/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock(1).jpg)

Tesla (TSLA) has not exactly started the year on the front foot. The stock has slid more than 29.26% from its 52-week high and dropped nearly 21% over the last three months. Thursday, Apr. 2, added insult to injury when shares sank 5.4% after a weak first-quarter fiscal 2026 delivery report, then slipped another 2.2% in the very next trading session.

In Q1 2026, Tesla managed to grow deliveries by 6% to 358,023 vehicles, yet still came up short of the 365,000 analysts had penciled in. The energy storage unit, which had carried a bit of a golden child reputation, stumbled badly with deployments of 8.8 GWh. The figure not only trailed the 10.4 GWh posted a year ago but also missed the 14.4 GWh consensus by a mile.

China, the world’s largest electric vehicle (EV) market, is adding another layer of complexity. Rising competition from domestic automakers is starting to erode Tesla’s footing, with retail sales declining despite “rising” headline figures, according to Electrek.

Wholesale numbers included vehicles rolling out of Giga Shanghai and heading to Asia and Europe, which conveniently glossed over softer demand at home. Strip that away, and the picture looks less flattering, with retail sales in China at 112,798 vehicles in Q1 compared to 134,607 a year earlier.

Tesla loyalists tend to shrug off these cracks and keep their eyes on the horizon. They are betting on autonomous driving, cybercabs, and robots, not just cars rolling off assembly lines. Still, as the core business is starting to wobble, it raises the obvious question of what investors should actually do with the stock.

About Tesla Stock

Tesla has built its name on EVs but has steadily branched into energy storage, solar, and software-driven services. The Austin, Texas-based company runs a tightly controlled, vertically integrated playbook, selling directly to customers while developing its own batteries, artificial intelligence (AI) systems, and charging network.

