So far, the Iran war has relied on missiles and air power rather than ground forces, putting more attention on one of the Pentagon’s favored weapons: the Tomahawk cruise missile. Tomahawk missiles are manufactured by defense contractor RTX (RTX) through its subsidiary, Raytheon.

Reports indicate that the U.S. has fired more than 850 Tomahawk missiles in the war with Iran. The Center for Strategic and International Studies (CSIS) reports that Tomahawks are being used in the Iran war more than in any military campaign in history. “Replenishing inventory after this campaign will take time, and creates near-term risk for the United States,” the organization noted.

The missiles, which can be launched from ships and submarines and can strike targets within 1,000 miles, cost between $2 million and $3.5 million each and are the subject of several military contracts. RTX signed a $381 million contract in late January for Tomahawk missile work, and also received a $384 million modification to a previously awarded contract in December. On Feb. 4, the company also announced five framework agreements with the Pentagon to increase production and speed up deliveries of its Tomahawk missiles and other products.

With Tomahawk reserves reportedly dwindling, RTX and Raytheon appear to be a compelling investment for the near future. Even if the war winds down quickly, Raytheon will be hard at work replenishing U.S. reserves for the foreseeable future. And that will mean plenty of profits for RTX stock.

Let’s take a closer look..

About RTX Stock

RTX is the parent company of Raytheon, Collins Aerospace, and Pratt & Whitney. The company, which used to be known as Raytheon Technologies, is headquartered in Arlington, Virginia, which is strategically close to the Pentagon. RTX has a market capitalization of $267 billion.

Shares are up 67% in the last year, far outdistancing the S&P 500 ($SPX). But while defense stocks have enjoyed big returns in the last 12 months, RTX is notably outperforming many of its biggest competitors, including Lockheed Martin (LMT), General Dynamics (GD), and Northrop Grumman (NOC).

However, RTX stock’s rapid rise has coincided with an elevated valuation. The stock trades at a forward price-to-earnings (P/E) ratio of 28.8 times versus competitors all trading at 25 times or lower. Still, RTX is trading at roughly its 10-year mean, so shares are not outrageously priced at this point.

RTX also provides an annualized dividend of $2.72 per share. With a yield of 1.4%, the dividend provides an added incentive for holding RTX stock.

RTX Beats on Earnings

RTX reported a solid fourth quarter, with adjusted sales of $24.2 billion, up 12% from a year ago. Net income of $2.11 billion was up 2% from Q4 2024, while EPS of $1.55 beat analysts’ expectations for $1.46 per share. For full year 2025, RTX reported $88.6 billion in sales, up 10% year-over-year (YOY), and net income of $8.53 billion, up 11% YOY.

The Raytheon segment specifically accounted for $7.65 billion in sales in Q4, up 7% YOY. Operating profit from the segment was $885 million, up 7% from the same period last year.

"We enter 2026 with great momentum and are well positioned to deliver our 2026 financial outlook,” CEO Chris Calio said. “We remain focused on investing in new capabilities, expanding production capacity, and executing on our backlog to meet the growing needs of our customers."

The company issued guidance for 2026 sales between $92 billion and $93 billion, with EPS in the range of $6.60 to $6.80. The company will report Q1 2026 earnings on April 21.

What Do Analysts Expect for RTX Stock?

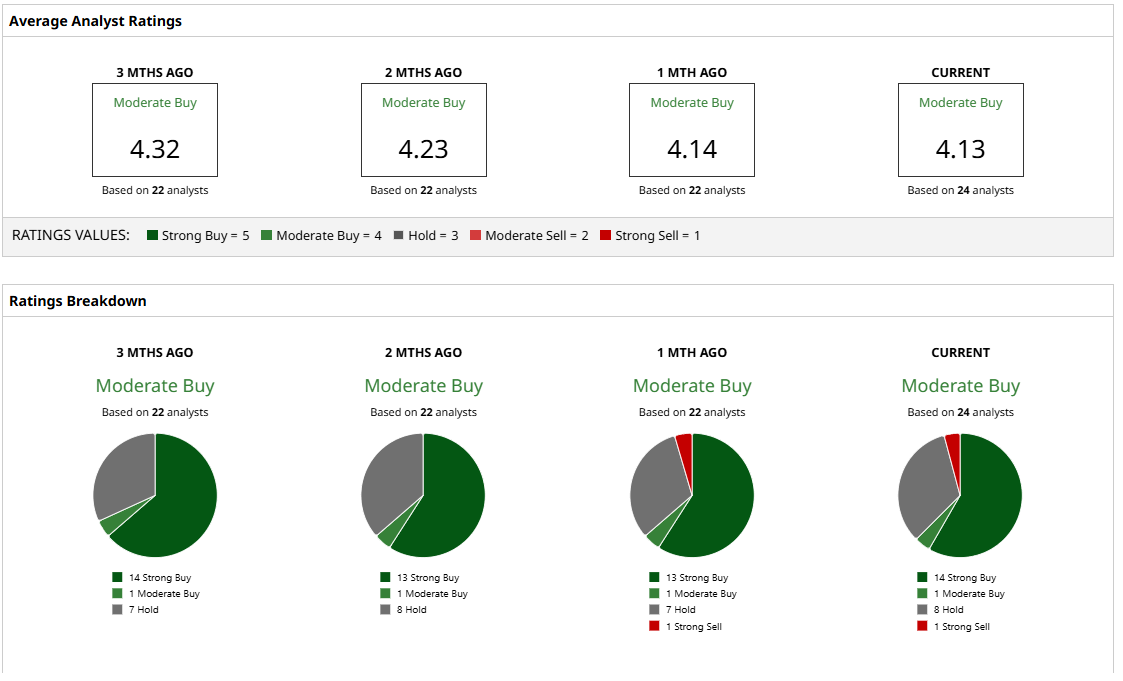

Analysts are consistently bullish on RTX stock. Based on 25 analysts with coverage, RTX has a “Moderate Buy” consensus rating. That consensus breaks down to 15 “Strong Buy” ratings, one “Moderate Buy,” eight “Hold” ratings, and one “Strong Sell” rating.

Analysts have a mean price target of $214.23, representing potential upside of 8% from current levels. The high price target of $240 indicates possible gains of 21%, while the low price of $160 warns of a potential 19% drop from here.

However, I’m more on the bullish side when it comes to RTX. The company makes the Pentagon’s favored cruise missile, and the military will need many more to replenish its stockpile used over the last month. For consistent profits, a solid dividend, and its key position as a defense contractor, RTX stock looks like a strong buy, even if the Iran war comes to a rapid conclusion.

On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)