/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

When Michael Burry speaks, Wall Street usually listens. The investor made famous by “The Big Short” has once again stirred the pot, and this time questioning whether the artificial intelligence (AI) boom is starting to look a little too expensive. His concern is the sheer scale of data center spending and the effect it is having on cash flow, balance sheets, and reported earnings.

Burry has openly challenged heavyweights like Oracle Corporation (ORCL), Alphabet (GOOGL), and Caterpillar (CAT), asking when does this AI infrastructure spending actually end? He argues companies are borrowing aggressively and potentially stretching accounting to soften the blow of soaring capital expenditures.

Critics argue Burry’s structural analysis may be sharp, but his timing has historically tested investors’ patience. Markets, they say, can stay enthusiastic longer than skeptics expect. Still, Burry pushes back, defending his track record and insisting excess capital cycles rarely end smoothly.

So, if you want to invest like Michael Burry, it might not be about chasing the AI rally. It could be about knowing which popular names to step away from now.

Stock #1: Oracle

Founded in 1977, Texas-based Oracle is a global leader in enterprise information technology, with a market capitalization of approximately $417.8 billion. The company is best known for its Oracle Database and autonomous systems, which serve as critical infrastructure for businesses worldwide. Oracle offers a broad portfolio of cloud-based applications, including ERP, HCM, and NetSuite, supporting organizations across industries.

With expanding capabilities in cloud infrastructure, hardware, and consulting services, Oracle plays a central role in modern enterprise computing. The company continues to focus on scalable, secure solutions that support data-driven operations and long-term digital transformation.

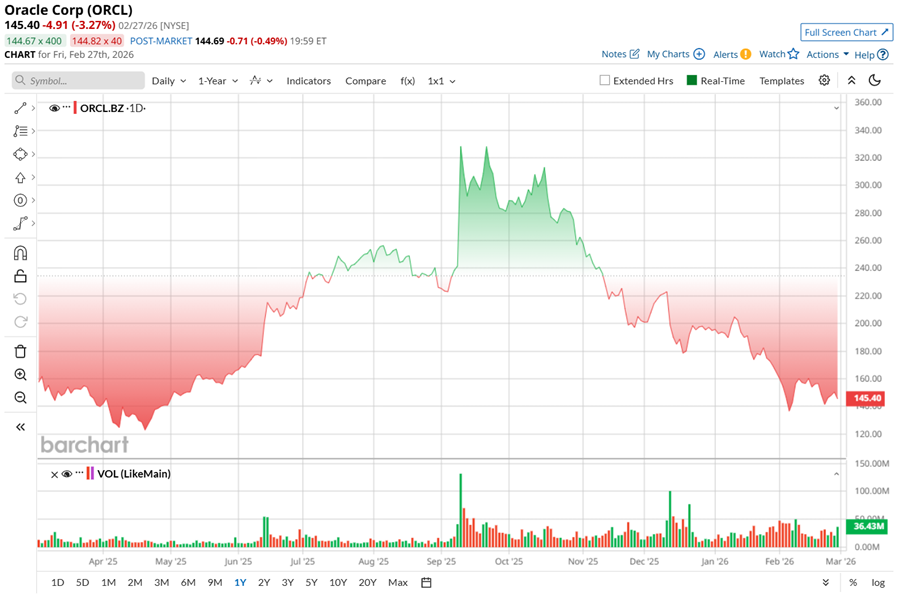

Oracle was once the market’s AI infrastructure darling. Fueled by cloud acceleration and AI excitement, the stock rose impressively last year. The real jump came in September, when a solid quarterly report sent shares soaring nearly 36% in a single session, pushing ORCL to a peak of $345.72 on Sept. 10. At that point, investors were fully bought into Oracle’s cloud reinvention story.

But markets shift. Since October, sentiment has cooled as heavy spending and balance-sheet leverage grabbed attention. From its high, the stock is now down 58%. Consequently, over the past 52 weeks, shares are down about 10.8%, with a sharp 26.36% slide in just the last three months.

Investors are concerned and are tied to spending. Oracle raised $18 billion in new debt to fund data center construction, pushing total debt above $100 billion. It also joined the massive Stargate AI project alongside OpenAI and SoftBank (SFTBY), a $500 billion infrastructure push. The opportunity is enormous, but so is the investment.

Technically, momentum remains cautious, though rising trading volume suggests investors are watching closely for signs of stabilization.

Valuation wise, ORCL stock is priced at roughly 19.8 times forward non-GAAP earnings, which sits below its historical average and looks reasonable relative to the broader sector.

Nevertheless, leverage is part of the story. With a debt-to-equity ratio above 3 and interest coverage just under 5, the balance sheet offers less room for error if growth slows. Still, Oracle continues to reward shareholders, paying dividends for 16 years and raising them for 11 consecutive years. Its latest $0.50 per share quarterly payout equals $2 per share on an annualized basis, yielding about 1.38%.

