/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Semiconductor company Micron Technology (MU) recently raised its quarterly dividend from $0.115 per share to $0.15, indicating an increase of 30%. The new dividend accumulates to an annual rate of $0.60 and yields 0.14% on current prices. This dividend hike comes as Micron faces a surge in demand for DRAM and NAND memory chips.

However, investors have also focused on Micron’s potentially rising capex as the company seeks to expand its infrastructure to support rising demand for memory chips. And, the company landed its first five-year Strategic Customer Agreement (SCA), which reportedly includes detailed multi-year commitments that promote operational stability.

Against this backdrop, should you consider buying Micron Technology’s stock?

About Micron Technology Stock

Micron Technology is a leading semiconductor company specializing in the design, manufacturing, and sale of innovative memory and storage solutions like DRAM and NAND flash. Headquartered in Boise, Idaho, it serves as the central hub for global operations, directing a network of fabrication plants, research centers, and sales offices worldwide.

The company focuses on enabling data-intensive applications across data centers, PCs, mobile devices, and the automotive sector through advanced technology that transforms how the world uses information. It has a market capitalization of $455.99 billion.

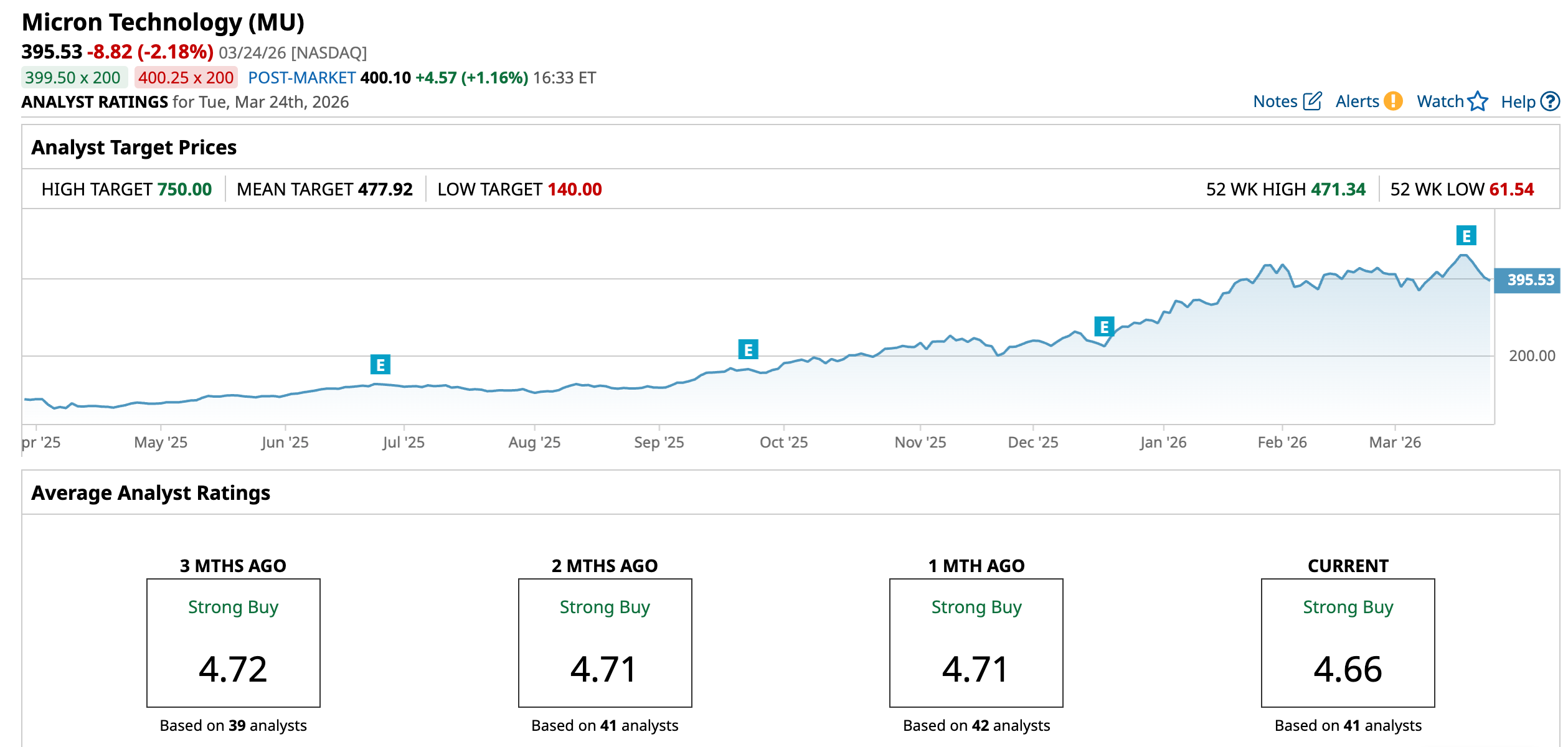

A huge AI-driven surge is driving demand for Micron’s DRAM and high-bandwidth memory (HBM) chips, outpacing supply and pushing prices significantly higher. This has led to the company’s stock gaining 308% over the past 52 weeks and 38.6% year-to-date (YTD). Just for comparison, the S&P 500 index ($SPX) is up 13.68% over the past 52 weeks and is down 4.2% YTD. Micron’s stock reached an all-time high of $471.34 on March 18, but is down 19% from that level.

Despite the huge surge, Micron’s stock is trading at relatively cheaper levels. On a forward-adjusted basis, its price-to-earnings ratio of 6.98 times is lower than the industry average of 21.53 times.

