SanDisk (SNDK) stock has rallied significantly in recent months, delivering outsized gains despite ongoing geopolitical tensions. Even with the introduction of Alphabet’s (GOOG) (GOOGL) TurboQuant compression algorithm, designed to reduce memory requirements for artificial intelligence (AI) models, investor sentiment toward SanDisk has remained positive.

SNDK shares have climbed about 259% year-to-date (YTD) and have surged more than 629% over the past six months. The rally in SNDK stock is being driven by the rapid build-out of AI-focused data centers, which has significantly increased demand for NAND flash memory. As a major supplier of NAND solutions, SanDisk has benefited from this surge in infrastructure spending related to AI workloads.

At the same time, favorable supply dynamics within the global memory market have strengthened the company’s pricing power. Limited supply across the industry has allowed SanDisk to command higher prices for its products, contributing to expanding margins and improving profitability. These supply constraints, combined with sustained demand from AI infrastructure, have played a key role in supporting the company’s sharp share-price appreciation.

Looking ahead, SanDisk will report its third-quarter fiscal 2026 earnings on April 30. Strong demand and higher pricing are likely to power its Q3 financials and share price.

SanDisk's Q3: Here’s What to Expect

SanDisk has experienced a strong rally in its stock price, and the continued momentum in its underlying business suggests additional upside potential. For the upcoming third quarter, the company has guided revenue in the range of $4.4 billion to $4.8 billion. This outlook implies sequential growth of approximately 45% to 58%, representing a significant acceleration compared with recent quarters. By comparison, SanDisk reported second-quarter revenue of $3.03 billion, which increased 31% sequentially and 61% year-over-year (YoY).

The anticipated growth in SanDisk’s top line is expected to be supported primarily by higher pricing across its product segments. Pricing strength has emerged amid tight supply conditions in the memory market. In YoY revenue growth.

Profitability is also projected to improve meaningfully. SanDisk expects adjusted gross margins to fall within a range of 65% to 67%, representing a substantial increase from both the previous quarter and the same period last year. In the second quarter, the company reported an adjusted gross margin of 51.1%, a sharp improvement from 29.9% in the prior quarter, driven largely by stronger pricing. Ongoing reductions in unit production costs are also expected to contribute to further margin expansion.

Stronger revenue and expanding margins are likely to translate into significant bottom-line growth. SanDisk has projected adjusted earnings per share of $12 to $14 for the third quarter. At the midpoint of this guidance, earnings would more than double sequentially, highlighting the strong operating leverage in the company’s current business cycle.

Is SNDK Stock a Buy Before April 30?

SanDisk stock’s outlook ahead of April 30 remains positive. The company continues to benefit from a favorable NAND memory environment led by sustained demand, a growing customer base, and higher pricing. These dynamics are helping drive margin expansion, positioning SanDisk to deliver robust third-quarter growth and potentially support further gains in its share price.

From a valuation perspective, the stock also appears attractive relative to its earnings growth trajectory. SNDK’s forward price-to-earnings ratio of 18.5 remains reasonable given the company’s solid earnings growth. Analysts expect a significant jump in profitability, with EPS forecasted to surge by more than 2,000% in fiscal 2026. This is expected to be followed by another year of significant expansion in fiscal 2027, when the company’s bottom line is projected to more than double. Such a strong earnings growth projection suggests further upside for SNDK stock.

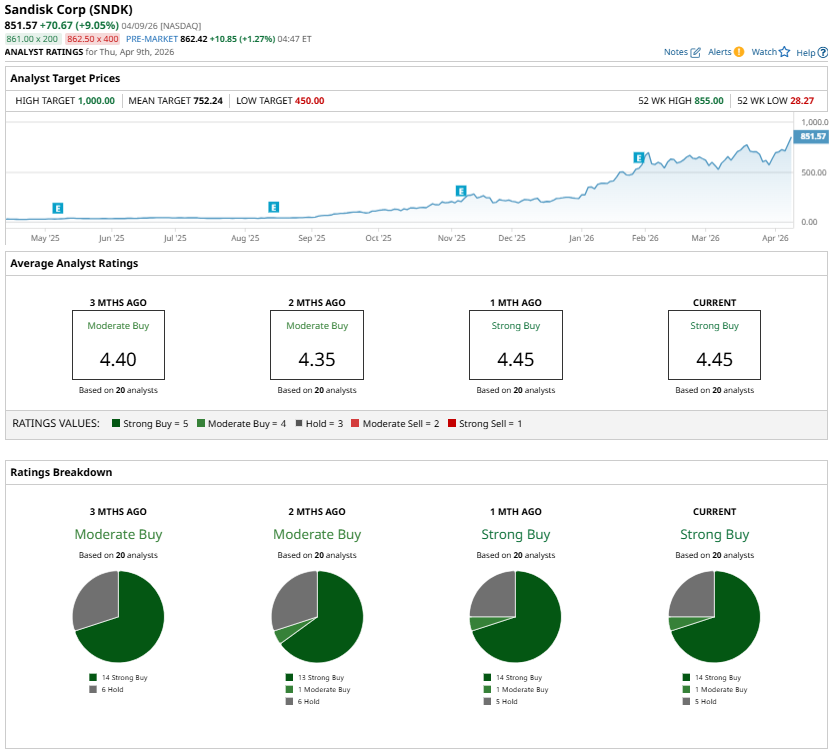

Analysts’ sentiment toward the stock remains positive despite its recent rally. Wall Street continues to maintain a consensus “Strong Buy” rating, reflecting confidence in NAND demand's ongoing strength and sustained pricing momentum. With industry fundamentals remaining supportive and profitability expected to improve significantly, SanDisk appears well-positioned to maintain its growth trajectory in Q3, making its stock a buy.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)