U.S. stocks have had a rough start this spring, and the selloff has pushed several familiar names into oversold territory. The S&P 500 Index ($SPX) is nearing oversold levels across the board as volatility continues to rise, putting several familiar names under added strain. Among the most notable names are Sysco (SYY) and Estée Lauder (EL), two S&P 500 companies that fell hard on company-specific headlines and now trade near recent lows.

Both stocks look beaten down for different reasons. Sysco was hit after the company unveiled a debt-heavy acquisition, while Estée Lauder slid on takeover speculation that raised concerns about valuation and leverage.

These sharp selloffs have left investors asking the same question. Has the market gone too far, or is there still more downside ahead?

Oversold Stock #1: Sysco (SYY)

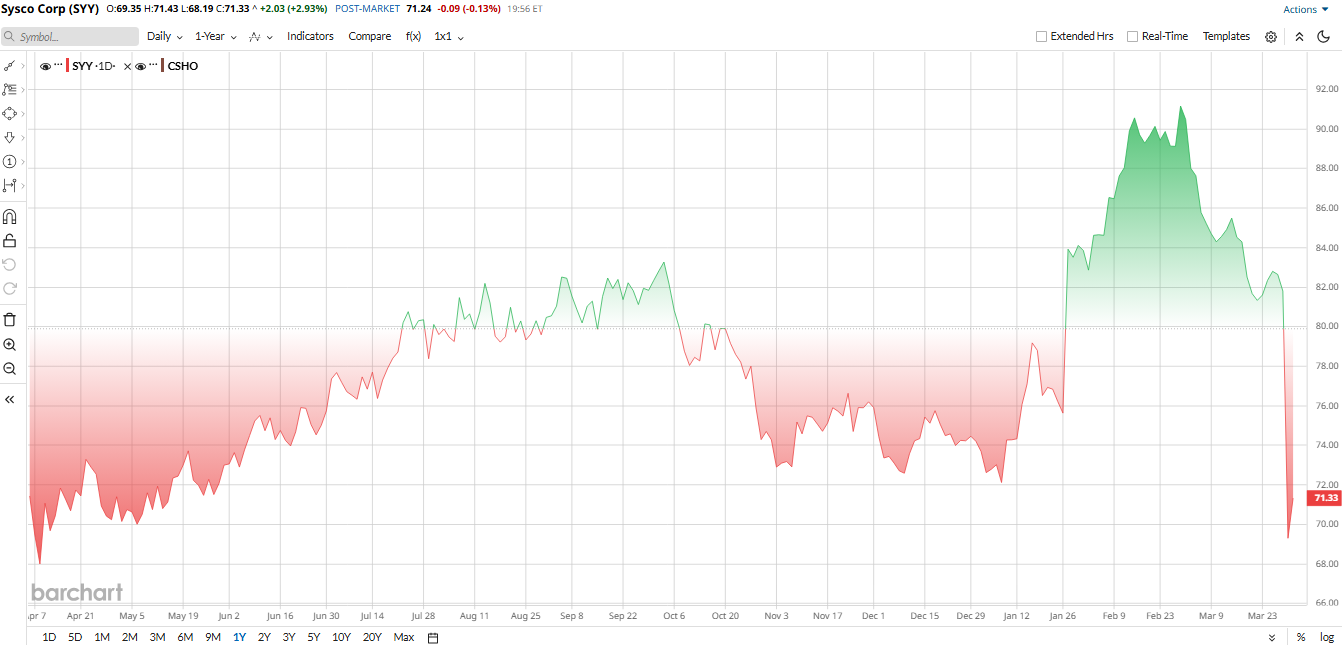

Sysco has taken the harder hit in recent days. SYY stock, which traded near $80 in early March, fell about 15% on March 30 to roughly $69, giving up previous gains and bringing the stock roughly flat year-to-date (YTD).

The decline came after the company said it would buy Jetro Restaurant Depot in a $29.1 billion deal. The acquisition is being funded mostly with new debt, which was enough to rattle the market. Even after the drop, Sysco remains a dominant foodservice distributor with $21 billion in quarterly sales and a long record of steady cash generation.

At recent prices, Sysco does not look especially expensive. SYY stock trades at about 15.6 times trailing earnings, which is in line with other mature food distributors. Its forward dividend yield is about 3%, giving income investors another reason to watch the name.

