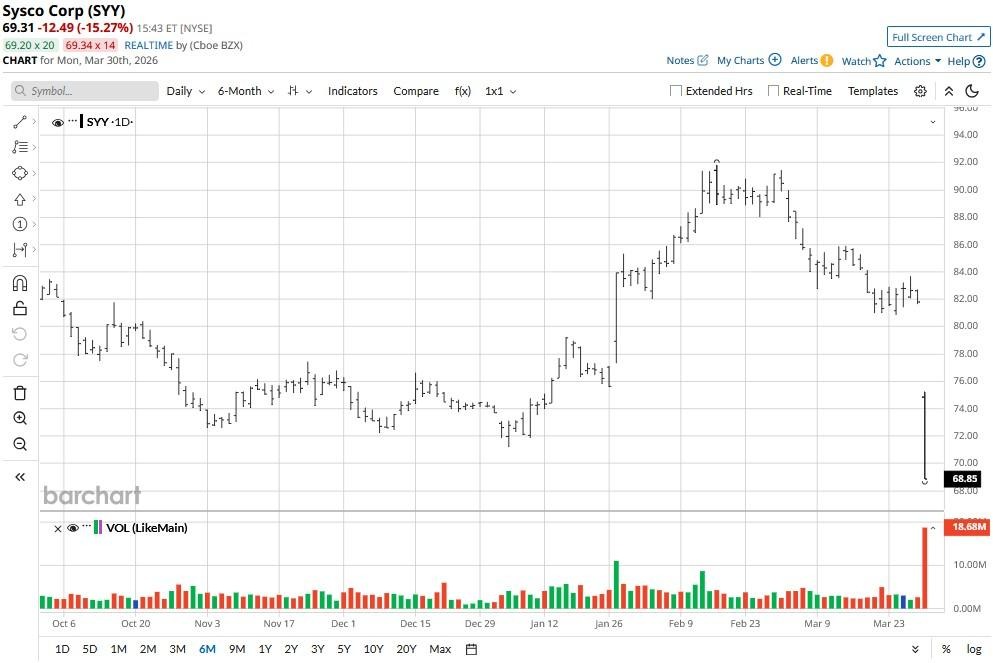

Sysco (SYY) shares were hit hard on March 30 after the food distribution company said it’s spending $29 billion on buying Jetro, a “cash and carry” heavyweight that owns Restaurant Depot. In a post-announcement interview with CNBC, CEO Kevin Hourican dubbed Jetro a “gem of an asset,” but integration risks and the sheer size of this deal still made investors bail on SYY today.

At the time of writing, Sysco stock is trading at a more than 20% discount to its year-to-date high.

Is Jetro Deal Bullish for Sysco Stock?

Sysco expects the aforementioned transaction to boost its earnings per share (EPS) by mid-to-high single digits in the first year — and generate up to $2 billion in excess free cash flow by year four.

That’s capital “we can return to investors, increase dividends, increase buybacks, or reinvest in the business for growth,” Hourican said this morning on Squawk Box.

In short, the Jetro acquisition is bullish for SYY shares, as it’s expected to boost the firm’s operating margin to 6%.

Long-term investors should load up on Sysco also because its relative strength index (14-day) has crashed into the mid-teens, indicating extremely oversold conditions that may trigger a relief rally in the near-term.

Why Else Should You Buy SYY Shares Today?

Jetro deal is largely positive for SYY also because it gives it a strong foothold in “cash and carry,” which CEO Hourican described as a “compounding growth business” in the CNBC interview.

Historically, the cash and carry format tends to be resilient during economic volatility as it’s where you go “to save money,” the chief executive added.

Simply put, now that the NYSE-listed firm has both a premium delivery service as well as a value-focused cash and carry segment, it’s strongly positioned to weather macro shifts and benefit from the sprawling small restaurant landscape.

Over time, this may help Sysco shares stage an exciting comeback.

How Wall Street Recommends Playing Sysco

Investors should also note that Wall Street hasn’t thrown in the towel on SYY stock yet.

The consensus rating on Sysco Corp remains at “Moderate Buy”, with the mean target of about $92 indicating potential upside of nearly 35% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)