/Baxter%20International%20Inc_%20logo%20on%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

Baxter International Inc. (BAX), headquartered in Deerfield, Illinois, develops and provides a portfolio of healthcare products. With a market cap of $8.8 billion, the company develops, manufactures, and markets products and technologies related to hemophilia, immune disorders, infectious diseases, kidney disease, trauma and other chronic and acute medical conditions. The company's products are used by hospitals, kidney dialysis centers, nursing homes, rehabilitation centers, doctors' offices, and research laboratories.

Companies worth $2 billion or more are generally described as “mid-cap stocks,” and BAX perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the medical instruments & supplies industry. Baxter excels through diversified healthcare products and innovative expansions. Strategic acquisitions enhance its connected care solutions, while investments in new launches and geographic growth solidify its medical technology leadership.

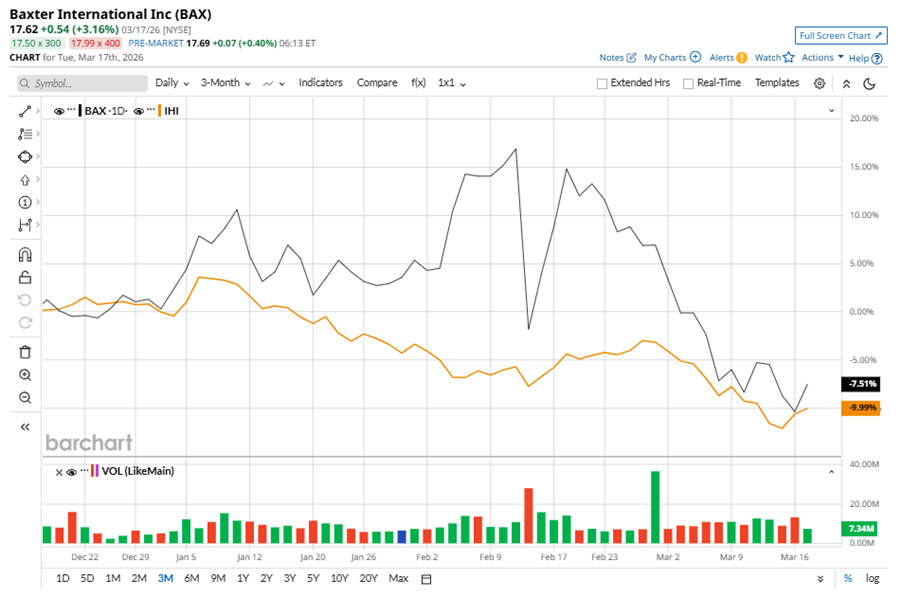

Despite its notable strength, BAX shares have slipped 49.5% from their 52-week high of $34.92, achieved on Mar. 18, 2025. Over the past three months, BAX stock has declined 8.7%, outperforming the iShares U.S. Medical Devices ETF’s (IHI) 10.2% losses during the same time frame.

Shares of BAX dipped 24.1% on a six-month basis and fell 49.4% over the past 52 weeks, notably underperforming IHI’s six-month losses of 7.3% and 6.5% over the last year.

To confirm the bearish trend, BAX has been trading below its 50-day moving average since early March. The stock is trading below its 200-day moving average over the past year, with a minor fluctuation.

Baxter's underperformance is attributed to unfavorable product mix, inventory adjustments, and higher manufacturing costs, with improvements expected in the second half of 2026.

On Feb. 12, BAX shares tumbled 16% after reporting its Q4 results. Its adjusted EPS of $0.44 missed Wall Street expectations of $0.53. The company’s revenue was $3 billion, surpassing Wall Street forecasts of $2.8 billion. BAX expects full-year adjusted EPS in the range of $1.85 to $2.05.

BAX’s rival, Becton, Dickinson and Company (BDX) has taken the lead over the stock, with 9.6% gains on a six-month basis and a 9.8% dip over the past 52 weeks.

Wall Street analysts are cautious on BAX’s prospects. The stock has a consensus “Hold” rating from the 16 analysts covering it, and the mean price target of $20.08 suggests a potential upside of 14% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)