/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

Once a key beneficiary of the artificial intelligence (AI) boom, Super Micro Computer (SMCI) rode the explosive wave of demand for storage and networking solutions built for data centers, cloud infrastructure, and enterprise AI. And for a while, it seemed like nothing could stop it. But that high-flying narrative has unraveled quite fast.

After already facing investor concerns over shady accounting practices and delayed filing of financial reports nearly two years ago, shares of Super Micro are once again under intense selling pressure this year, dragged down by a deepening legal and regulatory crisis that erupted in late March. The latest blow came when co-founder Yih-Shyan "Wally" Liaw, along with a company employee and a contractor, was charged with illegally smuggling American AI hardware to China.

According to the U.S. Department of Justice, the trio allegedly orchestrated a scheme to bypass U.S. export laws, funneling at least $2.5 billion worth of servers equipped with restricted, cutting-edge AI chips from Nvidia (NVDA) to Chinese customers through intermediaries, effectively dodging national security sanctions. Unsurprisingly, investor confidence has taken a significant hit as a result.

What was once a momentum-driven favorite is now flashing red flags across Wall Street. In fact, Bank of America recently flagged SMCI as one of the most heavily shorted stocks among hedge funds, with short interest climbing to roughly 14.2% of float, clear evidence that bearish bets are stacking up fast. So, with SMCI in deep trouble and hedge funds increasingly betting against the company, should you still buy the stock now?

About Super Micro Stock

With its roots in San Jose, California, Super Micro operates as a global provider of application-optimized IT infrastructure solutions. The company focuses on delivering systems tailored for enterprise, cloud computing, artificial intelligence, and emerging areas like 5G and edge computing. Its offerings span a wide range of products, including servers, storage systems, AI platforms, IoT solutions, networking equipment, software, and related support services.

A key aspect of Super Micro’s model is its in-house design and manufacturing capabilities, with operations spread across the U.S., Taiwan, and the Netherlands. This vertically integrated approach allows the company to maintain control over core components such as motherboards, power systems, and chassis, while also benefiting from global scale and operational efficiency.

Also, the company is known for its modular “Server Building Block Solutions” approach, which enables customers to configure systems based on specific workload requirements. By offering flexibility across processors, memory, GPUs, storage, networking, and cooling technologies, including air and liquid cooling, Super Micro aims to address a wide variety of use cases. The company’s market capitalization currently stands at about $14 billion.

However, despite its strong positioning in the server market, Super Micro shares have been on a brutal downward slide. The stock has plunged as much as 63% from its 52-week peak of $62.36 reached last July, a sharp fall from grace for a former AI high-flyer. Over the past year alone, the stock is down 24.4%, and the pain has continued into 2026, with shares sinking another 23%. In stark contrast, the broader S&P 500 Index ($SPX) has delivered a 30% gain over the past year and is down just 3.6% in 2026.

Inside Super Micro’s Q2 Earnings Report

Super Micro dropped its fiscal 2026 second-quarter earnings report on Feb.3, which revealed an interesting picture of record-shattering revenue growth paired with sharply tightening margins. For the second quarter, the server maker reported net sales of about $12.7 billion, marking a staggering 123% year-over-year (YOY) growth. This massive surge was fueled by the relentless demand for AI-optimized server racks and data center infrastructure, which now accounts for over 90% of the company's total business.

The revenue also blew past Wall Street’s forecasted figure of $10.44 billion. While the top line growth was quite impressive, investors focused heavily on the company's profitability metrics, which showed signs of significant strain. Gross margins fell sharply to 6.4%, down from 9.5% in the previous quarter and significantly below the 11.8% reported a year ago, highlighting aggressive pricing strategies as SMCI battles for market share against rivals like Dell (DELL) and Hewlett Packard Enterprise (HPE).

Even so, earnings managed to beat expectations. The company reported non-GAAP EPS of $0.69, up 17% YOY and ahead of the Street’s forecast of $0.49 per share. Yet, cash flow painted a more cautious picture. Operating cash flow turned negative at $24 million, a notable decline from the $894 million generated in the previous quarter and $216 million in the same quarter last year.

As of Dec. 31, 2025, SMCI held $4.1 billion in cash and cash equivalents, compared to $4.9 billion in total bank debt and convertible notes. Looking ahead, Super Micro expects net sales of at least $12.3 billion for the third quarter of fiscal 2026. It also forecasts GAAP net income per share of at least $0.52 and non-GAAP EPS of at least $0.60. For the full year, revenue is projected to reach at least $40 billion.

