/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

San Jose, California-based Super Micro Computer, Inc. (SMCI) develops and manufactures advanced server and storage solutions built on a modular and open architecture. Valued at $19.6 billion by market cap, the company offers servers, storage systems, motherboards, full racks, chassis, and accessories worldwide.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and SMCI definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the computer hardware industry. SMCI excels in delivering customized modular solutions thanks to its innovative and open-standard architecture. Its adaptable product portfolio spans servers, storage, networking devices, and software, giving the company a competitive edge and strong market positioning.

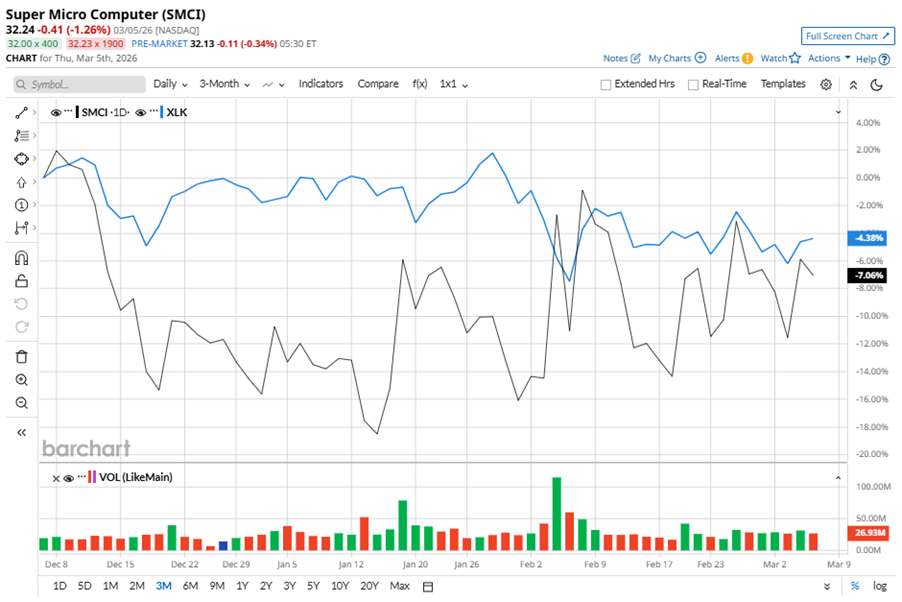

Despite its notable strength, SMCI slipped 48.3% from its 52-week high of $62.36, achieved on Jul. 31, 2025. Over the past three months, SMCI stock declined 7.1%, underperforming the Technology Select Sector SPDR Fund’s (XLK) 4.4% losses during the same time frame.

Shares of SMCI rose 10.2% on a YTD basis, outperforming XLK’s 2.6% dip over the same time frame. However, the stock dipped 17.1% over the past 52 weeks, significantly underperforming XLK’s 26.5% returns over the same time frame.

To confirm the bearish trend, SMCI is trading below its 200-day moving average since early November, 2025. However, the stock has been trading above its 50-day moving average since early February, with some fluctuations.

SMCI's underperformance is driven by gross margin decline due to unfavorable customer and product mix, higher freight costs, component shortages, and a shift toward large customers with stronger pricing leverage.

On Feb. 3, SMCI reported its Q2 results, and its shares closed up by 13.8% in the following trading session. Its adjusted EPS of $0.69 beat Wall Street expectations of $0.49. The company’s revenue was $12.7 billion, beating Wall Street forecasts of $10.4 billion. For Q3, the company expects revenue to be $12.3 billion.

In the competitive arena of computer hardware, Dell Technologies Inc. (DELL) has taken the lead over SMCI, showing resilience with a 16.4% uptick on a YTD basis and a 50.7% gain over the past 52 weeks.

Wall Street analysts are reasonably bullish on SMCI’s prospects. The stock has a consensus “Moderate Buy” rating from the 19 analysts covering it, and the mean price target of $42.76 suggests a notable potential upside of 32.6% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)