The company’s latest reported quarter showed revenue of $20.8 billion, up 3% from a year earlier, while adjusted EPS rose 6.5% to $0.99. For fiscal 2025, sales climbed 3.2% to $81.4 billion, and adjusted EPS increased 3.5% to $4.46. Management expects fiscal 2026 sales growth of about 3% to 5%, with low-single-digit EPS growth.

The Jetro deal could also improve the story over time. CEO Kevin Hourican has described the asset as a strong fit, and management says the acquisition could lift margins and cash flow if integration goes well. Sysco expects the deal to add to earnings and generate roughly $2 billion of extra free cash flow by year four.

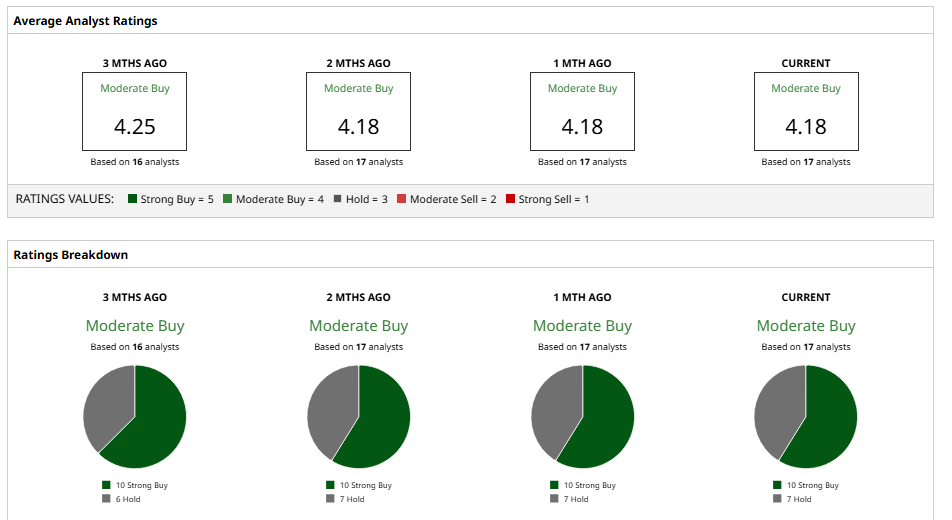

Wall Street remains cautious but constructive. Analysts have a consensus "Moderate Buy" rating on SYY stock. The average price target of $90.78 implies potential upside of about 27% from current levels.

Oversold Stock #2: Estée Lauder (EL)

Estée Lauder makes prestige beauty products, including skincare, makeup, fragrance and hair care, selling through department stores, travel retail and digital channels across global luxury markets for consumers worldwide.