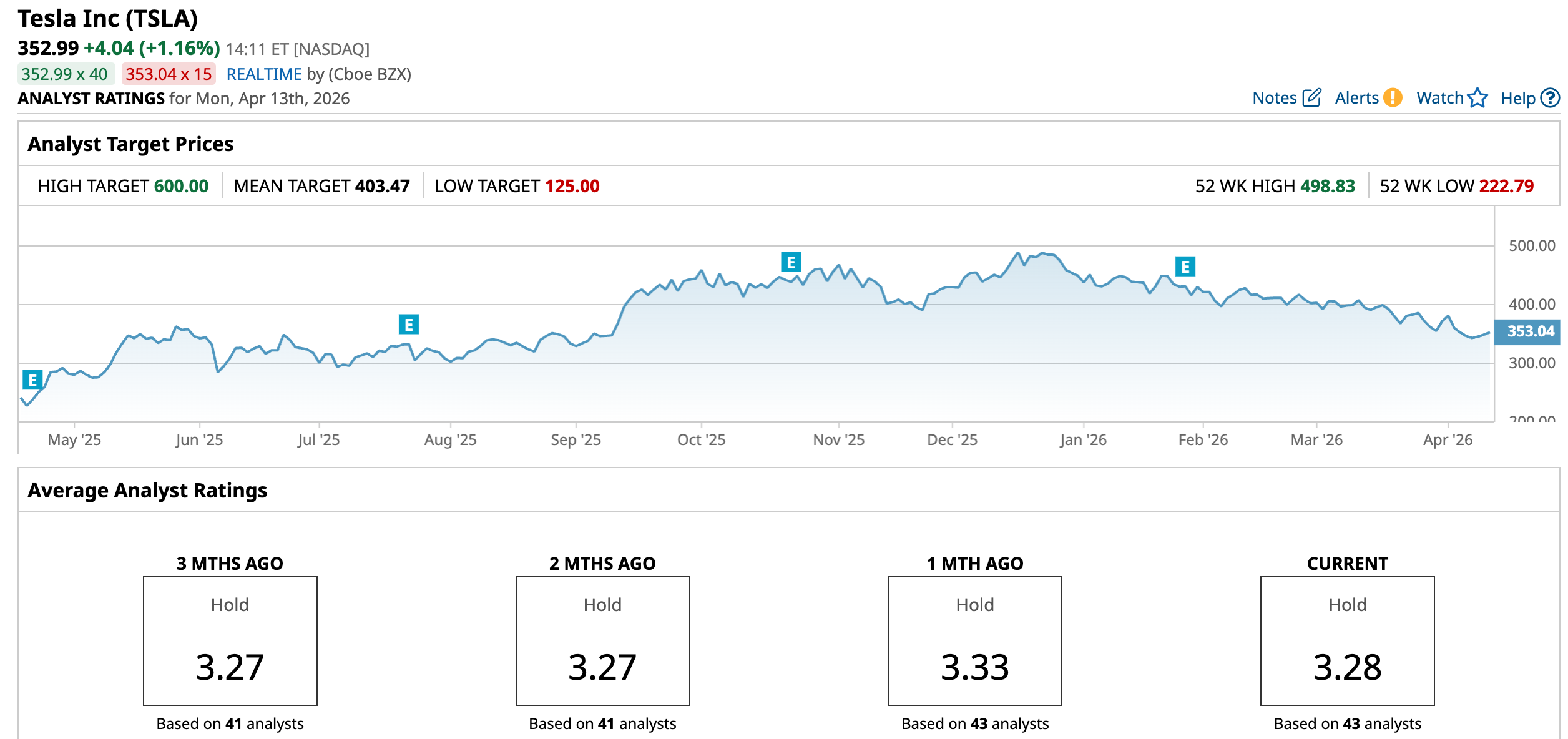

Tesla carries a market cap of approximately $1.3 trillion, reflecting both dominance and expectation. Over the past 52 weeks, the stock has gained 40.47%, though it has pulled back 21.2% on a year-to-date (YTD) basis, reflecting mounting near-term pressure.

Valuation only adds fuel to the fire. The stock is currently trading at 170.84 times forward adjusted earnings and 12.76 times sales. The figures sit at a clear premium, with the figures well above both industry peers and their own five-year historical averages, reflecting that the market has already baked in a lot of future success.

Tesla Surpasses Q4 Earnings

On Jan. 28, Tesla reported Q4 fiscal 2025 results that managed to beat expectations on both revenue and earnings. Revenue came in at $24.9 billion, down 3.1% year-over-year (YOY) but ahead of the $24.79 billion estimate. Adjusted EPS landed at $0.50, which fell 16.7% from the prior year but still cleared the $0.45 forecast.

Automotive dragged its feet and pulled total revenue lower, with sales in that segment dropping 10.6% YOY to $17.7 billion. Other segments stepped up to carry the load. Energy generation and storage revenue rose 25.4% to $3.9 billion, while services and other revenue jumped 18.4% to $3.4 billion.

Margins followed automotive down the hill. Adjusted EBITDA declined 4.1% to $4.1 billion, and non-GAAP net income fell 16.4% to $1.8 billion. Deliveries also slipped 15.6% to 418,227 units, reinforcing the sense that demand has cooled.

However, cash flow held the fort better than expected. Free cash flow reached $1.4 billion, and capital expenditures came in slightly below the earlier $9 billion guidance. The restraint will not last long. Management has already rolled up its sleeves for a heavy spending phase, with CapEx set to exceed $20 billion.

Tesla plans to bankroll six major facilities, including a refinery, an LFP factory, Cybercab, Semi, a new Megafactory, and the Optimus factory. At the same time, it continues to pour money into AI computer infrastructure while scaling Robotaxi and Optimus deployments.

The next checkpoint arrives on Apr. 22, when Tesla reports Q1 fiscal 2026 earnings after the closing bell. Analysts expect EPS for the quarter to jump 46.7% YOY to $0.22. For the full fiscal year 2026, they see earnings rising 28.4% to $1.40, followed by another 39.3% climb to $1.95 in fiscal year 2027.

What Do Analysts Expect for Tesla Stock?

Wall Street, for its part, cannot seem to agree on which way this story goes. JPMorgan analyst Ryan Brinkman has taken a notably bearish stance, sticking to a $145 price target and an “Underweight” rating after the delivery miss.