How Are Analysts Viewing Super Micro Stock?

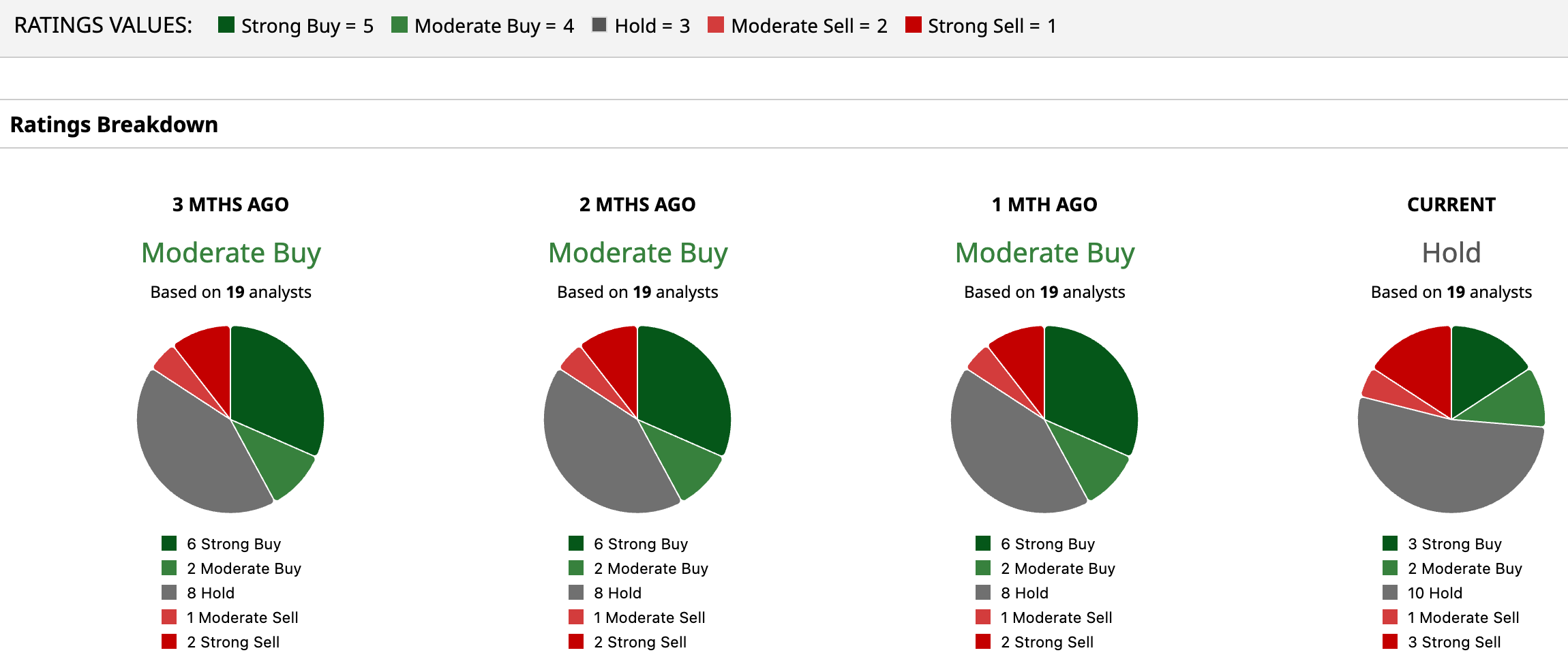

With regulatory uncertainty continuing to cast a shadow over its outlook, Super Micro is drawing a cautious stance from Wall Street. The stock currently carries a consensus “Hold” rating, reflecting a market that’s far from convinced. Of the 19 analysts covering the name, just three are firmly bullish with “Strong Buy” ratings, while two lean positive with “Moderate Buy.” However, the majority remain on the fence, with 10 analysts rating it a “Hold,” and sentiment on the bearish side including one “Moderate Sell” and three “Strong Sell” calls.

The average price target of $34.67 suggests a potential upside of 53.8%, pointing to room for recovery if sentiment improves. Moreover, at the high end, the Street-high target of $60 implies a massive 166.2% upside.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)