On Dec. 10, Oracle Corporation rolled out its fiscal second-quarter 2026 numbers, generating revenue of $16.06 billion, up 14% year-over-year (YOY). Cloud once again carried the load, climbing 34% to $8 billion. Within that, cloud infrastructure demand was on fire, soaring 68% and more than making up for a 3% dip in legacy software sales.

Meanwhile, non-GAAP EPS jumped 54% annually to $2.26, beating expectations. Backlog also exploded, with remaining performance obligations (RPO) hitting $523 billion, up a staggering 438% YOY, giving Oracle years of contracted revenue visibility.

Oracle is going all-in on infrastructure, building out data centers to power its expanding cloud footprint. In Q2 alone, capital expenditures surged to about $12 billion. That aggressive spending pushed free cash flow into negative territory, swinging to a $10 billion outflow for the quarter. This serves as aa reminder that this cloud pivot comes with a hefty price tag.

Management made it clear the spending wave is not slowing down. Oracle Corporation now expects fiscal 2026 CapEx to hit roughly $50 billion, $15 billion above its prior outlook. Unlike some bigger peers, Oracle is funding much of this through borrowing. Including operating leases, total debt has risen sharply, and credit default swap prices have climbed to levels last seen during the 2008 crisis.

Still, management projects cloud revenue growth between 37% and 41% in Q3, with total revenue expected to rise by 16% to 18%. Non-GAAP EPS growth is anticipated between 12% and 14%, and even penciling in an extra $4 billion of revenue in fiscal 2027.

Analysts tracking Oracle expect the tech stock’s fiscal 2026 EPS to grow 36.6% YOY to $6.01, followed by a 4.8% surge to $6.30 in fiscal 2027.

