/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

Netflix (NFLX) will announce its first-quarter 2025 financial results on April 16. Ahead of the announcement, NFLX stock has shown notable resilience, gaining more than 14% over the past three months despite ongoing geopolitical tensions and broader macroeconomic uncertainty.

The streaming giant’s core subscription business remains the key catalyst. Netflix continues to attract and retain subscribers worldwide, strengthening its competitive position. At the same time, its newer ad-supported subscription tier is steadily gaining traction with consumers. Together, these two growth drivers are supporting the company’s expansion strategy and could contribute to another solid quarterly performance.

Options market activity indicates that investors are preparing for a potentially meaningful stock move following the earnings release. Current options pricing suggests an expected post-earnings swing of approximately 6.3% in either direction for contracts expiring on April 24. The expected move is higher than Netflix’s average earnings-related fluctuation of about 4.7% over the previous four quarters.

Notably, Netflix’s recent earnings reactions show some downside pressure. NFLX shares declined after the earnings release in three of the past four quarters, highlighting the possibility of volatility around the upcoming announcement, even if underlying business fundamentals remain stable.

Netflix Q1 Preview: Content, Pricing Power, and Ads Set to Drive Growth

Netflix is expected to deliver a solid Q1 performance, supported by expanding membership, higher pricing, and increasing advertising revenue. Notably, the streaming giant recently raised prices across all subscription tiers in the U.S., a move that is likely to strengthen both revenue and earnings in the coming quarters.

A major factor supporting this pricing power is Netflix’s expansive content library. High-quality programming drives user engagement, enables the company to implement price increases, and strengthens its competitive positioning.

For Q1, Netflix expects revenue to reach approximately $12.16 billion, representing year-over-year (YOY) growth of about 15%. The Q1 revenue is likely to benefit from compelling content, continued subscriber growth, and higher pricing.

Advertising is also emerging as a meaningful component of Netflix’s growth strategy. Since launching its ad-supported subscription tier, the company has broadened its revenue base by attracting price-sensitive viewers while opening a new channel for advertisers. Advertising revenue reached approximately $1.5 billion in 2025, and management is targeting roughly $3 billion in ad sales by 2026, reflecting the rapid expansion of this segment.

Alongside its growth initiatives, Netflix is focused on profitability. Management is targeting operating margins of about 31.5% in 2026, representing an improvement of roughly 200 basis points from the previous year. This margin expansion is expected to be supported by cost management, with content spending growing at a slower pace than overall revenue.

For the first quarter specifically, Netflix anticipates operating margins of approximately 32.1%, up about 40 basis points YOY. Earnings are projected to reach $0.76 per share, representing growth of more than 15% YOY.

Analysts’ earnings estimates are aligned with the company’s guidance. Notably, Netflix has exceeded analysts’ EPS expectations in three of the past four quarters, strengthening confidence in the company’s execution and ability to expand profitably.

What Do Analysts Think of Netflix Stock?

Netflix’s growing member base, ability to raise prices, and momentum in its advertising business position it well to deliver strong earnings in the coming quarters.

From a valuation perspective, NFLX stock currently trades at approximately 32 times forward earnings. While this multiple reflects the company’s premium positioning within the streaming industry, it remains reasonable when viewed alongside expectations for continued EPS growth. Analysts expect Netflix’s EPS to rise by 26% in 2026, followed by 22% growth in 2027.

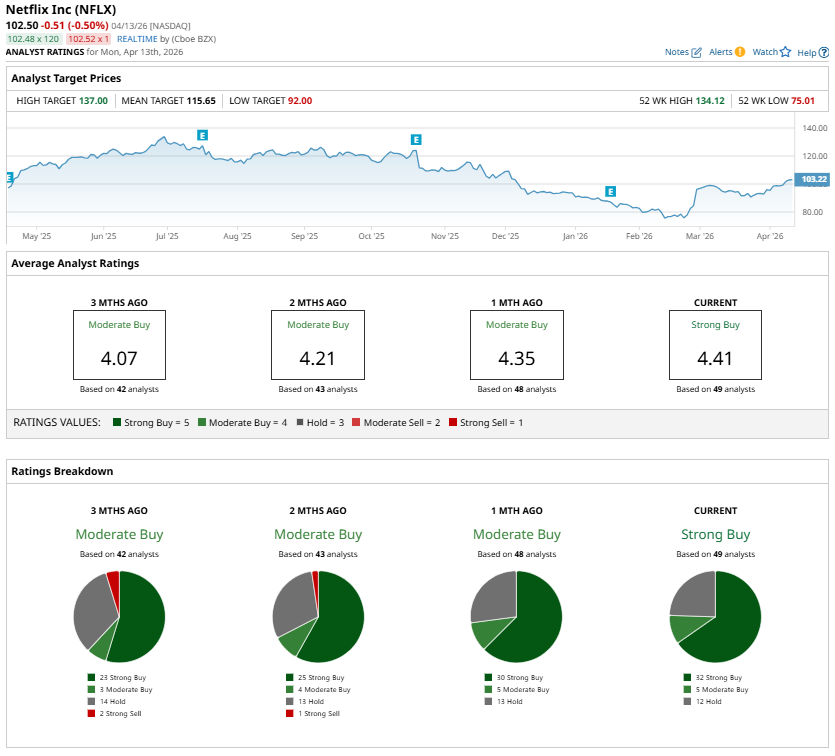

Wall Street analysts maintain a “Strong Buy” consensus rating on Netflix ahead of Q1 earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)