/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)

Everyone loves a comeback story, right? Well, maybe not in this case. I am not taking sides regarding the social debate and horrific recent history surrounding United Healthcare (UNH). However, I am doing what I always do: looking at stocks and ETFs and their charts. And sizing up risk of major loss, as well as return potential. Then merging them into what I hope is a balanced discussion of a stock that has been a hot topic for a couple of years.

UnitedHealth Group has long been the undisputed titan of the managed care world, a massive, vertically integrated engine that seemingly only knew how to grow. Not long ago, it was the single largest stock within the Dow Jones Industrial Average ETF (DIA), at more than 10%. That price-weighted index rewarded UNH reaching $600 a share with that accolade. But that was so 2024, right?

Since that time, the narrative has shifted from “growth at any cost” to a disciplined, almost defensive, focus on margin preservation. Oh, and the stock cratered, such that Tuesday morning’s more-than-10% pop still left UNH 50% below its all time high.

For those looking to play the potential recovery of this healthcare giant, there is a specialized vehicle that offers a broader way to capture this industry-wide pivot: the iShares U.S. Healthcare Providers ETF (IHF).

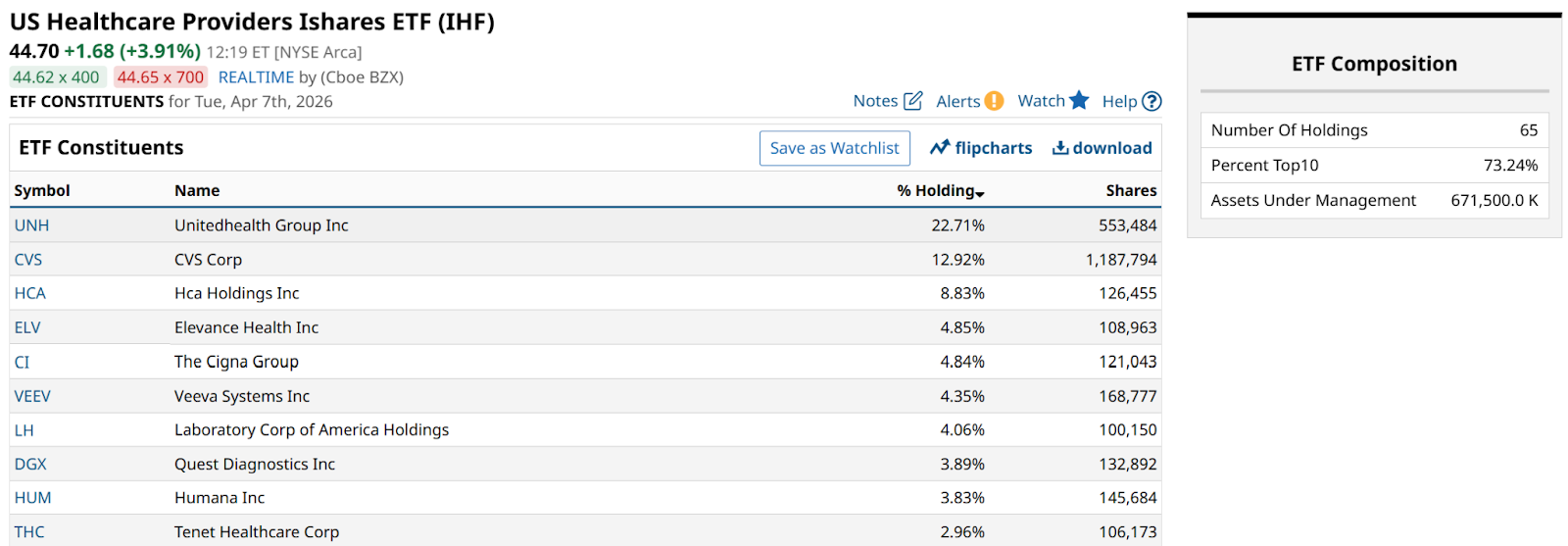

UNH is the cornerstone of the IHF basket, currently accounting for more than 22% percent of total ETF assets. This means that if you own IHF, you are making a concentrated bet on UnitedHealth, but you are also surrounding it with the other major players— CVS (CVS), HCA Holdings (HCA), Elevance (ELV), and Cigna (CI). All of these companies are navigating the same stormy regulatory waters.

