/A%20close-up%20shot%20of%20the%20Taiwan%20Semi%20logo%20on%20a%20corporate%20building%20by%20Jack%20Hong%20via%20Shutterstock.jpg)

The AI boom shows no signs of cooling. Data centers worldwide added capacity at a record clip in early 2026, with high-performance computing chips leading the charge. Chip designers like Nvidia (NVDA) and Advanced Micro Devices (AMD) keep placing massive orders, yet the one company that actually manufactures these advanced processors trades as if the party might end tomorrow.

That company is Taiwan Semiconductor Manufacturing (TSM). The company recently released its preliminary first-quarter 2026 revenue figures, and they deliver a clear message: this AI foundry leader just posted numbers too strong to dismiss, and at a valuation that makes it hard to ignore.

Q1 Revenue Shatters Expectations

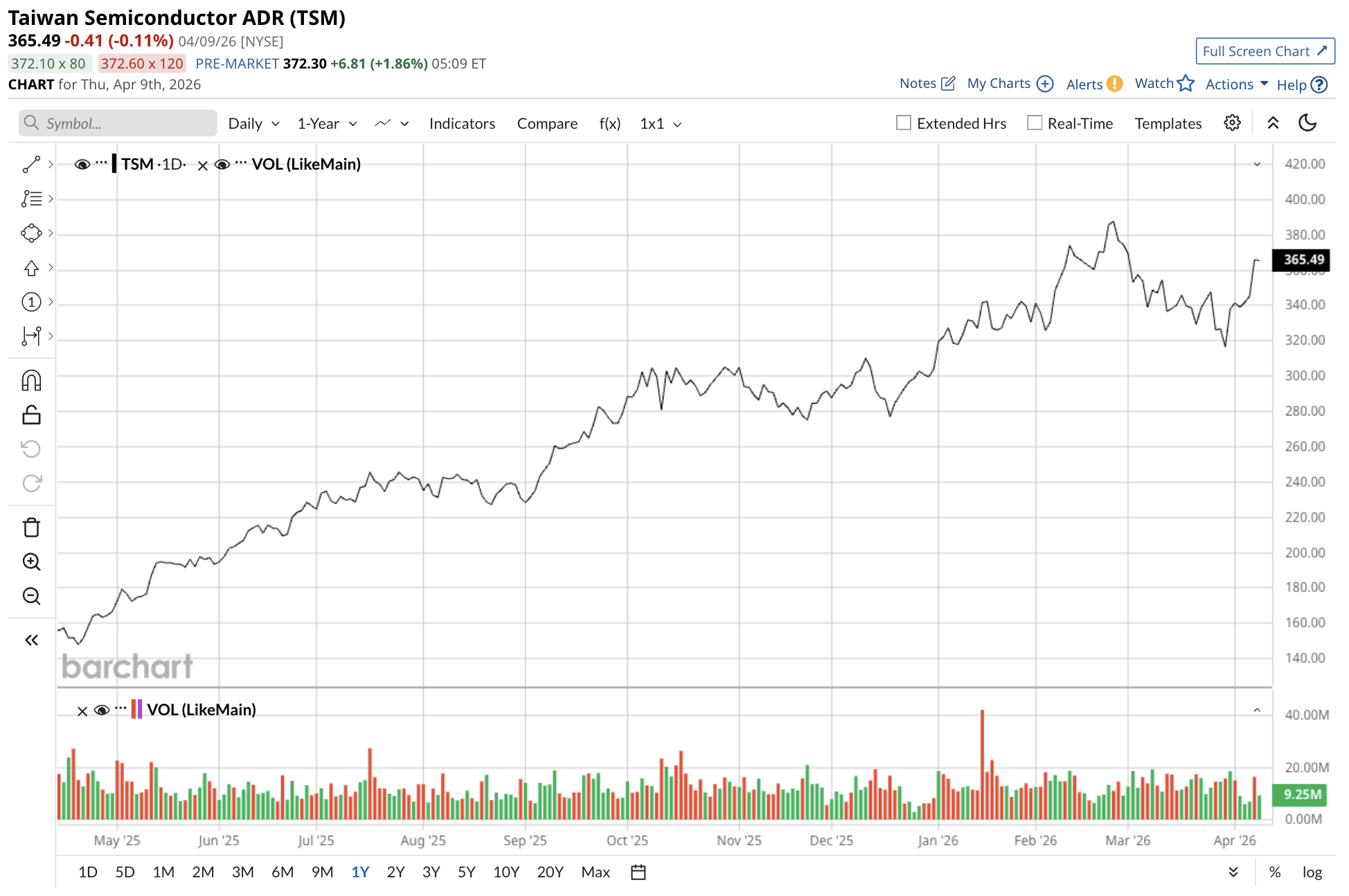

Taiwan Semicondutor reported Q1 revenue of $35.71 billion, up 35% year-over-year (YOY) from the prior-year period. That beat LSEG SmartEstimate forecasts of roughly $35.4 billion. March alone delivered $13.07 billion in sales, a more than 45% jump from March 2025 and a nearly 31% sequential gain from February. For context, Taiwan Semiconductor's Q4 2025 revenue stood at $33.73 billion. The acceleration came despite ongoing capacity ramps and geopolitical headlines.

Let's put the growth in perspective with a side-by-side look:

- Q1 2026 revenue: $35.71 billion, up 35% YOY

- Consensus estimate: $35.4 billion

- Q1 2025 revenue: $25.5 billion

- Full-year 2026 guidance: 30% revenue growth in USD terms, based on the Q4 2025 earnings call

No matter how you slice it, Taiwan Semiconductor outpaced both its own prior pace and Wall Street expectations. That 35% clip marks the latest chapter in a string of beats fueled by advanced nodes (3 nanometer (nm) and below), which now command premium pricing and higher margins.

While Taiwan Semiconductor didn't provide preliminary earnings, analyst estimates are looking for $3.29 per share. Considering the revenue growth, that figure may undershoot the mark. The company will reports its full quarterly results on April 16.