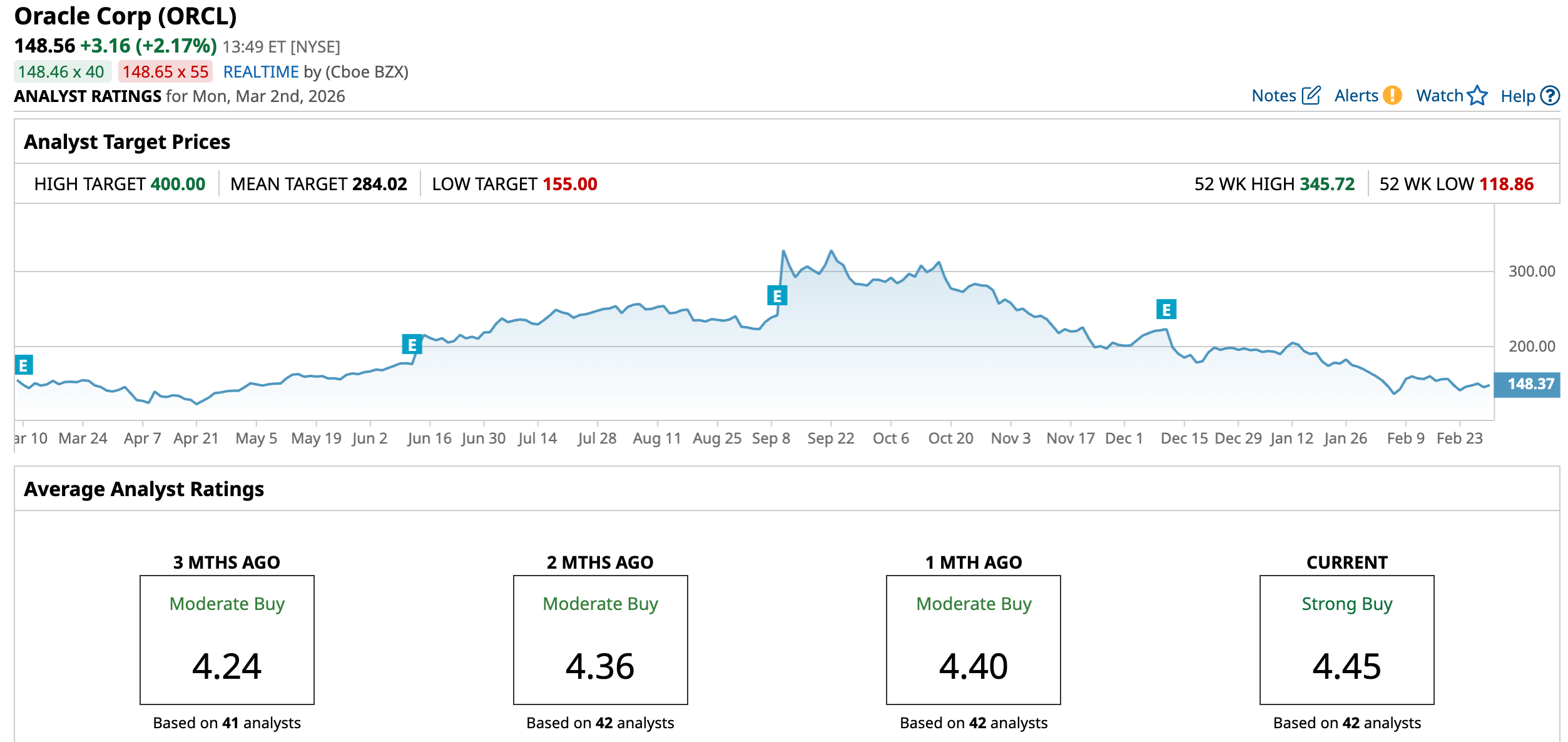

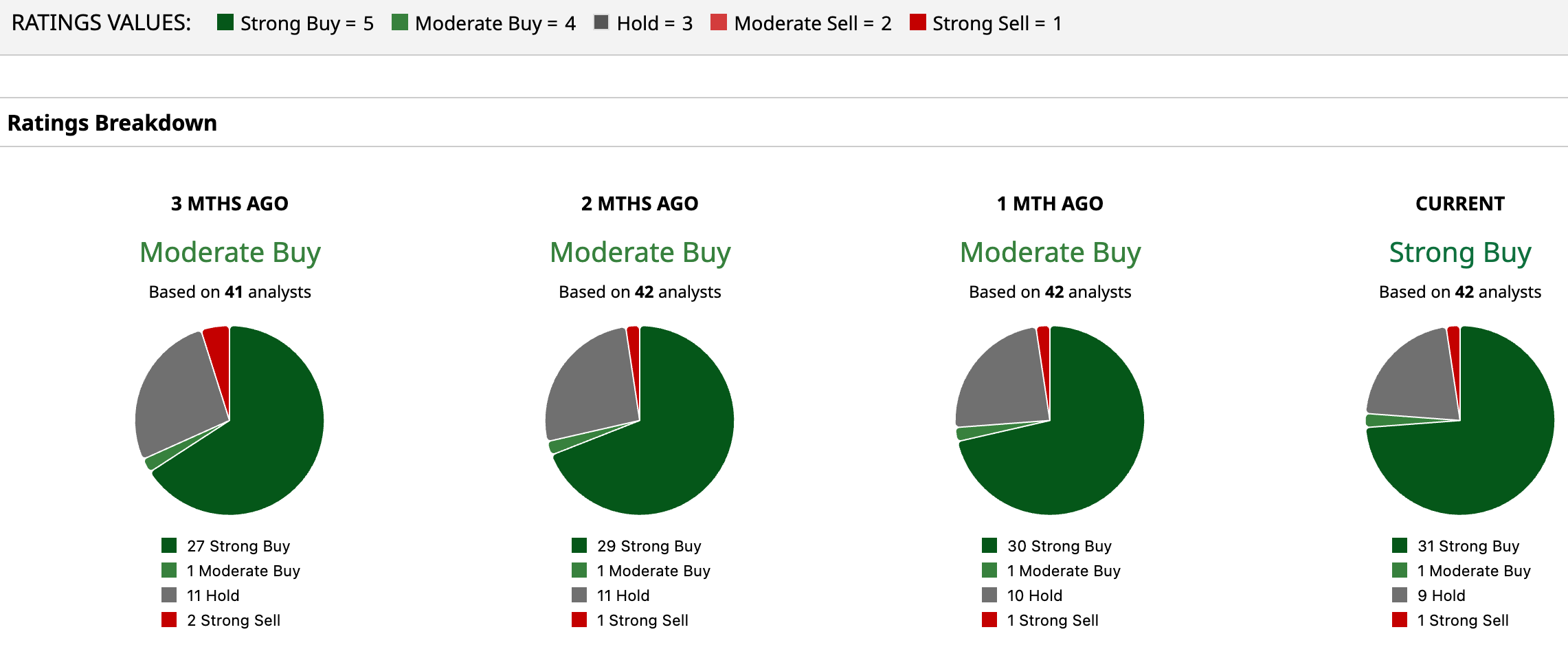

Overall, analysts are upbeat on ORCL, giving a consensus “Strong Buy” rating, an upgrade from a “Moderate Buy” rating a month back. Of the 42 analysts rating the stock, a majority of 31 analysts rate it a “Strong Buy,” one advises a “Moderate Buy,” nine analysts are playing it safe with a “Hold” rating, and the remaining one is outright skeptical, having a “Strong Sell” rating.

The tech stock’s consensus price target of $284.02 implies 91.2% upside potential. Meanwhile, the Street-high target of $400 suggests the stock could rally as much as 169%.