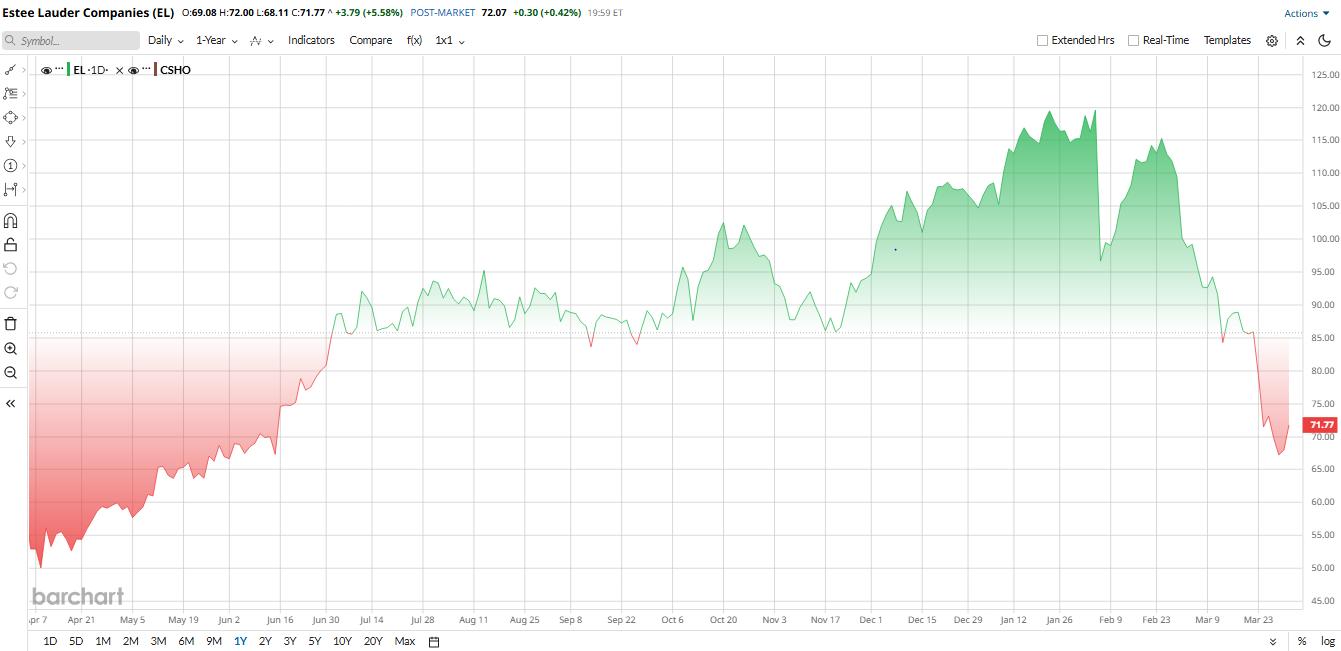

Unfortunately, the company has also been caught in the recent wave of selling. EL stock traded in the $90 range earlier this year before sliding nearly 10% on March 24 on reports that Estée Lauder may be considering the purchase of Spanish beauty group Puig (PUIGF). That sparked investor concerns about price and debt, and the shares kept falling. The stock now trades near $67, down roughly 35% YTD and far below its late-January peak.

The pullback came even though the underlying business remains intact. In its latest quarter, the company reported revenue of $4.23 billion, up about 6% from a year earlier and roughly in line with expectations. Growth was helped by travel retail and a rebound in Asia, while management described the quarter as a strong one.

Unlike Sysco, Estée Lauder still carries a premium valuation. The stock trades at about 36.8 times trailing earnings, above the cosmetics sector average of around 19 times. That is less demanding than before, but it still leaves little room for disappointment.

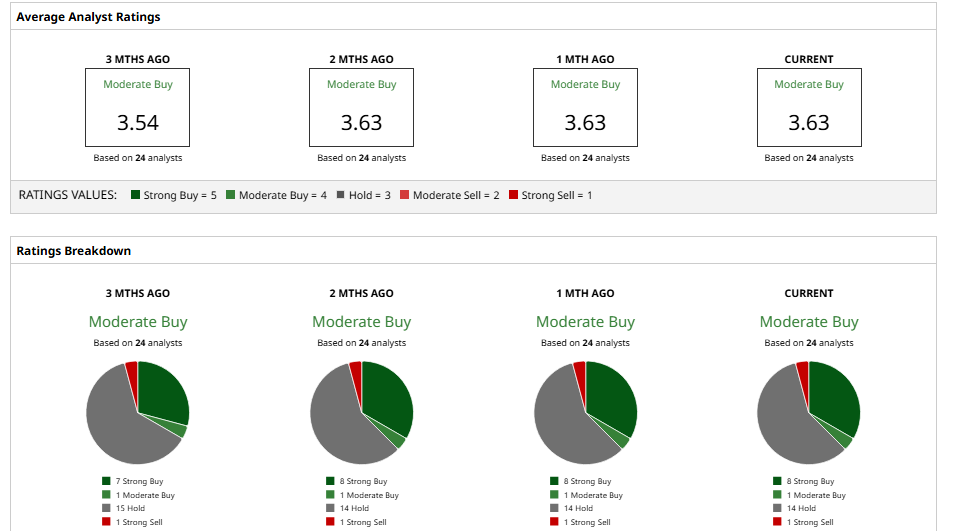

Analysts see room for a rebound, however. The consensus rating is a “Moderate Buy," with the average target of $104.52 suggesting more than 55% potential upside from the current price. Citi recently upgraded EL stock to a “Buy” with a $120 target, while JPMorgan kept an “Overweight” rating and a $121 target.

Other firms are more restrained, but even the lower-end targets sit well above the current share price. That suggests the recent weakness is being driven more by sentiment than a breakdown in the business.

The Bottom Line

Sysco and Estée Lauder are both trading at oversold levels. On one hand, Sysco’s drop reflects fear around a large debt-funded deal, while Estée Lauder’s decline is tied more to takeover rumors and market nerves about luxury spending.

For investors looking for quality names at discounted prices, both of these stocks may deserve a chance. Sysco offers a steadier income story with valuation support, while Estée Lauder offers more upside if growth in beauty demand keeps holding up.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)