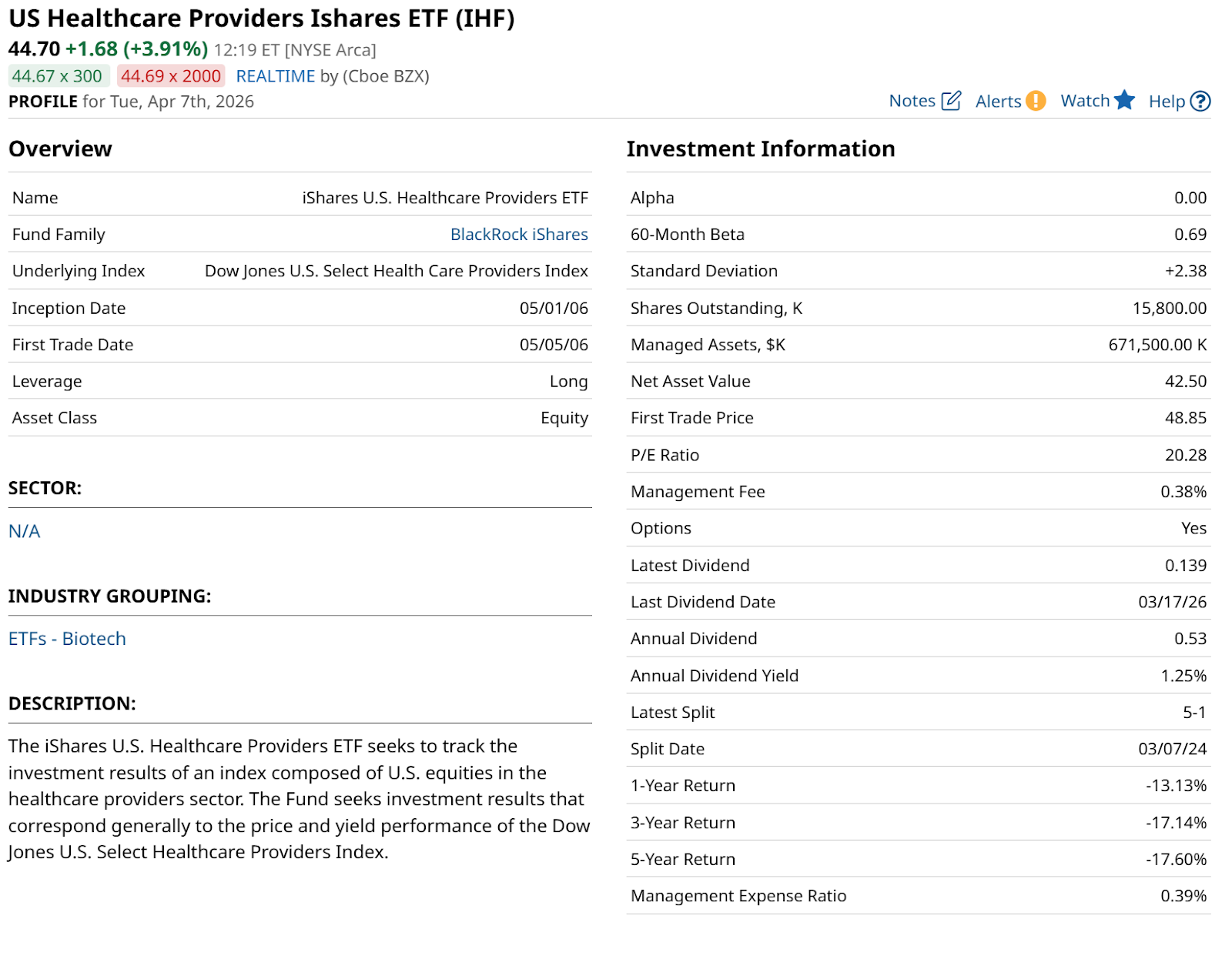

IHF is about to celebrate its 20th birthday. However, for the past 6 years of its existence, its price per share has remained the same, albeit with plenty of volatility in between.

The Case for the Comeback: Efficiency Over Expansion

The bullish narrative for UNH in 2026 is centered on a strategic retreat that could pave the way for a more profitable future. After a difficult 2025 defined by rising medical costs and the fallout from a major cyberattack, management has spent the first few months of this year “right-sizing.”

For the first time in decades, UNH is projecting a slight revenue decline as it exits over 100 counties and sheds unprofitable Medicaid contracts. The goal is simple: prioritize earnings quality over raw membership numbers.

The company is also aggressively leaning into artificial intelligence to automate administrative back-office tasks and improve clinical productivity at its Optum clinics. This financial rigor is expected to drive earnings growth of roughly 13% for fiscal 2027, even as the top line shrinks.

As a result of that market-driven reset in the stock price, UNH stock might now reflect much of the regulatory gloom. And remember, this is a company that still controls a massive portion of the American healthcare spend.

The bear case for UNH and thus, by extension IHF, is rooted in a hostile regulatory environment that hasn’t been this intense in over a decade.