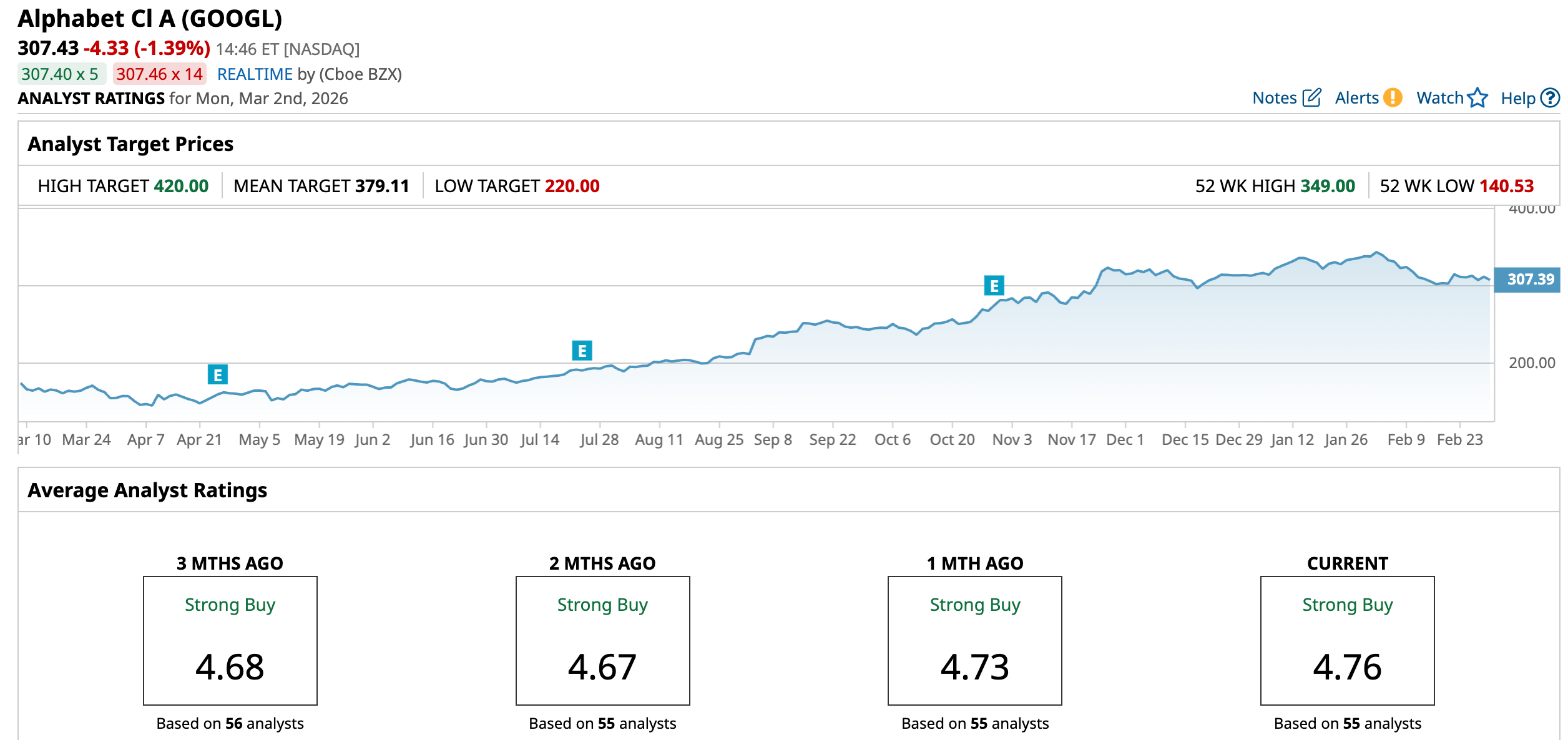

Stock #2: Alphabet Stock

California-based Alphabet hardly needs an introduction in global technology circles. Valued at roughly $3.77 trillion by market cap, the company is one of Silicon Valley’s most influential forces. Far beyond Search, Alphabet has expanded into AI, cloud infrastructure, autonomous mobility through Waymo, and advanced research led by DeepMind. Its Gemini models reflect an ambition not just to join the AI race, but to define it.

The market has taken note. Fresh confidence in Google’s AI game plan and steady cloud growth has fueled a solid run in the stock, keeping Alphabet firmly planted among the world’s most valuable companies.