Micron Technology’s Q2 Delivers Strong Results on AI Memory Demand Surge

For the second quarter of fiscal 2026 (quarter ended Feb. 26), Micron’s revenue increased by a whopping 196.3% year-over-year (YOY) to $23.86 billion, which was higher than the $19.61 billion that Wall Street analysts had expected. Non-GAAP gross margin as a percent of revenue increased from 37.9% to 74.9%.

The company’s cloud memory business unit revenue increased by 162.9% annually to $7.75 billion, while its core data center business unit’s revenue grew by 210.8% to $5.69 billion. The company’s non-GAAP EPS (on a diluted basis) grew YOY from $1.56 to $12.20, higher than the $8.80 that Street analysts had expected. Despite these robust results, the stock dropped as investors were concerned about the company’s expenditures to scale the next AI cycle.

Wall Street analysts expect Micron’s profitability to continue to grow. For the current quarter, its EPS is expected to grow significantly YOY to $18.90. For fiscal 2026, analysts expect the company’s EPS to grow considerably to $40.01, followed by a 53.1% expansion to $61.25 in fiscal 2027.

What Do Analysts Think About Micron Technology Stock?

Following Micron’s latest quarterly results, Wall Street analysts have issued multiple positive reaffirmations of its prospects. Analysts at Barclays maintained an “Overweight” rating on the stock, raising the price target from $450 to $675, citing solid results and a strong outlook supported by tight supply-and-demand conditions for DRAM and NAND through this year. Barclays analysts also highlighted Micron’s first five-year supply chain agreement, which provides increased visibility.

RBC Capital analysts maintained an “Outperform” rating and a $525 price target. The firm expects gen AI demand to remain strong and structural drivers to play a bigger role in the current upcycle than anticipated. RBC Capital analysts also expect healthy pricing through 2027 and sizable expansion potential. Citing Micron’s solid Q2 results, KeyBanc analysts kept a bullish “Overweight” rating on the stock and raised the price target from $450 to $600.

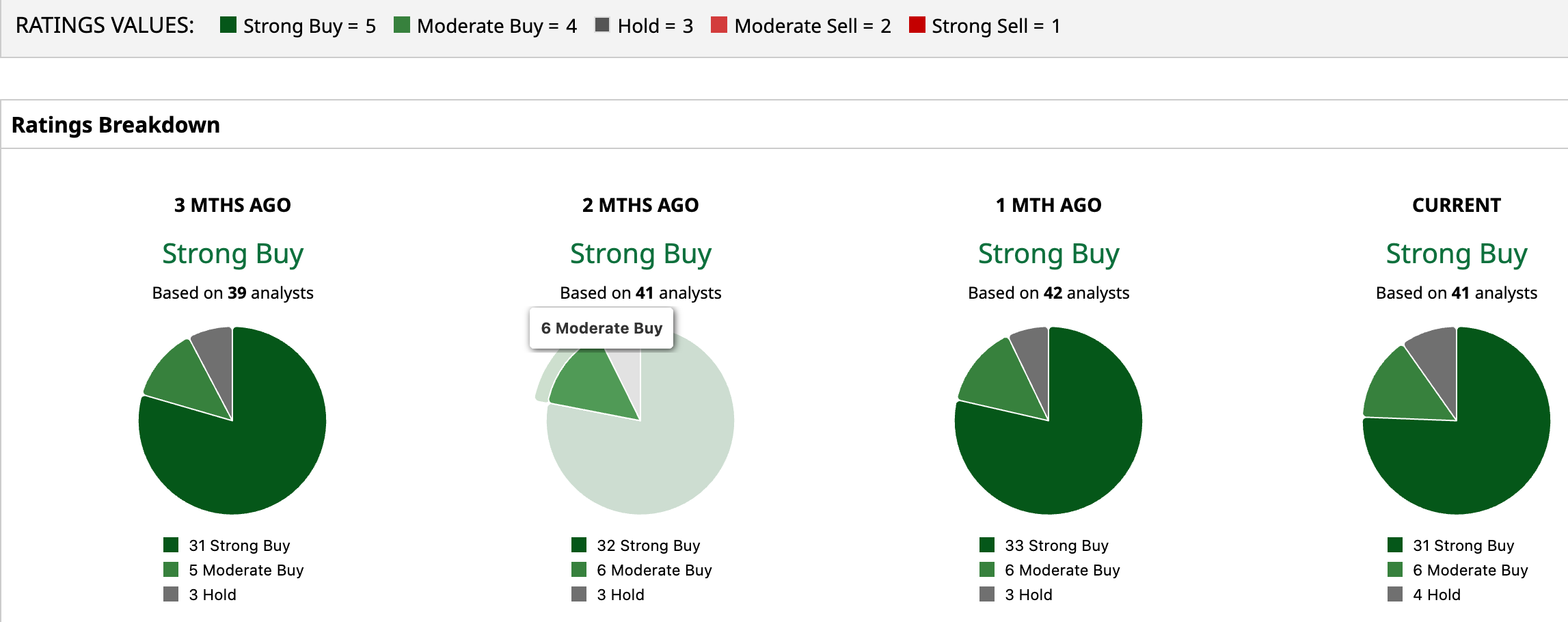

Micron Technology has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 41 analysts rating the stock, a majority of 31 analysts have given it a “Strong Buy” rating, six analysts rated it “Moderate Buy,” while four analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $477.92 represents an 20.8% upside from current levels. The Street-high price target of $750 indicates a 89.6% upside.

Key Takeaways

Despite the stock's dip after its earnings, Micron is sporting solid fundamentals. The whopping 30% hike in its dividend exhibits faith in its cash flow generation. As Wall Street analysts are bullish about its prospects, the stock might be a buy now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)