/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

Oracle (ORCL) has managed to quietly become one of the most interesting names in the enterprise software/cloud infrastructure space, especially as artificial intelligence (AI) spending ramps up in the tech industry. However, investors are focusing their attention on the company's next quarterly results, set to be announced on March 10. This is an important event that could shape investors' perceptions of Oracle’s cloud infrastructure play.

This is an important time for Oracle. Over the last year, hyperscalers and enterprises alike have ramped up their spending on AI infrastructure, databases, and cloud services. The company has placed itself at the center of the AI revolution with its Oracle Cloud Infrastructure (OCI) service. This has been gaining traction among hyperscalers and enterprises that seek alternatives to Amazon's (AMZN) Amazon Web Services, Microsoft's (MSFT) Azure, and Alphabet's (GOOG) (GOOGL) Google Cloud. With artificial intelligence compute services in high demand, investors are awaiting Oracle’s results to see if it can sustain the growth rate it displayed in its latest quarterly report.

About Oracle Stock

Oracle is one of the world’s largest enterprise software companies. The company specializes in database technology, cloud infrastructure, and enterprise applications. It is based in Austin, Texas. Currently, Oracle has a market capitalization of approximately $439 billion, making it one of the largest tech companies in the world.

ORCL stock has been highly volatile over the last 12 months, trading between $118.86 and $345.72. Currently, shares trade at approximately $149.20. Oracle’s weighted alpha is -24.19x, which is indicative of a recent pullback, even as the S&P 500 Index ($SPX) has been stable over the same period.

From a valuation perspective, the stock is trading at 27.25x trailing earnings and 25.85x forward earnings. These are comparable multiples for mature large-cap technology stocks. The stock is trading at a price-to-sales (P/S) ratio of 7.75x and a price-to-cash-flow ratio of 23.15x, implying investors are paying a premium for the growth in the cloud infrastructure business.

At the same time, the return on equity of 70.6% for Oracle indicates the profitability of the enterprise software model.

Oracle Beat on Earnings as Cloud Momentum Accelerated

In December, Oracle reported solid results for Q2 2026, and the results underscored the importance of the cloud platform for the company. For the quarter, the company generated $16.1 billion in revenue, representing a 14% increase from the prior year. At the same time, cloud revenue for the quarter was $8 billion, representing a 34% increase from the prior year.

The most impressive results were from the cloud infrastructure (IaaS) segment, in which the company generated $4.1 billion in revenue, representing a 68% increase from the prior year. At the same time, the SaaS business is doing well, with the company’s Fusion Cloud ERP revenue increasing by 18% and NetSuite revenue increasing by 13%.

Perhaps the most impressive statistic from the quarter is the increase in the company’s remaining performance obligations (RPO), which is a measure of future revenue. For the quarter, the RPO grew by 438% and is now at $523 billion. The growth in RPO is due in part to new commitments from major technology companies, including Meta Platforms (META) and Nvidia (NVDA).

Additionally, Oracle reported GAAP earnings per share (EPS) of $2.10, which represents a 91% increase from the prior year. On the other hand, the non-GAAP EPS came in at $2.26, which represents a 54% increase from the prior year. Moreover, the company reported operating cash flow of $22.3 billion for the last 12 months. This shows that the company has the ability to generate significant cash even when investing in the cloud.

Another notable strategic move was the sale of the company’s holding in Ampere Computing, which indicates that the company is moving away from designing its chips and toward the concept of being chip-neutral, where customers are free to use the chips or GPUs of their choice.

The management also highlighted the strong growth rate in the company’s strategy for the multicloud, where the company integrates its database into other cloud environments such as Amazon Web Services, Microsoft Azure, and Google Cloud. The multicloud database business has seen an increase of 817% year over year, the highest growth rate for the company.

What Do Analysts Expect for Oracle Stock?

