/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

CoreWeave (CRWV) is a specialized cloud computing company delivering GPU-powered infrastructure tailored for AI workloads, machine learning, VFX rendering, and high-performance computing. It provides scalable access to Nvidia (NVDA) GPUs via Kubernetes clusters, auto-scaling storage, and developer-friendly tools, helping enterprises train massive models faster and cheaper than general clouds.

Founded in 2017 by ex-crypto miners, CoreWeave is headquartered in Livingston, New Jersey. The company has data centers primarily in the U.S. (28-plus sites) and is expanding intp Europe (the U.K., Norway, Sweden, Spain), supporting global clients.

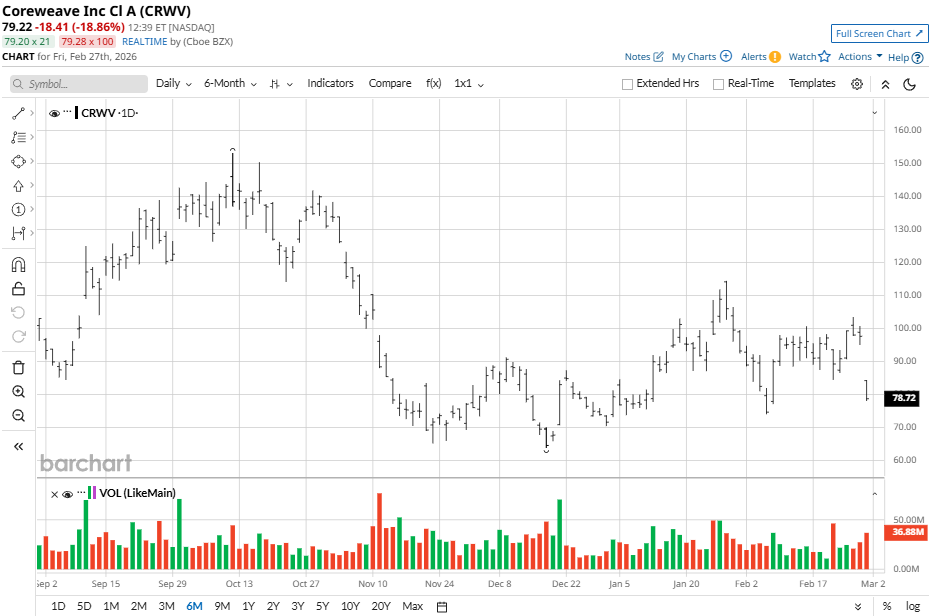

CoreWeave Stock Drops From Highs

Since its March 2025 initial public offering (IPO) at $40, CRWV stock has been highly volatile amid AI hype. Currently trading near $79, the stock is up sharply from its 52-week low of $33.51 but down 58% from the 52-week high of $187. Recent five-day action shows that the stock has slipped 21% while the past one-month period reveals a 6% drop. Mixed with the 50-day moving average (MA) at $88.16 versus the 200-day MA at $110.06, the 52-week range reflects massive swings, while year-to-date (YTD) the stock is up 8% despite being off its highs.

Coreweave stock underperforms compared to the Nasdaq Composite ($NASX), with the index showing a positive six-month report, gaining 4% against CRWV stock’s 12% fall. Still, AI catalysts keep CRWV punchier short-term versus index steadiness.

CoreWeave Reports Mixed Results

CoreWeave crushed revenue expectations in the fourth quarter of 2025 with $1.57 billion in sales — up 110% year-over-year (YOY) — fueled by surging AI GPU demand from hyperscalers like Microsoft (MSFT) and OpenAI. Full-year revenue came in at $5.1 billion, marking 168% YOY growth. However, EPS missed at a loss of $0.89 versus an estimated loss of $0.49, as net loss ballooned to $452 million amid aggressive expansion. Shares slipped post-earnings on conservative guidance.

Additional key metrics for the period include adjusted EBITDA of $898 million (slightly missing estimates of $929 million) with a 57% margin. Backlog exploded to $66.8 billion, while customer concentration eased. Operating expenses rose to $1.66 billion during Q4, while interest hit $388 million. Strong liquidity supports CoreWeave's capex ramp.

