With a market cap of $83.6 billion, American Tower Corporation (AMT) is a global real estate investment trust that owns and operates wireless communication infrastructure, including cell towers, rooftop sites, and data centers across multiple continents. With strong exposure to long-term trends like rising mobile data usage and 5G expansion, AMT is widely viewed as a high-quality infrastructure play with durable growth potential.

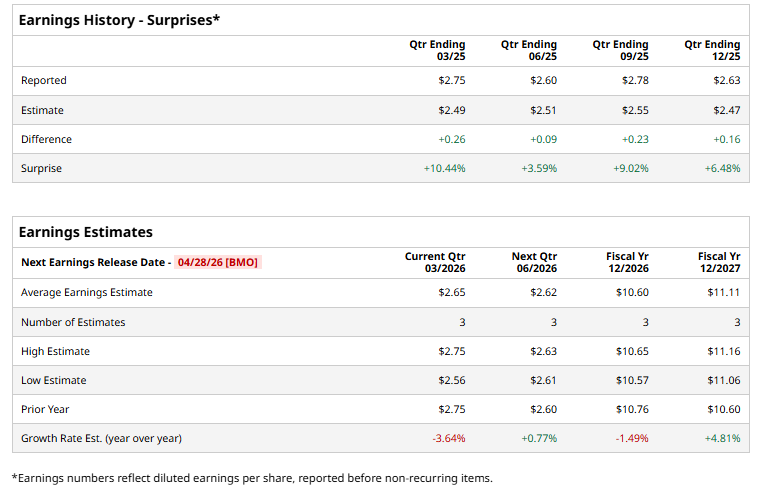

The Massachusetts-based REIT is expected to release its fiscal Q1 2026 results before the market opens on Tuesday, Apr. 28. Ahead of this event, analysts project AMT to report an AFFO of $2.65 per share, a 3.6% dip from $2.75 per share in the year-ago quarter. It holds a solid track record of consistently surpassing Wall Street's bottom-line estimates in the last four quarterly reports.

For fiscal 2026, analysts forecast the wireless infrastructure provider to report an AFFO of $10.60 per share, down 1.5% from $10.76 per share in fiscal 2025. However, AFFO is expected to grow 4.8% year over year to $11.11 per share in fiscal 2027.

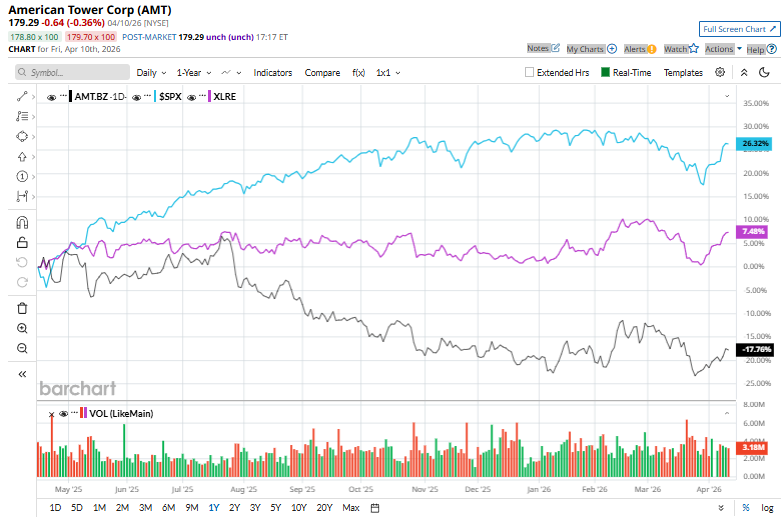

Shares of American Tower have declined 13.9% over the past 52 weeks, underperforming the broader S&P 500 Index's ($SPX) 29.4% gain and the State Street Real Estate Select Sector SPDR ETF's (XLRE) 11.6% rise over the same time frame.

On Mar. 5, American Tower announced a quarterly cash distribution of $1.79 per share, reinforcing the company’s commitment to returning capital to shareholders through consistent dividends. This payout reflects AMT’s stable, recurring cash flow model, driven by long-term leasing contracts with telecom operators. The dividend will be paid on April 28, 2026, to shareholders who are on record as of the close of business on April 14, 2026.

Analysts' consensus view on AMT stock is cautiously optimistic, with a "Moderate Buy" rating overall. Among 24 analysts covering the stock, 15 suggest a "Strong Buy," one gives a "Moderate Buy," and eight recommend a "Hold." The average analyst price target for American Tower is $219.45, indicating a potential upside of 19.7% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Quantum%20Computing/A%20concept%20image%20showing%20a%20ray%20of%20light%20passing%20through%20cyberspace_%20Image%20by%20metamorworks%20via%20Shutterstock_.jpg)

/International%20Business%20Machines%20Corp_%20logo%20on%20storage%20rack-by%20Nick%20N%20A%20via%20Shutterstock.jpg)