AI Demand Powers the Engine

High-performance computing (HPC) — the segment that includes AI accelerators — now accounts for the majority of TSM's wafer revenue. Management previously lifted its long-term HPC compound annual growth rate (CAGR) outlook to 26% to 29% through 2029, up from an earlier mid-40% range for AI accelerators specifically.

In the Q4 2025 call, management noted that the shift to HPC is complete, with AI-related demand visible across enterprise and hyperscale customers. TSM's share of the advanced foundry market means it captures the bulk of that spend. Competitors like Samsung and Intel (INTC) trail in both yield and capacity at the leading edge.

That said, capital expenditures remain elevated. TSM guided for 2026 capex of $52 billion to $56 billion to support 2nm and CoWoS advanced packaging ramps. Yet gross margins have held firm in recent quarters — 62.3% in Q4 2025, above the 59% to 61% guidance range — while Q1 2026 guidance called for gross margins of 63% to 65%. The numbers show pricing power more than offsets the spending.

Valuation Screams Opportunity

Here's where the story gets interesting for retail investors. Despite the blowout growth, TSM stock trades at a forward price-to-earnings (P/E) ratio of 25.3 times. That sits below the semiconductor industry median forward P/E of 29.4 times. For comparison, Nvidia's forward P/E sits at 23.5 times, while Micron's (MU) forward multiples sits at 7 times but with slower AI exposure.

Taiwan Semiconductor's trailing P/E sits around 34 times, but the forward multiple reflects expected 30% revenue growth for 2026 and a sustained 25% CAGR through 2029. TSM stock also yields 0.81% on its dividend, with a history of steady increases. Granted, Taiwan-based operations carry geopolitical risk, and currency swings can matter. Yet the company has navigated these issues for decades while expanding U.S. and Japanese fabs.

