/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

For more than 35 years, British chip designer Arm Holdings plc (ARM) has built its business on a simple but powerful model, licensing its instruction sets to some of the world’s biggest chipmakers, including Nvidia (NVDA) and Qualcomm (QCOM), and collecting royalties on every processor built using its designs. That approach has kept Arm at the center of the semiconductor industry without ever producing chips itself. Now, that is starting to change.

On March 24, Arm investors received a major update when CEO Rene Haas unveiled the company’s first in-house chip at an event in San Francisco. The move begins with the launch of the Arm AGI CPU, an Arm-designed processor built specifically for artificial intelligence (AI) data centers. It is aimed at a new wave of agentic AI workloads and is designed to deliver more than 2x performance per rack compared with traditional x86 platforms.

The shift has been long anticipated and marks a significant turning point for Arm, often referred to as the “Switzerland” of chip companies, as it now steps into more direct competition with some of its own customers. What makes this development even more notable is that Arm is not entering this space alone. The company has already secured a strong lineup of early adopters. Meta Platforms (META) is serving as the lead partner and co-developer of the Arm AGI CPU and is expected to be its first large-scale user.

Other early customers include Cloudflare (NET), F5 (FFIV), ChatGPT maker OpenAI, enterprise software company SAP (SAP), and SK Telecom (SKM), South Korea’s largest telecommunications operator, among others. With Arm now taking a more direct role in building AI-focused silicon, and doing so alongside some of the biggest names in tech, should investors be loading up on ARM shares after this shift?

About Arm Stock

Founded in 1990, England-based ARM is a world-leading technology company that acts as the architect for the digital world. Its designs sit at the core of modern electronics, powering everything from smartwatches and smartphones to high-performance computing systems. While it is a leading semiconductor player, Arm’s approach is different from most semiconductor companies. It doesn’t manufacture chips.

In fact, rather than manufacturing chips itself, Arm focuses on designing the underlying architecture, essentially the “blueprints” that determine how processors operate. This approach shapes its business model. The company generates revenue by charging licensing fees to customers such as smartphone manufacturers, cloud providers, and chip designers that use its technology. It also earns ongoing royalties each time a chip built on Arm’s architecture is shipped.

Although smartphones have traditionally been its largest revenue source, Arm’s presence has been expanding into other areas. Its designs are increasingly being used in data centers, automotive applications, consumer devices, and AI-related chips, reflecting a broader shift in the direction of computing demand growth. For a long time, this model allowed Arm to remain central to the semiconductor ecosystem without taking on the capital-intensive burden of running fabrication facilities.

However, the company is now adjusting its approach. With the introduction of its first in-house processor, the Arm AGI CPU, aimed at handling advanced AI workloads in data centers, Arm is beginning to move beyond pure design into a more direct role in the computing stack. Currently valued at a market capitalization of about $142.6 billion, shares of this chip designer are up an impressive 47.94% so far in 2026, while the broader S&P 500 Index ($SPX) has suffered a 3.5% decline year-to-date (YTD).

Arm’s valuation appears richly priced. The stock trades at an eye-watering 145.63 times earnings and 29.25 times sales, far above typical industry levels. By comparison, the sector’s median sits at just 28.74 times earnings and 2.96 times sales. This suggests investors are already baking in strong future growth, especially tied to AI and data centers.

Inside Arm’s Q3 Earnings Results

Arm’s third-quarter fiscal 2026 results, reported on Feb. 4, highlighted the company’s growing momentum in AI and data center markets. The company delivered record revenue of $1.24 billion, up 26% year-over-year (YOY), marking its fourth straight quarter above the $1 billion mark. The top line also edged past Wall Street expectations of $1.23 billion. A key driver behind this performance was record royalty revenue, which rose 27% annually to $737 million.

This growth was driven by the increasing adoption of higher-value technologies like Armv9 architecture and Arm Compute Subsystems (CSS), along with a growing presence of Arm-based chips in data centers. In fact, the company highlighted strong traction for its CSS, which it introduced nearly two and a half years ago. Demand has exceeded expectations, with Arm signing two additional CSS licenses during the quarter for edge AI tablets and smartphones, bringing the total to 21 licenses across 12 companies.

Five customers are now shipping CSS-based chips, including two that have already moved to second-generation platforms, while the top four Android smartphone vendors are all shipping devices powered by CSS. On the licensing side, revenue rose 25% YOY to $505 million, supported by the timing and scale of several high-value deals, as well as contributions from backlog.

