Energy stocks tied to liquefied natural gas have been drawing fresh attention as geopolitical risks disrupt the whole global supply. When major export facilities face damage or shutdown threats, LNG prices can move quickly, and the ripple effect often shows up in shares of producers and exporters.

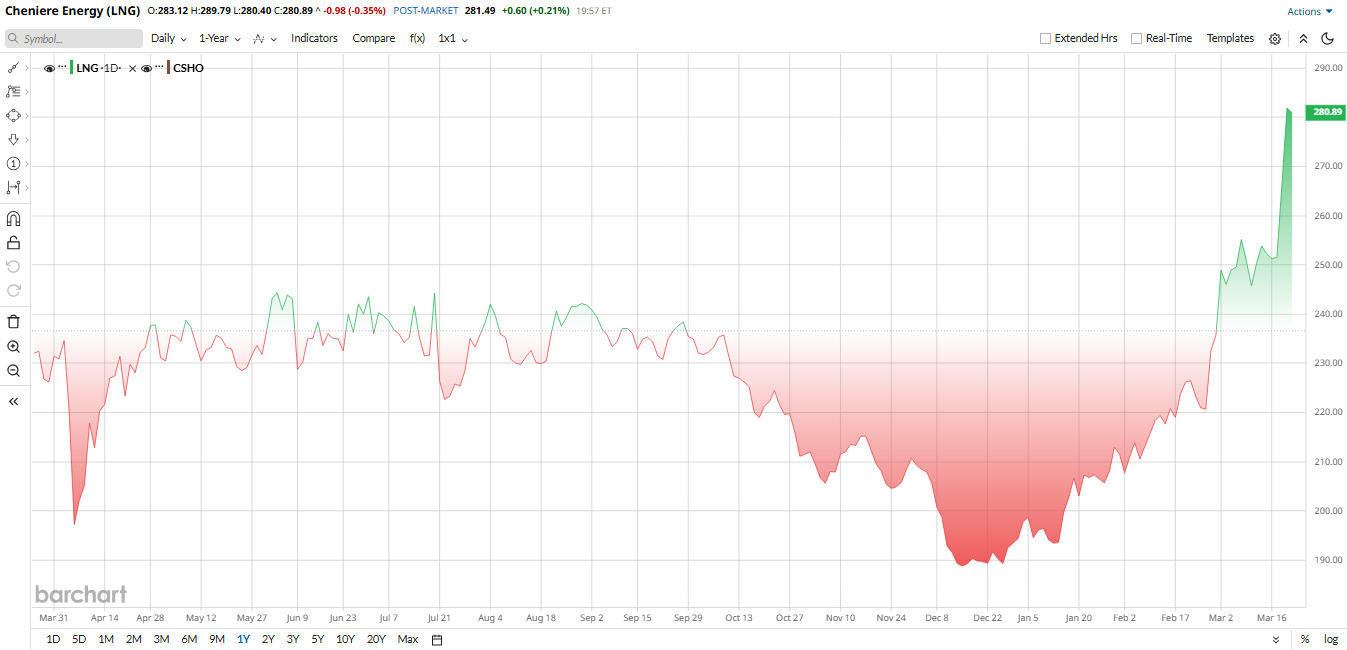

This has favorably impacted Cheniere Energy (LNG), as it is the largest LNG exporter in the U.S. Its shares have soared to historic levels since investors are responding to news that Iranian attacks have disrupted Qatar's LNG production capacity for up to five years. This reduction in supply has increased the expectations of the exporters, such as Cheniere. Now that the stock is already at an all-time high, the more important inquiry is whether the upswing will continue or if it is the investors buying a move that might as well be factored by the positive news.

About LNG Stock

Cheniere Energy is a Houston-based energy company that owns the Sabine Pass and Corpus Christi LNG export terminals. Its two main segments are LNG terminal operations and LNG/natural gas marketing. Essentially, Cheniere buys natural gas, liquefies it, and sells LNG to global customers. It operates six “trains” across two facilities and has long-term sales contracts with buyers around the world.

Cheniere is also lining up long-term growth. In December 2025, it began feeding LNG from its new Train 5, and in February 2026, it won two more FERC approvals for capacity expansions of the Sabine and Corpus Christi projects. It also signed a new 20-year contract with Taiwan’s CPC Corp. (1.2 MTPA).

Cheniere’s stock is having a banner run. After slumming in late 2025, LNG stock soared briefly, up roughly 47% in 2026. Most of those gains came amid the Iran-Israel conflict, as each time threats to Middle East supply flared, LNG exporters rallied. For example, after news of damage at QatarEnergy’s Ras Laffan LNG hub, Cheniere’s share price spiked to a new all-time high, briefly trading near $297. In short, bullish supply fears have lifted Cheniere far above its levels from a year ago.