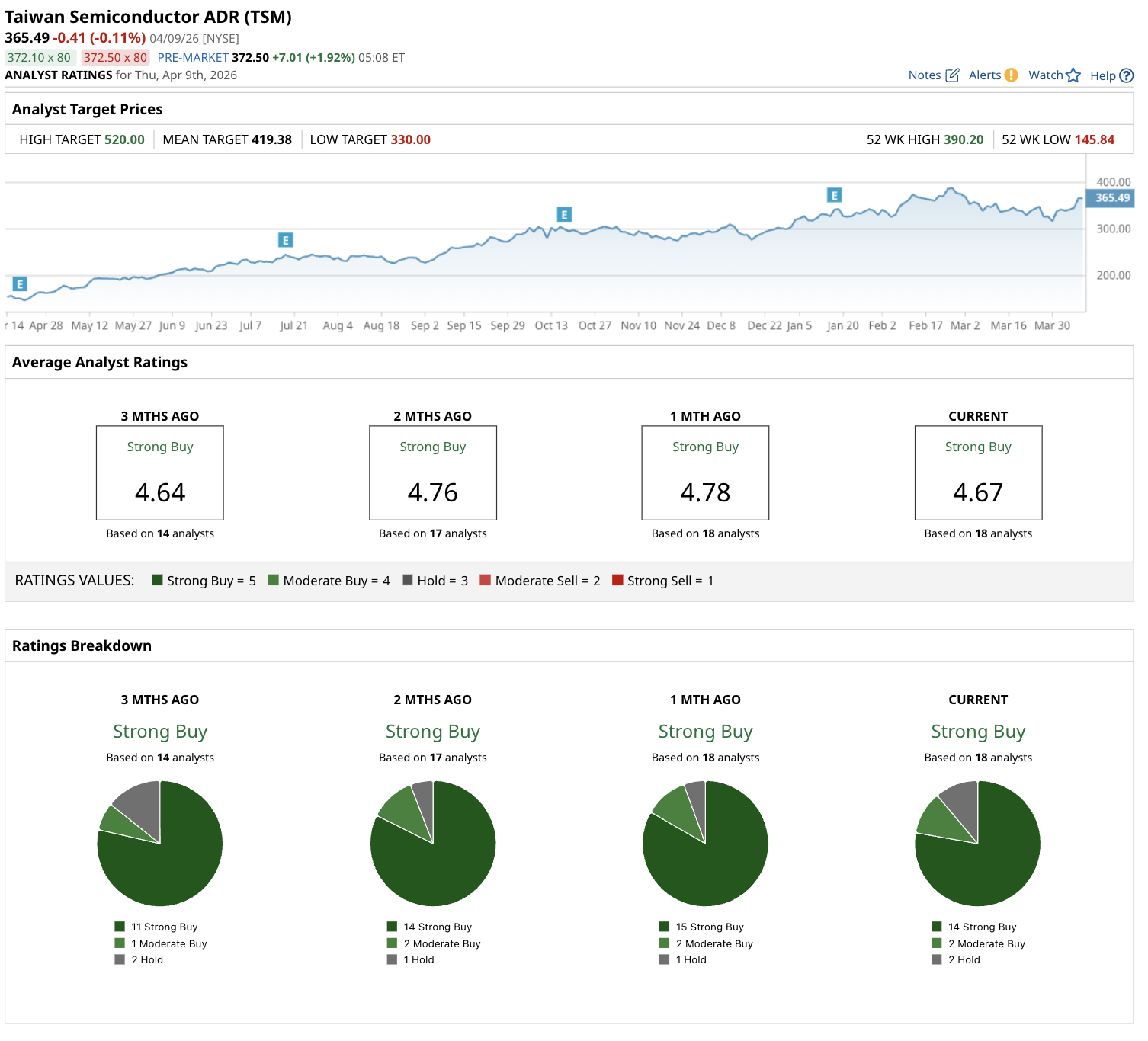

Wall Street Remains Bullish on TSM Stock

Analysts continue to have a “Strong Buy” consensus rating for TSM stock. Of the 18 analysts with coverage, 14 analysts have a "Strong Buy" rating, two analysts have a "Moderate Buy" rating, and two rate TSM stock as a “Hold.”

The mean price target of $419.38 implies potential upside of 12% from current levels. Targets range from a Street-high of $520 to a low target of $330, indicating there is little downside risk.

The Key Takeaway

When all is said and done, Taiwan Semiconductor's Q1 revenue surge confirms that AI demand remains structural, not cyclical. At a forward P/E competitive with its peers and with unmatched scale in advanced nodes, TSM stock offers a rare combination of growth and margin resilience.

Savvy investors should view any dip in TSM stock as a chance to add shares. This isn't hype — it's math. Taiwan Semiconductor belongs in any long-term tech portfolio built for the AI decade ahead.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)