/A%20Tesla%20Cybertruck%20with%20visible%20bullet%20impacts_%20Image%20by%20Karolis%20Kavolelis%20via%20Shutterstock_.jpg)

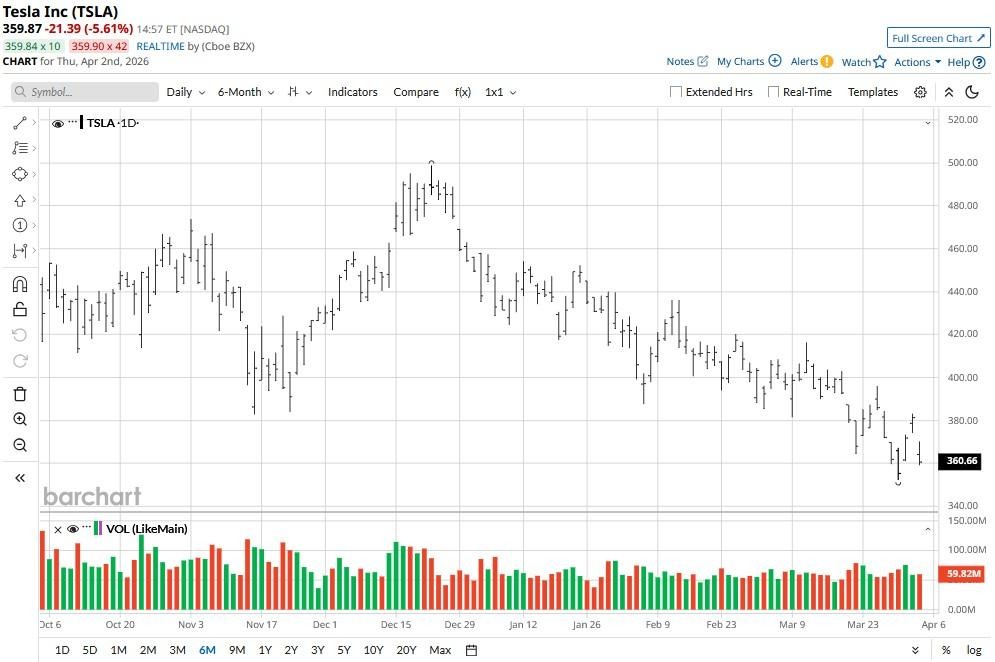

Tesla (TSLA) shares inched down on April 2 after the electric vehicle (EV) behemoth posted Q1 deliveries that came in significantly below Wall Street estimates.

In its press release, Elon Musk’s company said it delivered 358,023 vehicles in the first quarter — down more than 14% sequentially and missing consensus estimates of about 365,645 units.

Versus its year-to-date high, Tesla stock is now down roughly 20%.

Why Q1 Deliveries Are Particularly Bearish for TSLA Stock

Investors bailed on TSLA shares this morning mostly because the Q1 deliveries report signals the “EV slowdown” may be a company-specific problem — not a macro trend.

While Tesla grappled with a production-delivery gap of more than 50,000 units, its Chinese competitors actually saw a significant sales rebound in March.

BYD (BYDDY) surged with nearly 296,000 passenger vehicles sold, while Li Auto (LI) and Nio (NIO) posted strong double-digit gains (month-on-month) each. Even newcomer Xiaomi (XIACY) exceeded 20,000 monthly units.

This divergence indicates that Tesla is losing its grip on the world’s largest EV market (China), as local brands offer more frequent refreshes and aggressive pricing.

Dan Ives Remains Bullish As Ever on Tesla Shares

Despite delivery weakness, Wedbush’s senior analyst Dan Ives continues to recommend sticking with Tesla shares in 2026.

According to Ives, investors should focus more on the firm’s artificial intelligence (AI) initiatives, as they’re now more important for its future cash generation and stock price performance.

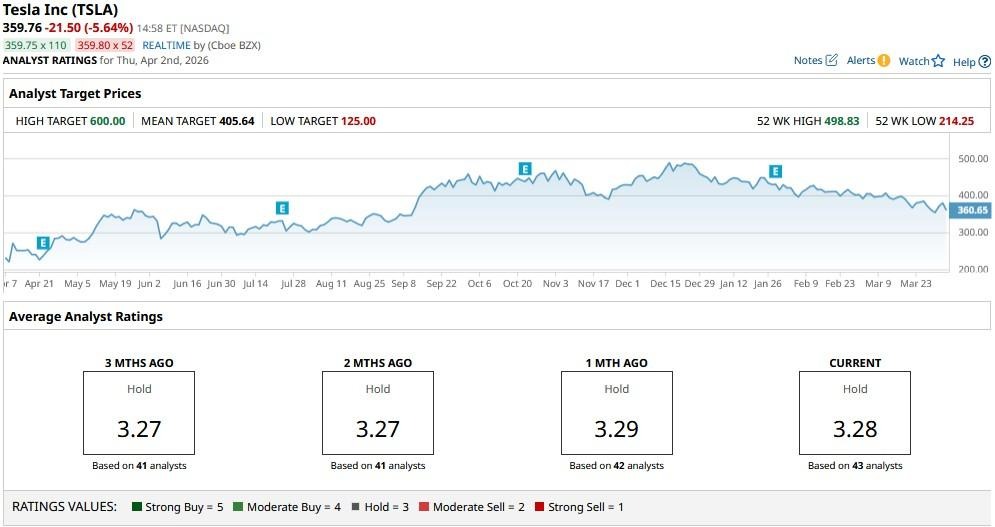

Ives maintained an “Outperform” rating on TSLA with a $600 price objective, indicating potential upside of more than 60% from current levels.

At less than 15x sales, the EV stock is currently trading at a much lower valuation multiple than its historical average, which makes it even more attractive for those seeking a bargain.

What’s the Consensus Rating on Tesla?

Other Wall Street analysts aren’t nearly as bullish as Ives — but they do believe that the recent selloff in TSLA stock has indeed gone a bit too far.

According to Barchart, while the consensus rating on Tesla is a “Hold,” the mean price target of about $405 signals potential upside of nearly 13% over the next 12 months.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.