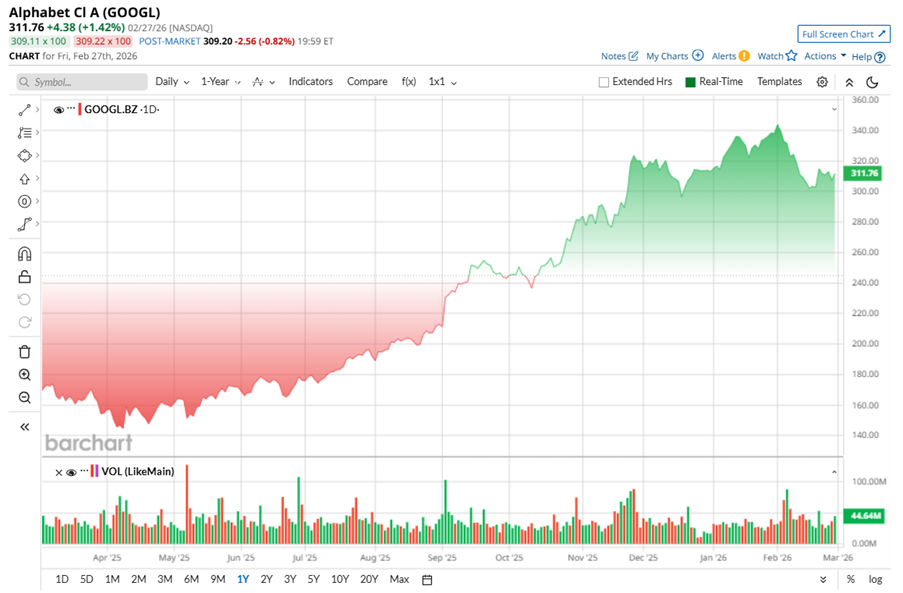

Alphabet has delivered a powerful rally over the past year. The stock recently touched a 52-week high at $349 in early February, reflecting strong investor conviction around its AI strategy and cloud momentum. Since that peak, however, shares have corrected about 10.7% and are down roughly 6.8% over the past month, as the market reassesses the scale and timing of returns from Alphabet’s elevated AI-related capital spending.

Technically, the pullback looks more like a pause after a strong rally rather than a major breakdown. Even after the recent decline, GOOGL remains up 85% over the past 52 weeks and over 50% in the last six months. Trading volumes are also picking up again, which suggests investors are still actively watching and stepping in at key levels.

After a solid run over the past year, Alphabet stock does not exactly look cheap. It trades around 27 times forward adjusted earnings, a bit above its sector average and historical median. Still, that multiple feels reasonable for a company growing revenue in the high teens and seeing strong momentum in Google Cloud. This is not a one-trick business either – its diversified model, strong balance sheet, and now a dividend add stability.

Alphabet wrapped up 2025 with a headline-grabbing fourth-quarter report on Feb. 4, showing just how central AI has become to its growth story. Revenue climbed 18% YOY to $113.8 billion, beating Wall Street’s expectations. EPS amounted to $2.82, up 31% annually, as both Search and Cloud delivered strong performances. For fiscal 2025, revenue crossed the $400 billion mark for the first time.

Google Services, which includes Search, YouTube, and subscriptions, generated $95.9 billion, up 14%. Search and other ad revenue rose 17% to $63.1 billion, while YouTube ads grew 9% to $11.4 billion.

Google Cloud stood out, with revenue surging 48% to $17.7 billion as AI demand accelerated. Backlog jumped to $240 billion. Operating income rose 31% to $31 billion, though heavy capital spending of $91.4 billion for the year pressured free cash flow margins.

Yet, Alphabet ended the year with over $126 billion in cash, supporting continued buybacks and dividends. The company funded $5.5 billion in buybacks and $2.5 billion in dividends in Q4 alone.

Despite the strong numbers, shares dipped as investors questioned how quickly AI investments will translate into sustained profits.

Looking ahead, management expects 2026 capital spending to land between $175 billion and $185 billion, almost double what it spent in 2025. Most of that jump is aimed at expanding AI and cloud capacity to meet rising demand. The higher spending may squeeze near-term FCF, but management is betting big on AI agents, smarter Search, and rising enterprise adoption to drive long-term growth.

Wall Street analysts tracking Alphabet sees its bottom line growing steadily. While fiscal 2026 EPS is projected to rise by 7.3% YOY to $11.60, in the next fiscal year, it is anticipated to surge bY 14.7% annually to $13.31.