The federal government has signaled a multi-year effort to claw back what it deems as overpayments to private insurers. Proposed reimbursement rate increases for 2027 are tracking well below medical inflation, forcing insurers to cut benefits and risk losing members to competitors or traditional Medicare. And, UNH is facing intense scrutiny on Capitol Hill. A recent Senate committee report accused the company of “gaming” the risk-adjustment system to inflate government payments. This headline risk, combined with ongoing Department of Justice antitrust inquiries into Optum’s vertical integration, remains a persistent overhang on the stock.

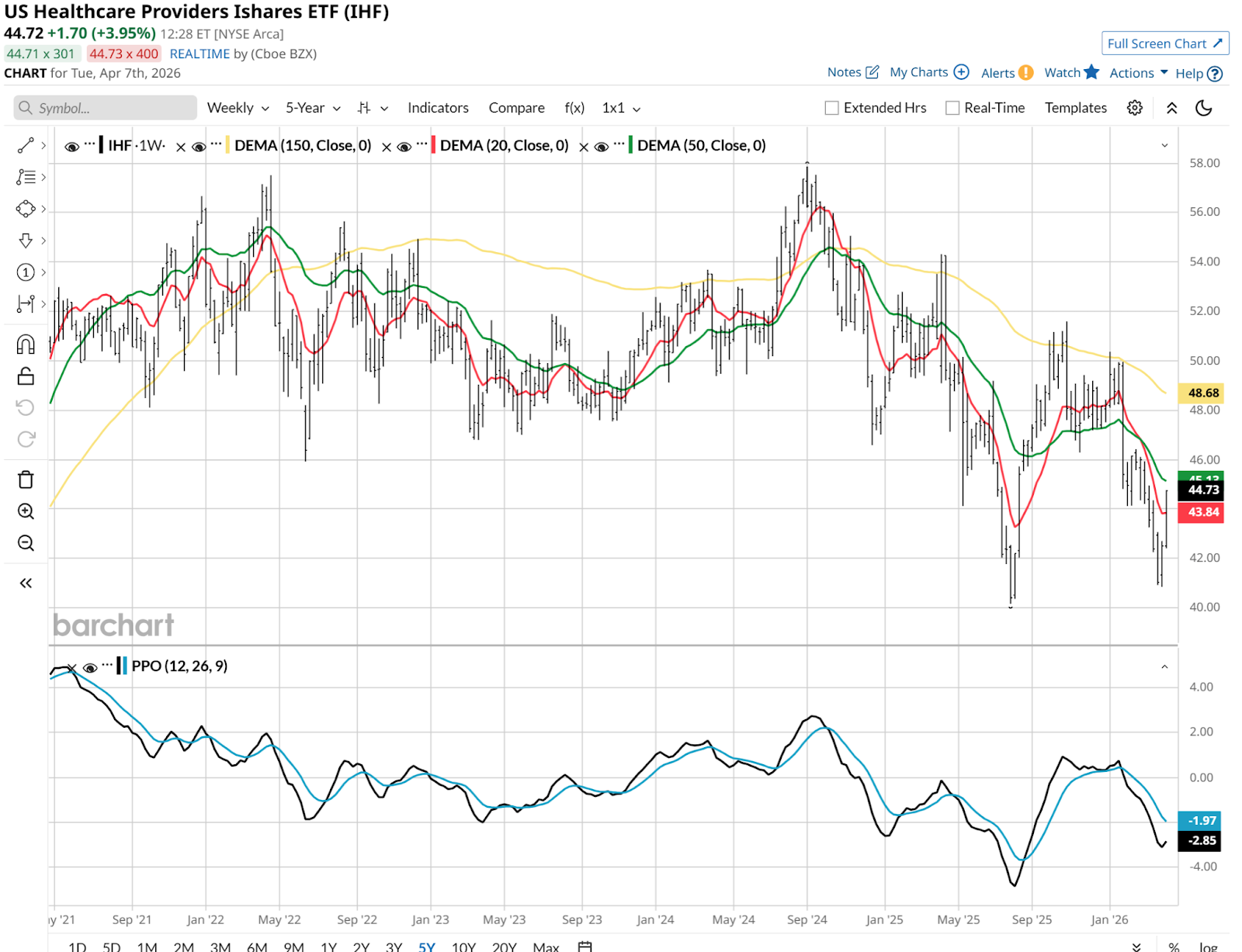

For me, it comes down to technicals. And for all investors, it comes down to how much risk you want to take, in any single position and across your portfolio. That’s why I’m showing IHF’s weekly chart above, for a longer look. Yes, UNH’s chart looks similar.

