/AI%20(artificial%20intelligence)/Close-%20up%20of%20computer%20chip%20with%20AI%20sign%20by%20YAKOBCHUK%20V%20via%20Shutterstock.jpg)

Taiwan Semiconductor Manufacturing Company (TSMC) (TSM), the world’s leading semiconductor foundry, ended 2025 on a solid note, fueled by surging demand for advanced nodes and AI accelerators. While the company will report its first-quarter earnings report on April 16, it provided an early glimpse with preliminary Q1 revenue growth of 35%, showing the strength of the current AI cycle. TSM stock has surged 23% year-to-date (YTD) and 147% over the past 52 weeks, outperforming the broader market.

With massive capital spending, margin pressures from global expansion, and the ramp-up of next-generation technologies, the Q1 report will reveal if TSM stock still has room to run.

AI Demand Continues to Power TSMC’s Growth

Valued at $1.6 trillion, TSMC is the world’s largest pure-play semiconductor foundry. Instead of designing its own chips, it manufactures chips designed by other companies. TSMC specializes in cutting-edge manufacturing nodes like 3nm and 5nm, which are among the most advanced in the world. It is the leading supplier to tech titans like Apple (AAPL), AMD (AMD), Nvidia (NVDA), Qualcomm (QCOM), and Broadcom (AVGO).

For the full year 2025, TSMC’s revenue surged 35.9% year-over-year (YoY) to $122 billion. Adjusted earnings per share (EPS) jumped 46.4%, while gross margin expanded close to 60%, driven by both strong demand and disciplined cost execution. High-performance computing (HPC) accounted for 58% of revenue and grew 48% YoY. Smartphones remained a significant contributor at 29%, while IoT and automotive segments also reported double-digit growth.

The explosive growth of AI is the driving force behind TSMC. Management highlighted that the company is not only seeing demand from direct customers but also from their customers. It now forecasts AI accelerator revenue to grow at a mid-to-high 50% compound annual growth rate until 2029. This layered demand highlights TSMC's critical role in the AI ecosystem.

2026 Outlook: Growth Remains Strong, but Costs Are Rising

For the first quarter, the company reported preliminary Q1 revenue of $35.71 billion, marking a strong 35% YoY increase and landing at the high end of its previously guided $34.6 billion to $35.8 billion range. Notably, March alone delivered a 45.2% YoY increase in revenue and 30.7% sequentially, signaling accelerating demand into the quarter’s close. Overall, the preliminary numbers suggest TSMC is entering 2026 with strong top-line momentum, highlighting the strength of AI-driven demand despite broader macro uncertainties.

For the full year, TSMC remains highly optimistic as it expects the foundry 2.0 industry to grow 14% YoY. The company’s revenue could increase by 30% for the year to $158 billion, aligning with consensus estimates. However, the company also expects capital spending to increase to between $52 billion and $56 billion, up from $40.9 billion in 2025.

TSMC expects 70% to 80% of this to go towards advanced process technologies, reflecting the company’s aggressive push to maintain its technological lead. It has already begun high-volume production of its two-nanometer (N2) technology and intends to deploy upgrades such as N2P and the A16 node, both of which are expected to boost performance and efficiency.

Analysts that cover TSMC also expect earnings to increase by 38.3% in 2026 to $14.73 per share, followed by 22.6% in 2027 to $18.06 per share. Trading at 24x forward earnings, TSM appears to be a reasonable AI stock to buy now.

The Key Takeaway Before Earnings Release

TSMC is not just another semiconductor company. When it comes to advanced chip manufacturing, TSMC is years ahead of most competitors like Intel (INTC) and Samsung (SMSN.L.EB). This dominance gives TSMC pricing power, long-term contracts, and deep customer dependency. The fact that no other manufacturer can fully replace it today provides TSMC with a competitive advantage, which is essential in this highly competitive and crowded AI space.

However, investors shouldn’t completely forget the risks. Rising capital expenditures, margin dilution from global expansion, and the increasing cost of advanced nodes could weigh on profitability in the near term. With revenue expected to grow close to 30% in 2026 and AI demand showing no signs of slowing, TSMC appears well-positioned for long-term growth. The stock is down 6.3% from its 52-week high of $390.20, making it a good opportunity to buy it on the dip.

What’s the Word on the Street About TSM Stock?