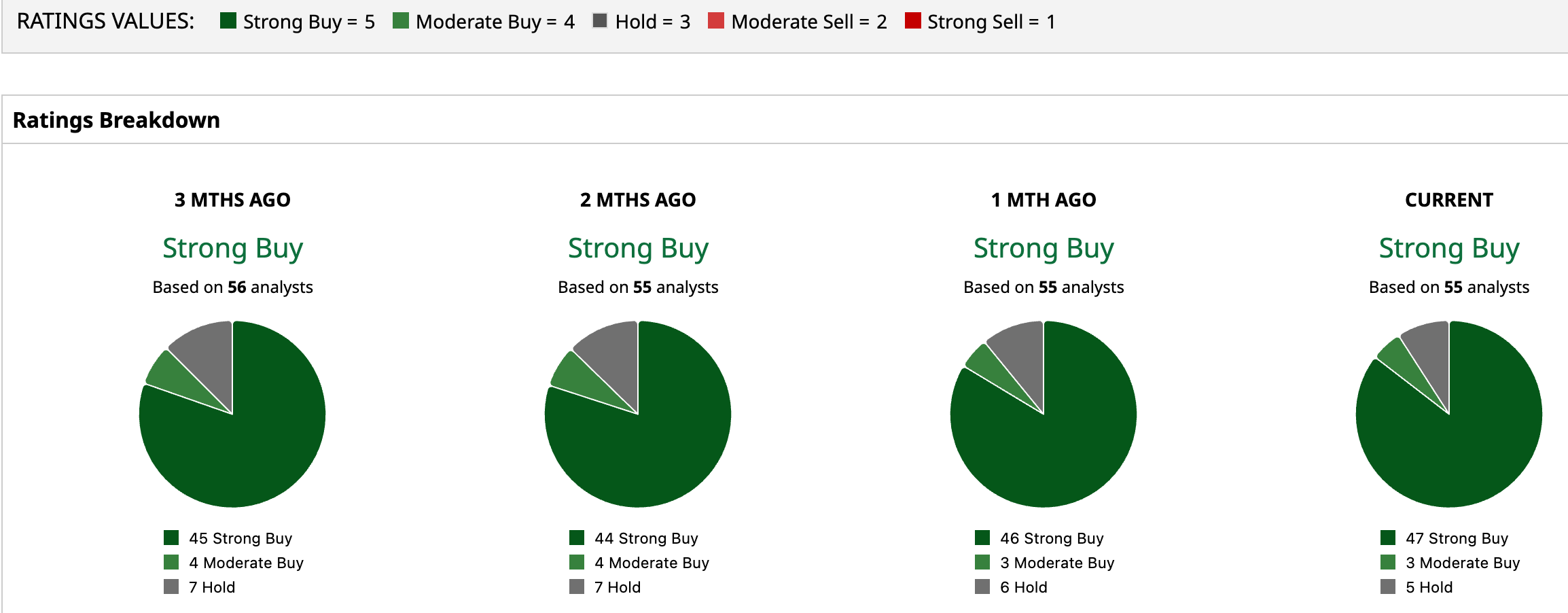

Analysts monitoring GOOGL are bullish, awarding it a “Strong Buy” rating overall. Out of 55 analysts, 47 recommend a “Strong Buy,” three suggest a “Moderate Buy,” and five are playing it safe with a “Hold” rating. The average price target of $379.11 suggests a 23% upside potential from here. Meanwhile, the Street-high target of $420 suggests GOOGL stock could rise 36.6%.