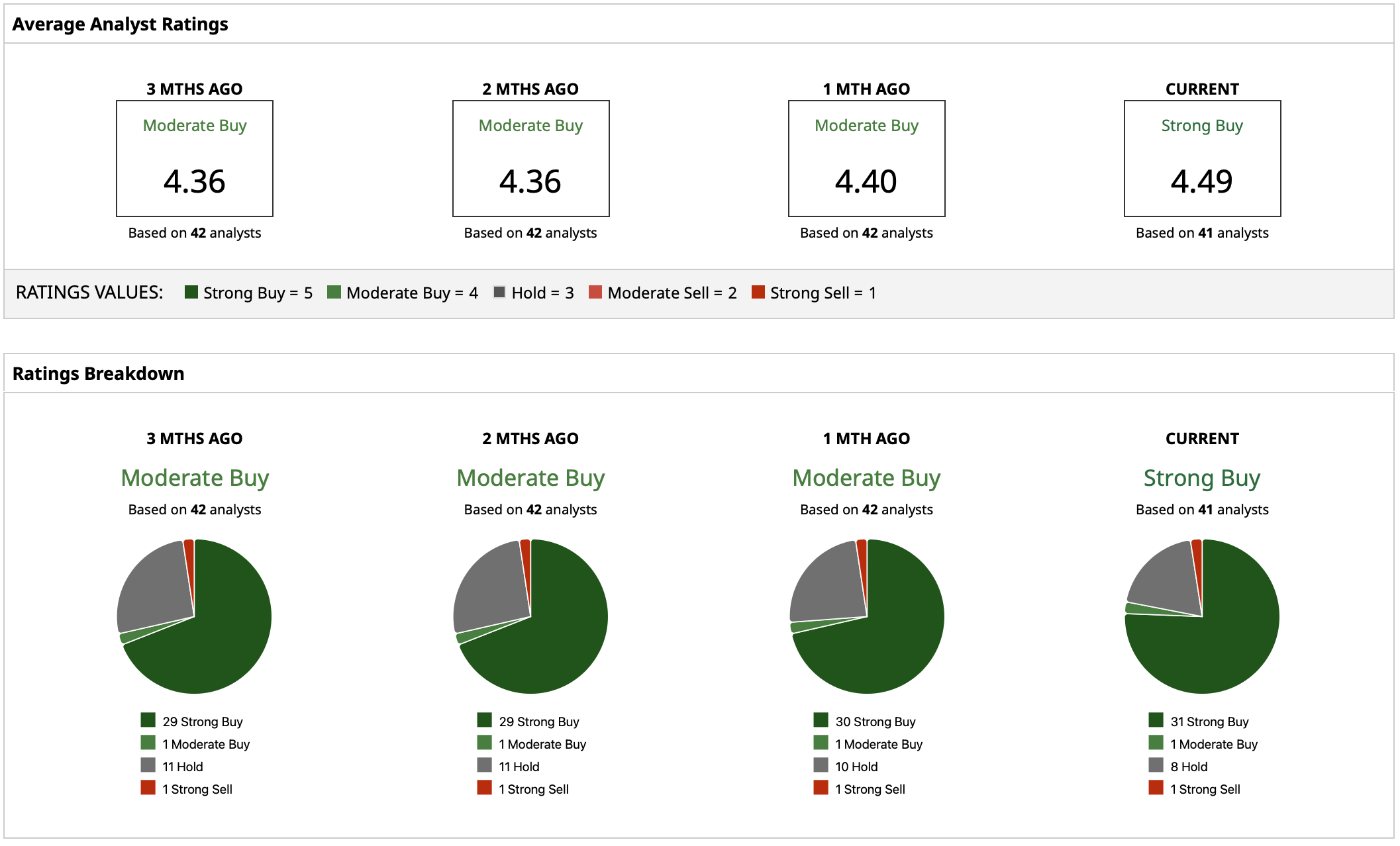

Wall Street analysts are quite positive about the growth prospects for the company in the long term with a “Strong Buy” rating consensus. ORCL stock has a mean price target of $280.18, compared to the current price of around $149. That indicates upside potential of about 88%, implying that the growth story for the company’s cloud infrastructure is still in the early stages. Analysts are quite uncertain about the growth prospects for the company’s AI infrastructure business, as the price targets vary from a low of $155 to a high of $400.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)