Momentum was equally visible in forward-looking metrics. Annualized contract value (ACV), which reflects normalized license and related revenue, climbed 28% YOY to $1.62 billion. Profitability remained solid, with non-GAAP EPS coming in at $0.43, comfortably ahead of the $0.41 estimate and up from $0.39 a year ago. Also, ARM maintained a strong balance sheet, ending the quarter with $3.54 billion in cash, cash equivalents, and short-term investments.

Looking ahead, Arm expects the momentum to continue. For fiscal Q4 2026, management is guiding for revenue of around $1.47 billion, with a possible variation of $50 million. Adjusted EPS is projected to land between $0.54 and $0.62, signaling continued strength as the company leans further into AI-driven growth.

How Are Analysts Viewing Arm Stock?

Wall Street is increasingly warming up to Arm’s evolving story. Raymond James recently upgraded the stock from “Market Perform” to “Outperform,” assigning a $166 price target. The upgrade reflects growing confidence in Arm’s shift toward a fabless semiconductor model. Analyst Simon Leopold highlighted that the move into producing its own chips, a strategy he has long supported, could drive stronger operating profits, accelerate growth, and add a meaningful new lever to the company’s strategy.

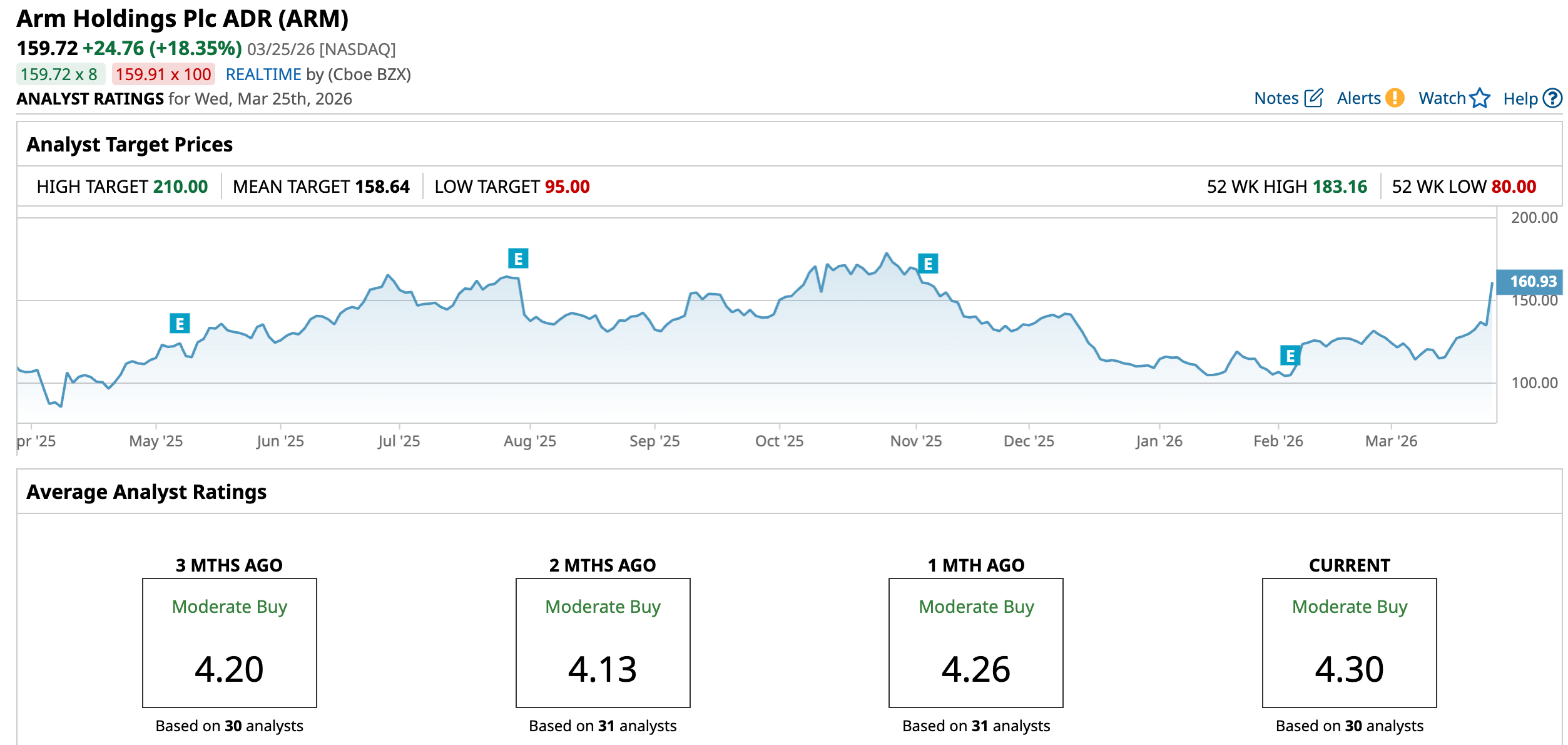

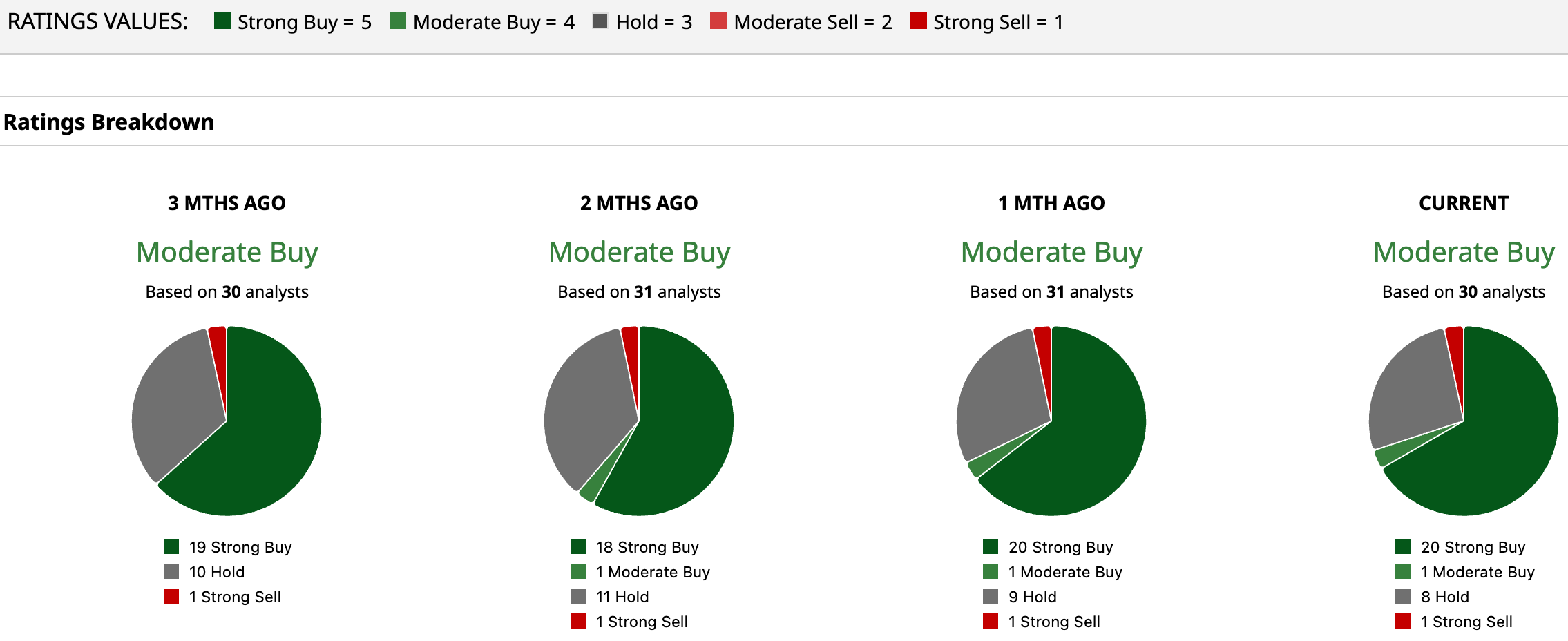

The broader analyst community also leans positive. Arm currently holds a consensus “Moderate Buy” rating, with sentiment skewed heavily toward the bullish side. Out of 30 analysts, 20 rate the stock a “Strong Buy,” one has a “Moderate Buy,” eight remain on “Hold,” and only one has issued a “Strong Sell.” The average price target of $158.64 has already been surpassed, while the most optimistic target of $210 implies the stock could climb as much as 31.5% from here, underscoring the high expectations surrounding Arm’s next phase of growth.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)