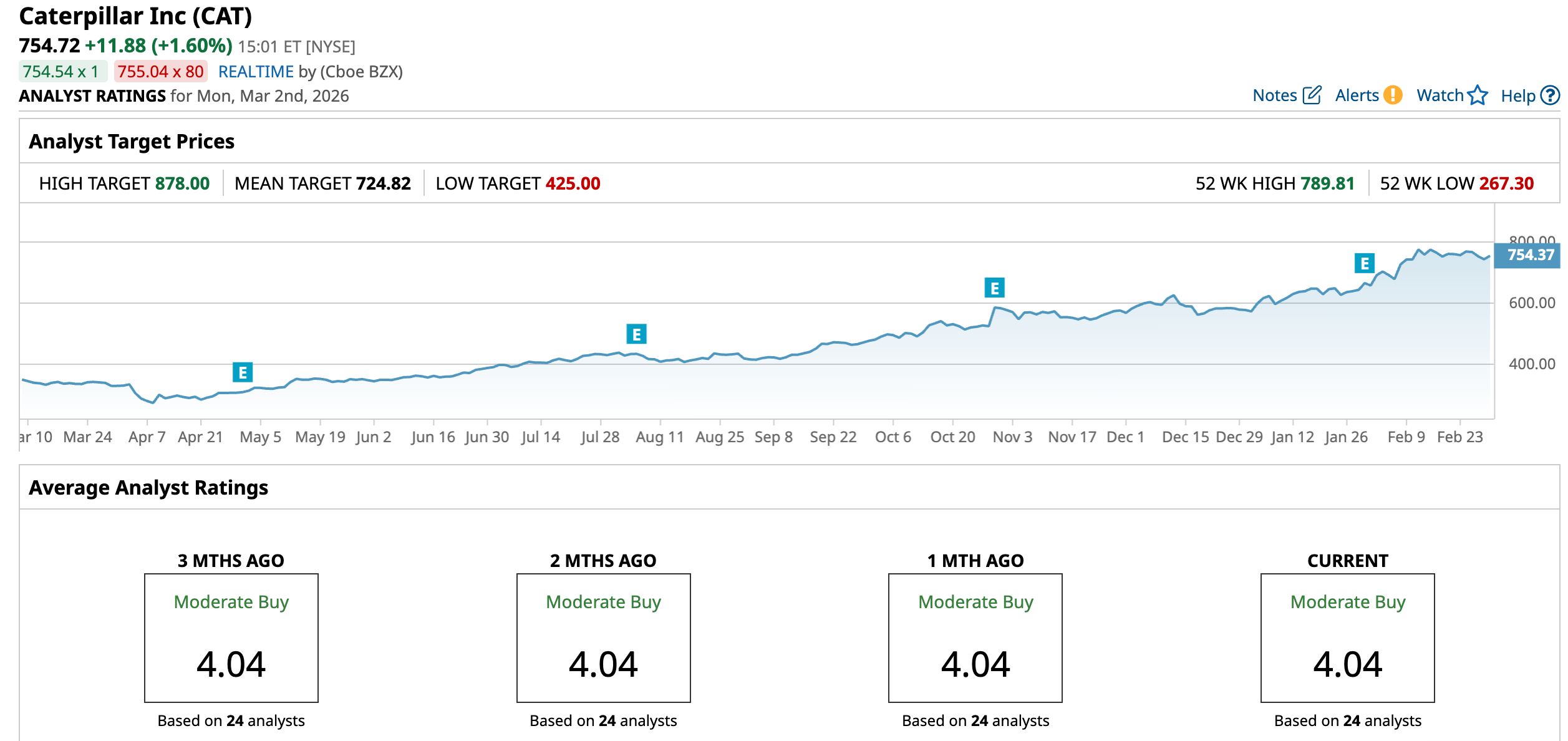

Stock #3: Caterpillar

Caterpillar has been a driving force in heavy machinery since 1925. It is the world’s leading manufacturer of construction and mining equipment, diesel engines, and locomotives. The Irving, Texas-based company pioneered track-type tractors and continues to shape global infrastructure through innovative and increasingly sustainable machinery.

With a market capitalization of about $345.6 billion, Caterpillar operates across construction, resource industries, energy and transportation, and financial products, delivering end-to-end solutions that power projects and industries worldwide.

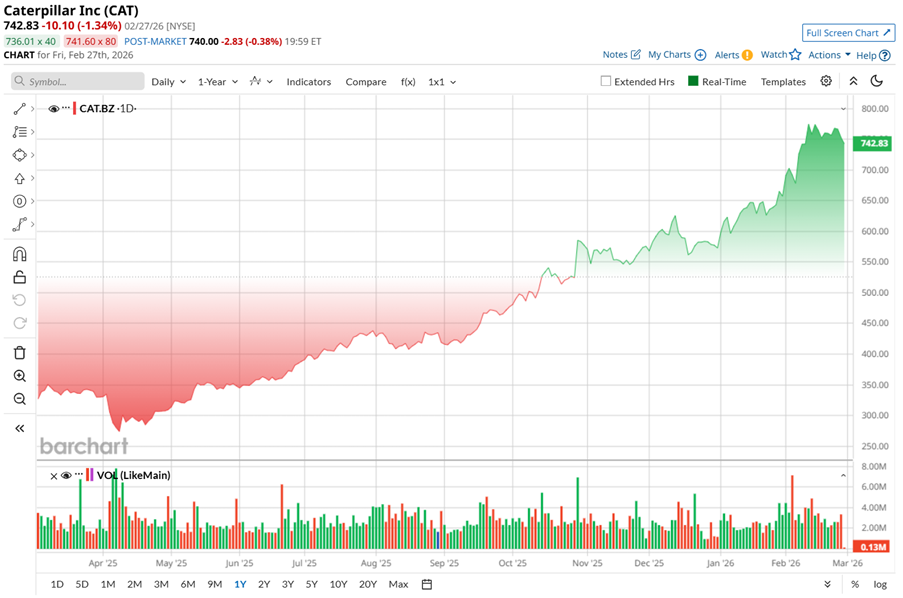

Caterpillar had an impressive run over the past few years. CAT stock has jumped about 118.5% over the past year and 80.65% in the last six months, reflecting a rebound in its core business cycle. A recovery in agriculture and manufacturing activity has driven higher equipment orders, while large-scale data center buildouts have added incremental demand. Caterpillar supplies critical machinery and power systems used in these projects, giving it direct exposure to digital infrastructure spending.

On renewed optimism around manufacturing momentum, shares touched a high of $789.81 on Feb. 12. The stock is now roughly 4.5% below that level, suggesting more like a healthy pause after a strong run.

Valuation-wise, Caterpillar’s shares are priced at 32.78 times forward adjusted earnings. On the surface, that multiple may look stretched. But investors appear willing to pay up, betting on the company’s operational resurgence, healthy backlog, and long-term infrastructure and energy tailwinds.

When it comes to dividends, Caterpillar has built serious credibility. It has paid dividends since 1933 and has increased them for 32 consecutive years, earning a place in the S&P 500 Dividend Aristocrats Index. On Feb. 18, the company paid a quarterly dividend of $1.51 per share, translating to an annualized dividend of $6.04 and a 0.8% yield. With a payout ratio of just 31.1%, those dividends remain comfortably supported by earnings.

Caterpillar delivered a stronger-than-expected fourth-quarter and fiscal 2025 results on Jan. 29, and the stock gained 3.4% intraday. Revenue for Q4 jumped 18% YOY to a record $19.1 billion, powered largely by solid demand across its machinery, power and energy (MP&E) business, which grew 18.7% annually.