In both cases, the technical positive is a budding double-bottom, which for IHF is in the $40-$42 price range. However, the 20-week moving average still trends down. Bottom line: this is a good “watch and track” for me, looking forward to at some point being able to have enough conviction to add it to my portfolio.

ROAR Score View of IHF

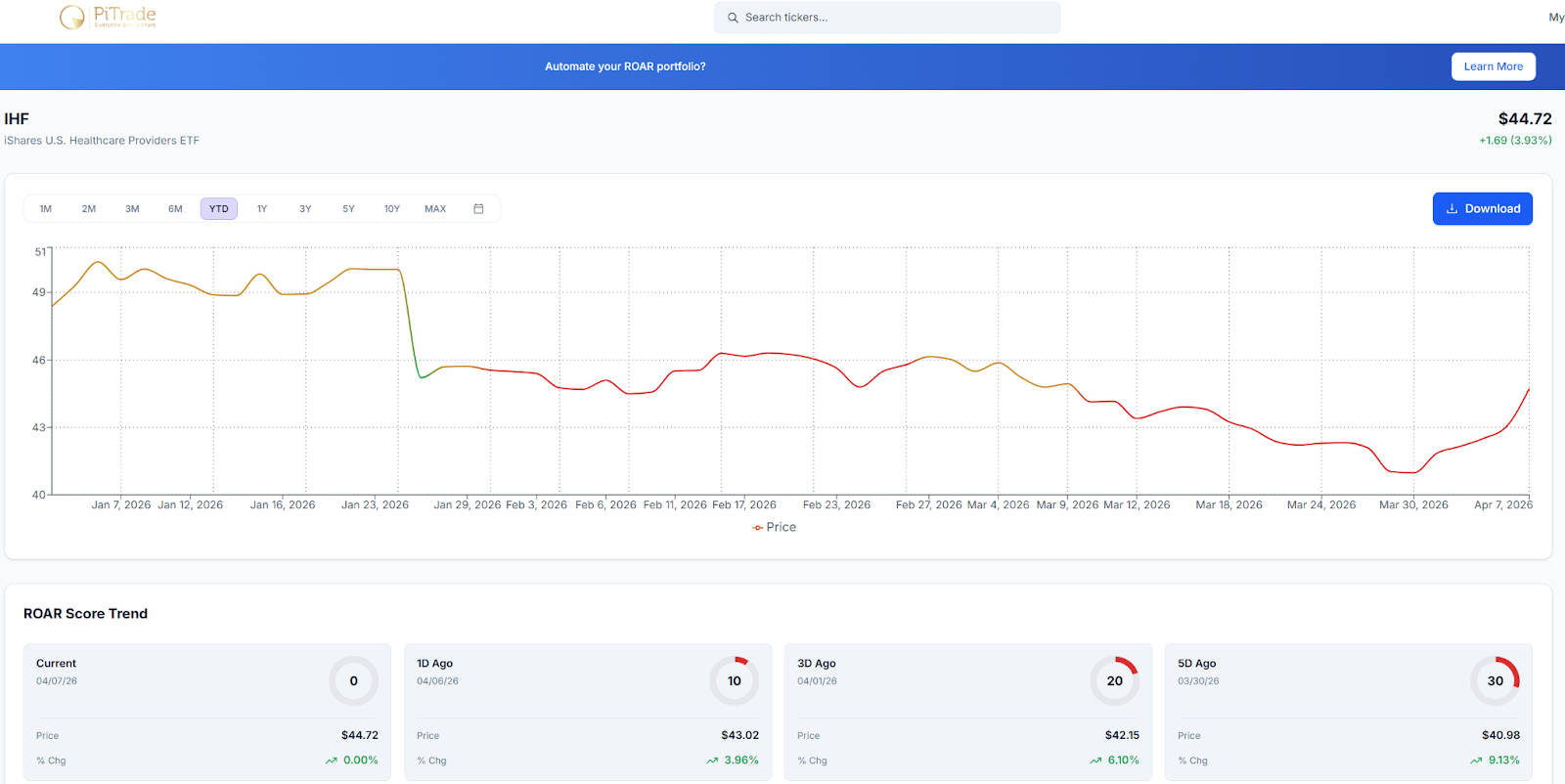

Investors and traders are confused by the seemingly endless whipsaw around the healthcare industry. And IHF’s ROAR Score reflects that. It is “fighting the rating” which actually stood at 0 momentarily, and has been below 40 for the past month.

That helped sidestep a 10% decline in IHF last month. And also reminds us that when a stock or ETF has a sharp bounce from the depths this one has been in, no technical system with a time horizon beyond that of a swing trader is going to adjust immediately. So the next few weeks will be a good “tell” here.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)