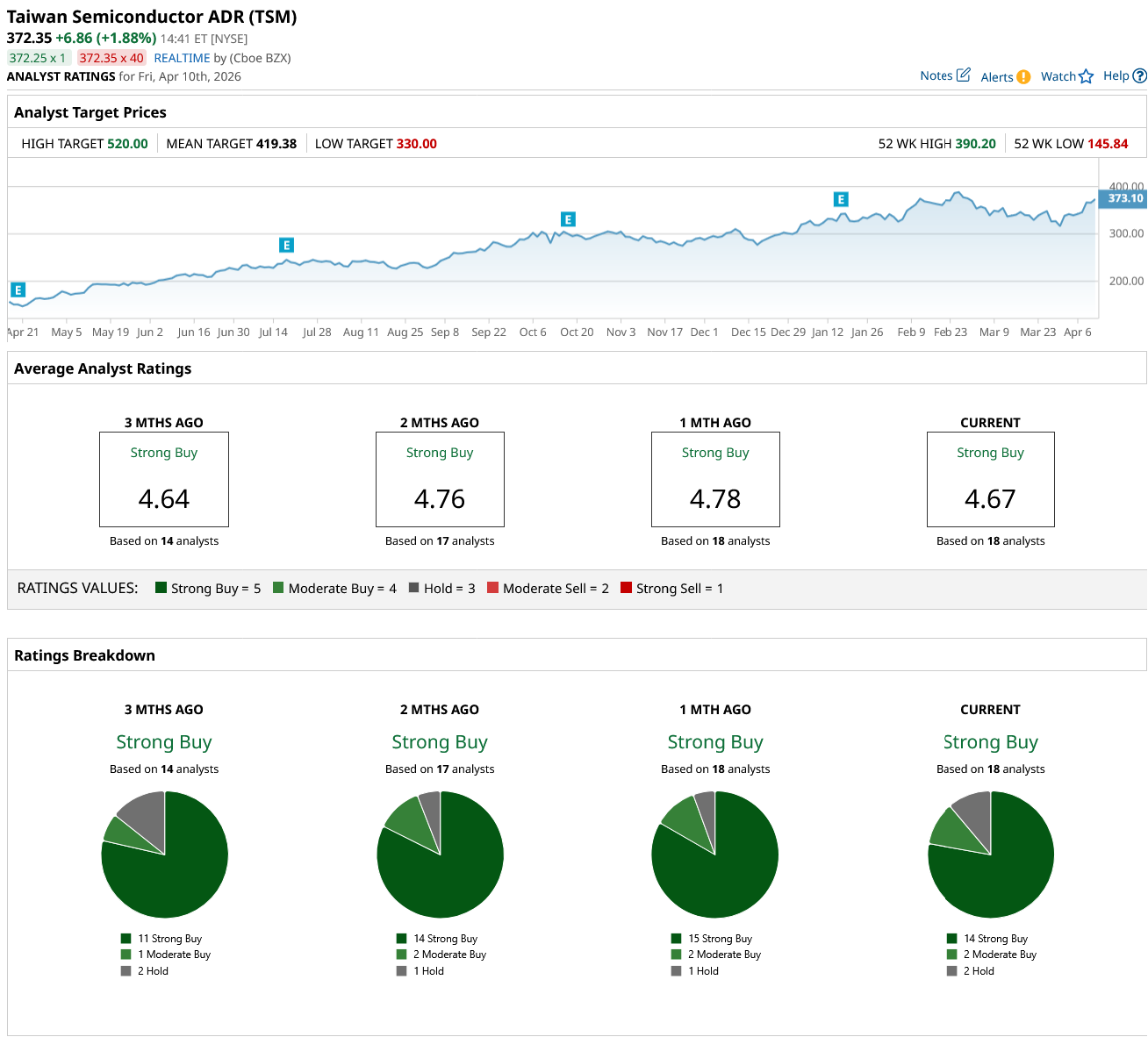

Overall, on Wall Street, TSM stock holds a consensus “Strong Buy” rating. Out of the 18 analysts that cover the stock, 14 rate it a “Strong Buy,” two say it is a “Moderate Buy,” and two rate it a “Hold.” Based on the average price target of $419.38, the stock has an upside potential of 13% from current levels. Plus, its high target price of $520 implies a potential upside of 40% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)