Even after this rally, Cheniere doesn’t look outrageously expensive. Its forward valuation is actually quite modest for an energy stock. The company trades at roughly 12× current earnings, well below the 19× average P/E of the broader energy sector. Which means LNG’s stock looks cheaper than oil majors or even many utility-like energy firms.

Impact of the Iran Conflict

The jump in Cheniere’s stock is directly tied to the Iran war. When Iran attacked Qatar’s LNG plants between March 18 and 19, QatarEnergy admitted “extensive damage” to Ras Laffan. Bloomberg reported this cut about 12.8 million tons per year, about 17% of Qatar’s capacity for up to five years. That news roiled global gas markets; LNG spot prices roughly doubled in days as markets anticipated a supply crunch. U.S. exporters like Cheniere became a safe haven.

Traders assumed U.S. LNG buyers like Shell (SHEL) and Total (TTE)) would have to buy more from Sabine Pass and Corpus Christi. Cheniere’s shares jumped on each wave of news, often climbing 5% to 10% in a session. Of course, any resolution of the conflict or alternative supplies could moderate prices, so traders are also wary of volatility.

Strong Q4 Performance Driven by Higher LNG Volumes

Cheniere Energy’s latest quarter highlights why investors have been willing to push the stock higher. In Q4 2025, the company generated about $5.45 billion in revenue, up 23% from a year ago, driven largely by higher LNG volumes. Net income surged to roughly $2.30 billion, more than doubling year-over-year (YoY), helped by increased shipments and favorable pricing dynamics. Adjusted EBITDA rose about 30% to $2.05 billion.

Operationally, the company delivered 185 LNG cargoes during the quarter, compared to 167 a year earlier, reflecting strong demand and added capacity from its Corpus Christi expansion. For the full year, revenue reached around $20 billion, while net income climbed 64% to $5.33 billion. Distributable cash flow came in near $5.29 billion, underscoring solid cash generation.

Management expects continued momentum, projecting 2026 EBITDA between $6.75 billion and $7.25 billion. The company is also guiding for steady cash flow as additional capacity ramps up.

Cheniere has expanded its share buyback plan beyond $10 billion through 2030 and continues to generate strong free cash flow, even as it invests in growth and reduces debt.

Wall Street Opinion of LNG Stock

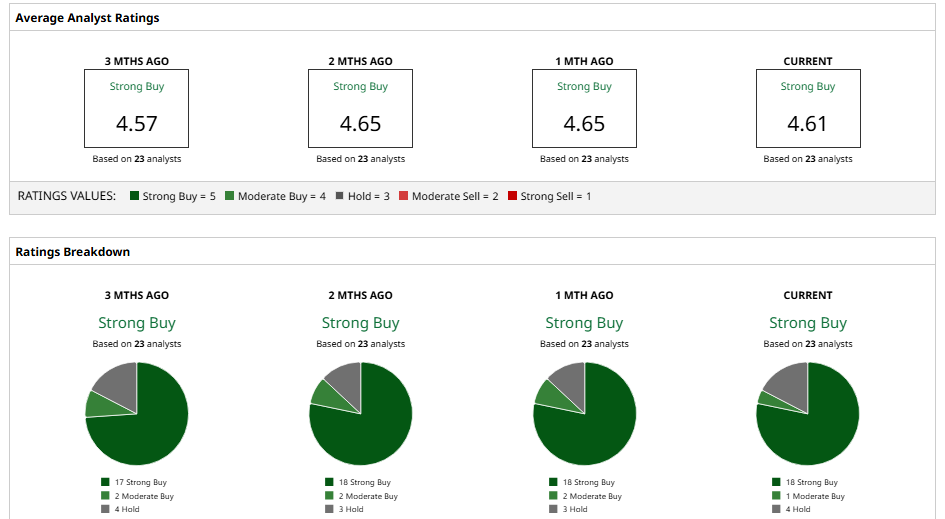

Wall Street analysts remain very bullish. Barchart’s consensus rating for LNG is a “Strong Buy.” The consensus price target is around $274, not far from the current $266, so the median analyst sees limited near-term upside.

Opinions vary; for example, Morgan Stanley recently reiterated an “Equal-Weight” rating with a $236 target, implying a slight downside, noting that much of the near-term opportunity is priced in.

In contrast, UBS analyst Manav Gupta set a $301 target, which suggests at least 19% upside, arguing Cheniere’s contracts and limited global LNG supply point to higher prices. Goldman Sachs is similarly upbeat; it had a $275 target, emphasizing that even before the Iran war, the global LNG market was tight.

The Bottom Line

Cheniere’s shares have surged on real, fundamental bullishness in global LNG markets. Its latest earnings and contracts back up the growth case. LNG stock is no longer a deep value; it’s near the top of its trading range, but it still trades cheaply versus broad energy peers. If you believe the Iran/Qatar disruption is structural or that other supplies won’t quickly come online, the rally might continue. If you worry prices will fall back, the current level may not look as attractive.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)