On the other hand, Baird analyst Ben Kallo trimmed his target from $548 to $538, a 1.8% cut, yet kept an “Outperform” rating, suggesting he still sees plenty of road ahead.

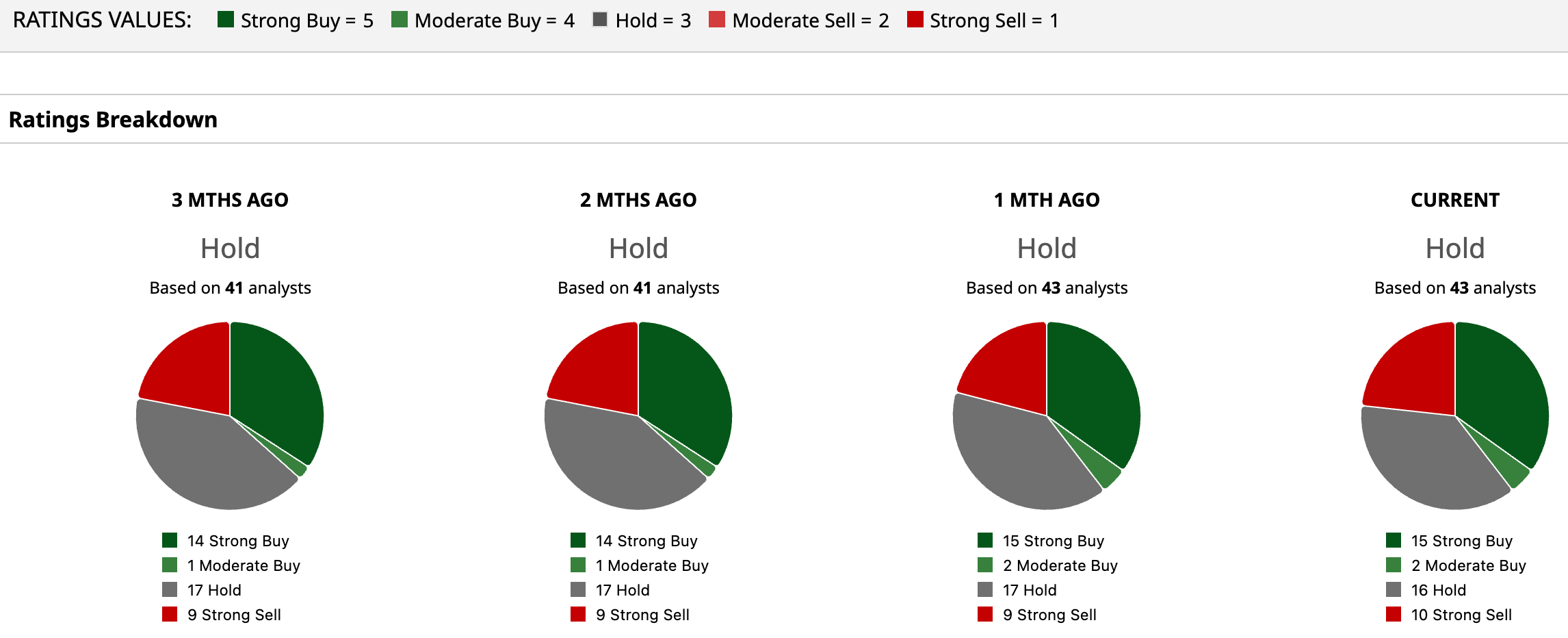

Across the broader analyst crowd, the stock lands in “Hold” territory. Among 43 analysts covering the stock, 15 have rated it a “Strong Buy,” two suggest “Moderate Buy,” 16 opt to “Hold,” while 10 have flagged a “Strong Sell.”

Even so, optimism continues to underpin sentiment. The mean price target of $403.47 points to an implied upside of 14.3%, while the Street high target of $600, set by Wedbush analyst Daniel Ives, suggests a potential gain of 70% from current levels. He maintains an “Outperform” rating, reflecting sustained confidence in Tesla’s long-term growth trajectory.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)