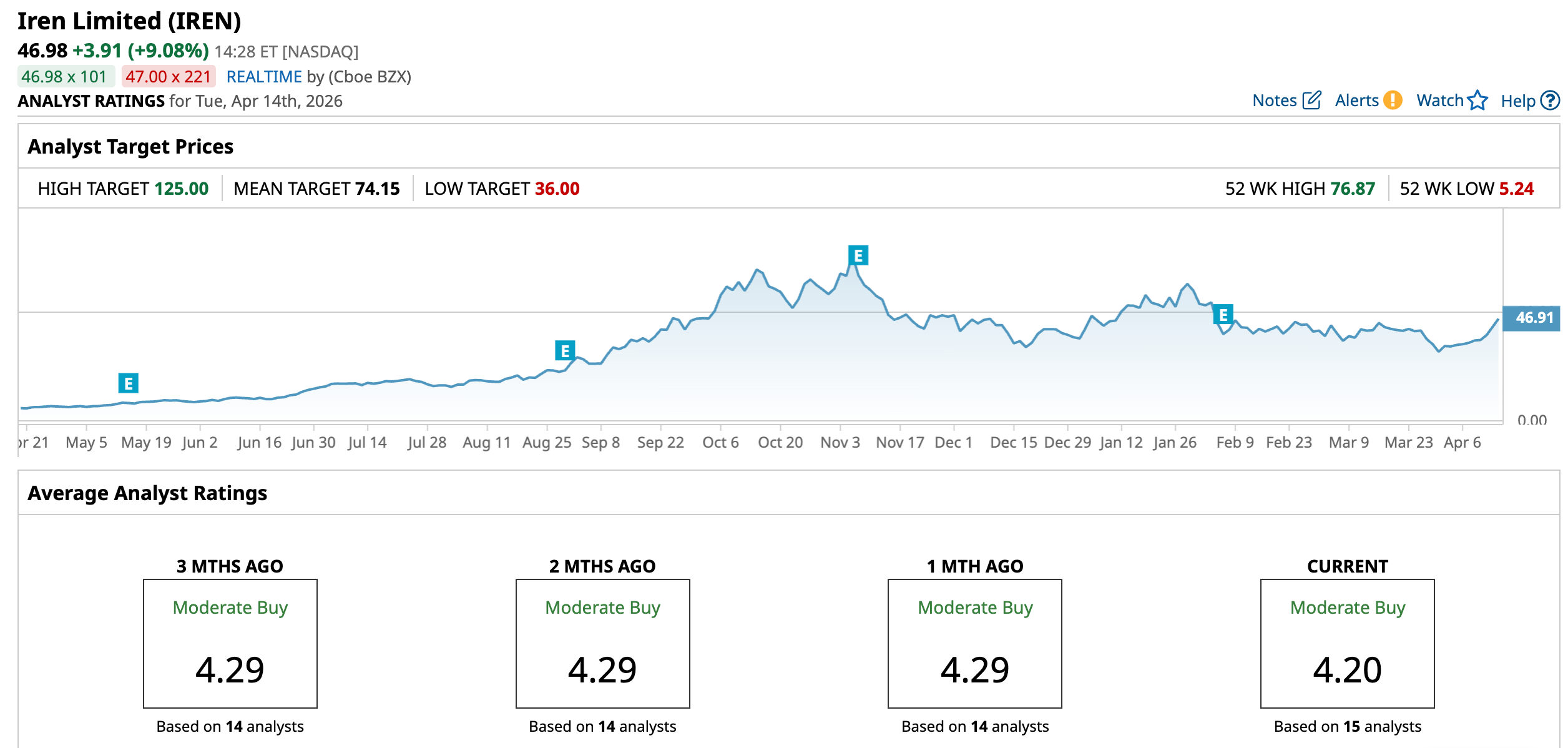

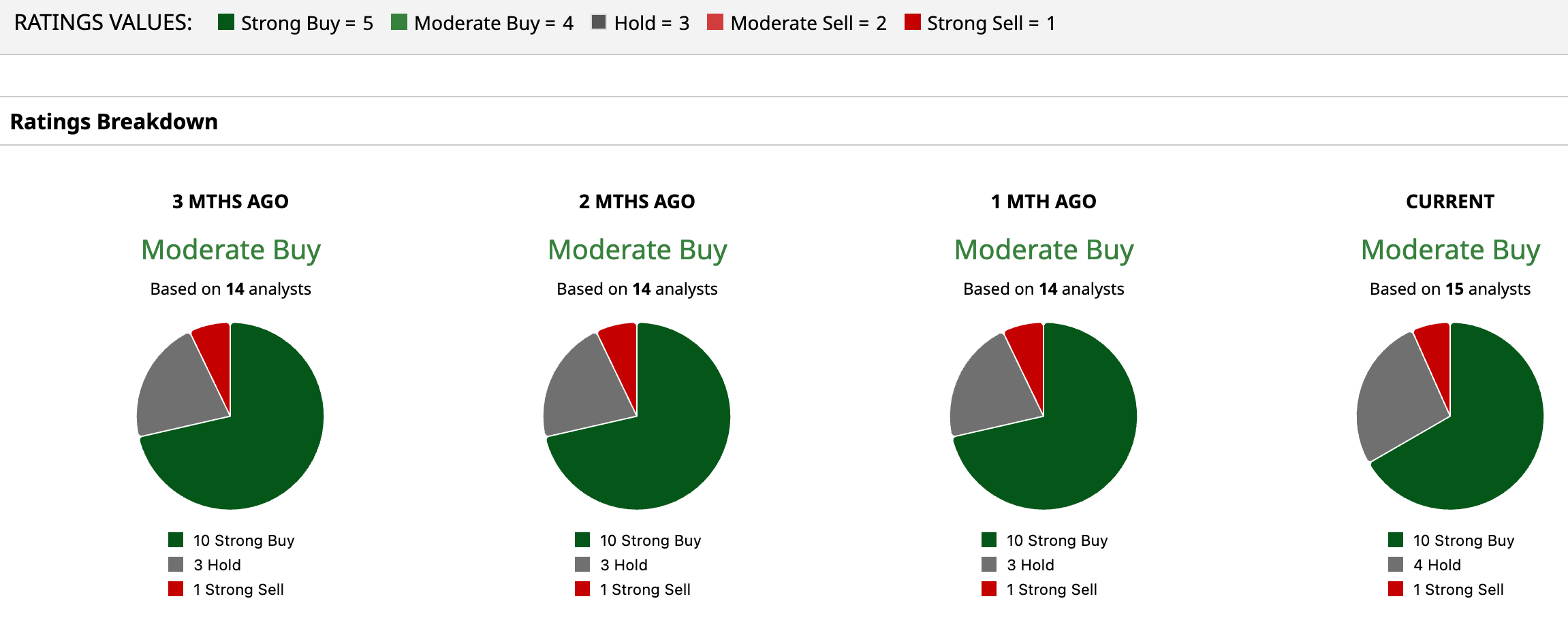

How Are Analysts Viewing IREN Stock?

Despite some volatility this year, Wall Street hasn’t lost faith in IREN. In fact, the stock still carries a “Moderate Buy” consensus rating, reflecting a market that remains broadly optimistic about its long-term AI pivot. Out of 15 analysts covering the name, a strong majority of 10 analysts are firmly bullish with “Strong Buy” ratings. Four prefer to stay cautious on the sidelines with “Hold,” while just one analyst takes a decisively bearish stance with a “Strong Sell.”

The skew clearly leans positive, signaling that most on the Street still see meaningful upside ahead. And the numbers back that up. The average price target of $74.15 points to a potential upside of about 57.8% from current levels. But it’s the high-end projections that really stand out. The Street-high target of $125 suggests the stock could surge as much as 166% if execution around its AI strategy plays out as expected.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)