/Synchrony%20Financial%20site%20on%20phone-by%20madamF%20via%20Shutterstock.jpg)

With a market cap of $23.8 billion, Synchrony Financial (SYF) offers a wide range of credit products, including credit cards, installment loans, and commercial financing solutions. It also provides banking and deposit products, serving customers across industries such as retail, healthcare, and digital services through partnerships with major brands and merchants.

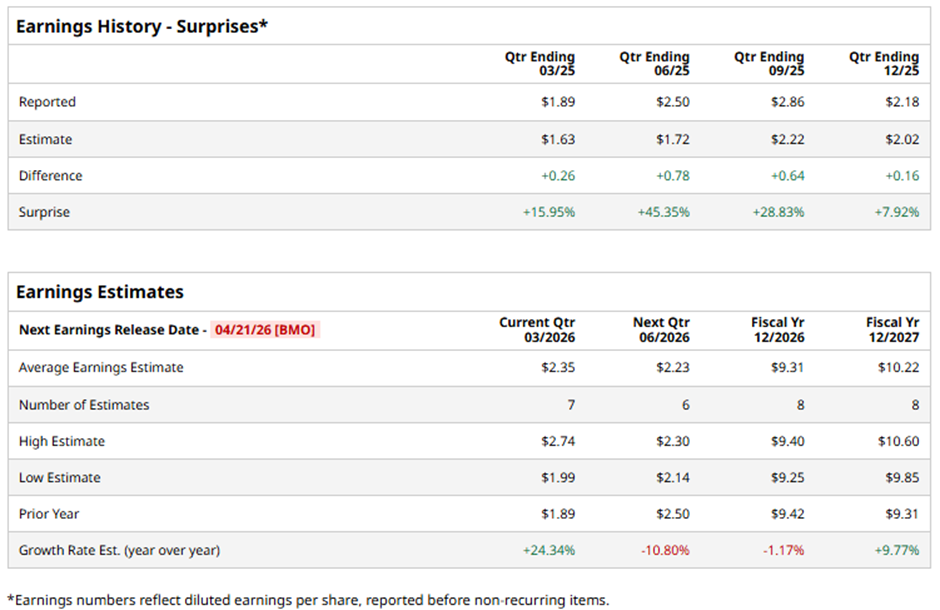

The Stamford, Connecticut-based company is set to announce its fiscal Q1 2026 results before the market opens on Tuesday, Apr. 21. Ahead of the event, analysts forecast SYF to report a profit of $2.35 per share, up 24.3% from $1.89 per share in the year-ago quarter. It has surpassed Wall Street's bottom-line estimates in the past four quarters.

For fiscal 2026, analysts expect the credit card issuer to report EPS of $9.31, down 1.2% from $9.42 in fiscal 2025. However, EPS is anticipated to grow 9.8% year-over-year to $10.22 in fiscal 2027.

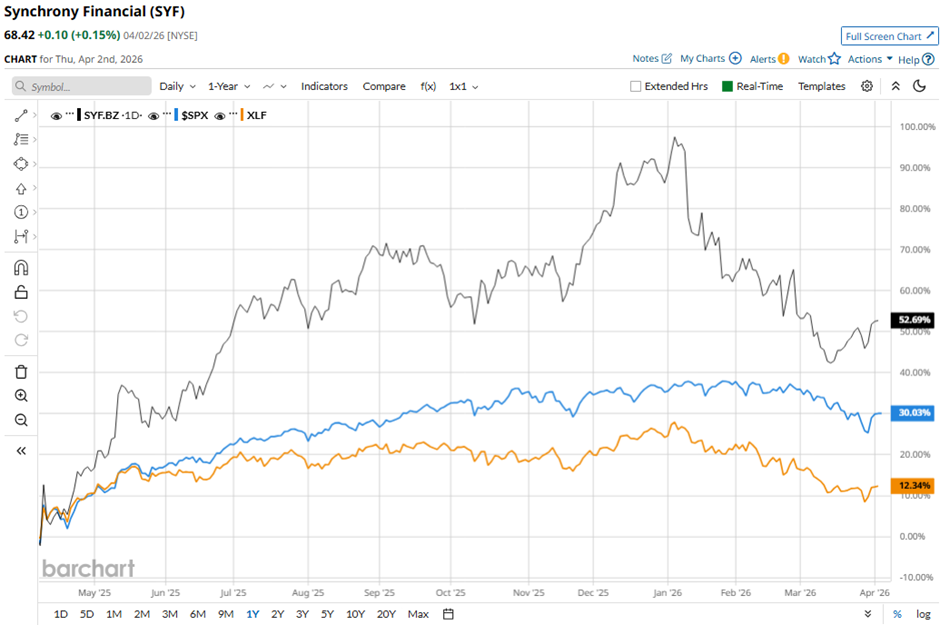

Shares of Synchrony Financial have surged 24.3% over the past 52 weeks, outperforming both the S&P 500 Index's ($SPX) nearly 22% gain and the State Street Financial Select Sector SPDR ETF's (XLF) 1.3% decline over the same period.

Shares of Synchrony Financial fell 5.8% on Jan. 27 after it reported Q4 2025 results that slightly missed expectations, with EPS of $2.04 and revenue of $3.79 billion. Investor sentiment was further hurt by weak 2026 guidance, with expected EPS of $9.10 - $9.50 (midpoint $9.30) below the analyst estimate.

Additionally, concerns grew after the management warned that a proposed 10% U.S. credit-card interest rate cap could significantly reduce lending, especially to lower-income consumers, alongside rising costs (up 10% to $1.40 billion) and a $67 million restructuring charge added pressure.

Analysts' consensus rating on Synchrony Financial stock is cautiously optimistic overall, with a "Moderate Buy" rating. Out of 24 analysts covering the stock, 14 recommend a "Strong Buy," one has a "Moderate Buy" rating, and nine give a "Hold" rating. The average analyst price target for SYF is $87.08, indicating a potential upside of 27.3% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)