The company provided a cautious outlook to investors with projected Q1 revenue of $1.9 billion to $2 billion, coming in below the $2.29 billion estimate. For fiscal 2026, the company foresees $12 billion to $13 billion in revenue, adjusted operating income of $900 million to $1.1 billion, and capex of $30 billion to $35 billion (contract-backed). Margins trough early then expand to low double-digits by year-end, prioritizing capacity for the AI boom.

CoreWeave Is Looking to Fund the Meta Deal

CoreWeave is negotiating $8.5 billion in delayed-draw term loans from banks like Morgan Stanley (MS) and Mitsubishi UFJ Financial Group (MUFG) to fund massive cloud computing expansion for Meta Platforms (META). The loan leverages CoreWeave's $14.2 billion contract with Meta from last year, covering GPU-powered AI services, plus a newly revealed $5 billion-plus deal from early 2026, totaling over $19 billion in backing.

This structure lets CoreWeave draw funds incrementally as needed rather than upfront, with Meta's strong credit profile likely securing an investment-grade rating despite CoreWeave's junk status, slashing interest costs. Banks are quietly syndicating to others, targeting a March 2026 close.

The move fits CoreWeave's debt-heavy growth strategy amid the AI infrastructure frenzy. Existing debt hit $14 billion (including $8 billion in prior GPU loans) plus $2.25 billion convertibles. AI firms tapped $200 billion-plus in private debt last year, and 2026 could double that.

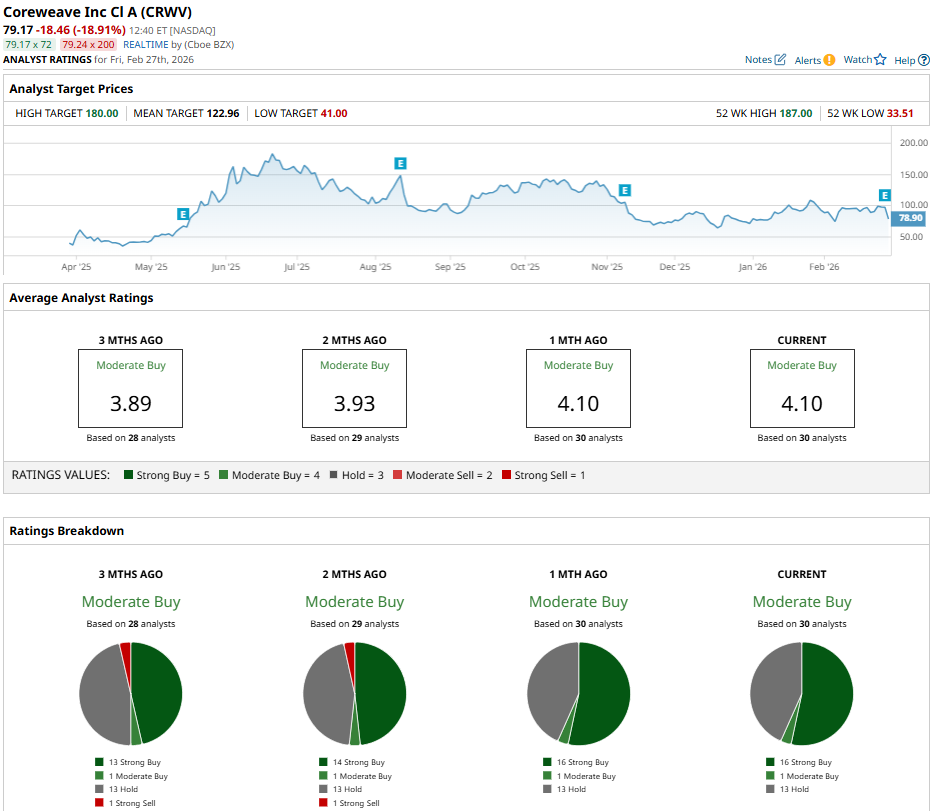

Should You Buy CRWV Stock?

As CRWV stock continues to suffer from volatility, analysts offer a consensus “Moderate Buy” rating with a mean price target of $120.61, reflecting potential upside of 53% from current levels. The stock has been rated by a total of 30 analysts, with 16 “Strong Buy” ratings, one “Moderate Buy” rating, and 13 “Hold” ratings.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)