Not everything was smooth. Operating profit slipped 9% to $2.66 billion, mainly due to higher manufacturing costs and tariff pressures. Still, adjusted EPS edged up to $5.16, comfortably ahead of what analysts were looking for.

For the full year, MP&E segment generated a strong $9.5 billion in free cash flow, despite ramping up capital expenditures by $800 million. Demand remained robust, pushing backlog to a record $51 billion – up $21 billion, or 71% YOY – fueled by solid fourth-quarter orders across its core businesses. Notably, about 62% of that backlog is slated for delivery over the next 12 months, giving the company clear near-term revenue visibility.

For the full year, enterprise operating cash flow for 2025 came in at $11.7 billion, and Caterpillar closed Q4 with $10 billion in enterprise cash. The company also returned significant capital to shareholders, spending $5.2 billion on share repurchases and $2.7 billion on dividends during the year.

Looking ahead to 2026, management expects revenue growth toward the upper end of its long-term 5% to 7% annual target. Caterpillar is also leaning into automation and AI, expanding its work with NVIDIA Corporation (NVDA) to bring more advanced, tech-driven capabilities to heavy industry.

For fiscal 2026, analysts tracking Caterpillar expect its profit to grow 18.9% YOY to $22.66 per share, while for the next year, it is projected to climb 21.6% to $27.56 per share.

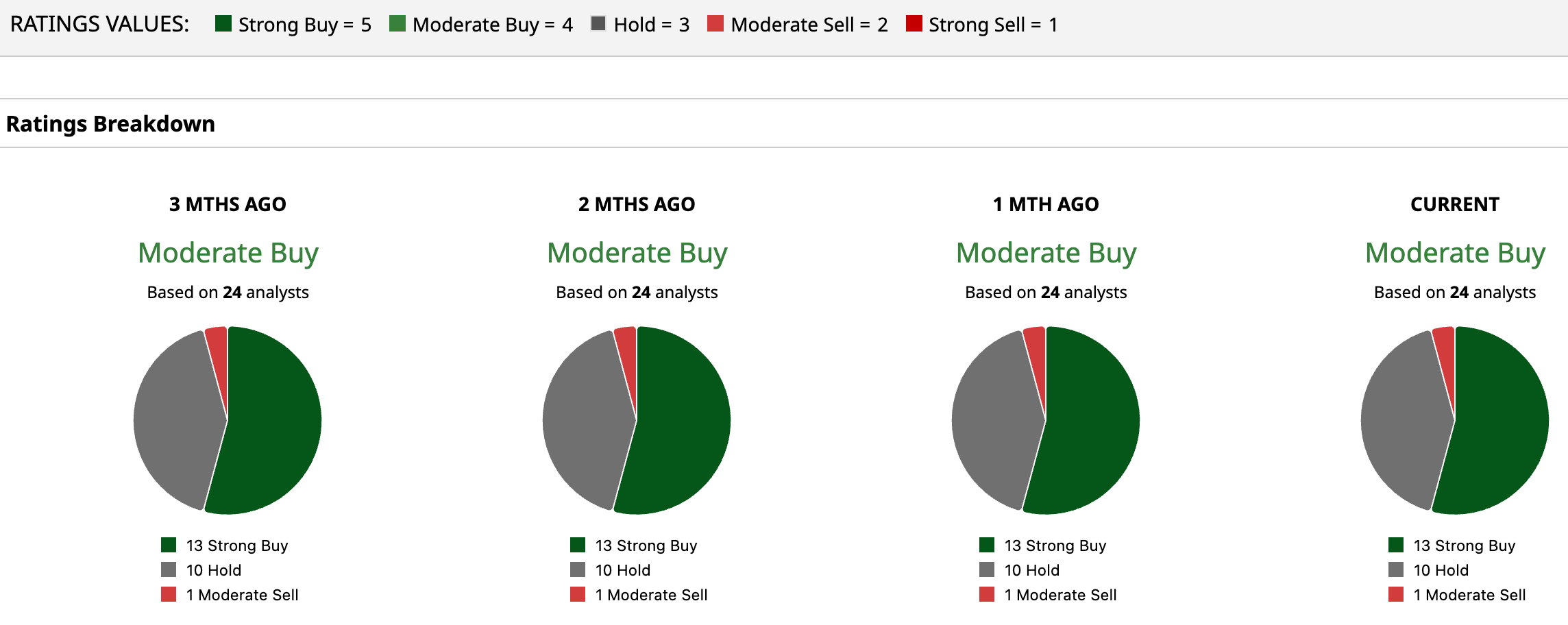

Caterpillar has a consensus “Moderate Buy” rating overall. Of the 24 analysts rating the stock, 13 analysts have given it a “Strong Buy,” 10 analysts are taking a middle-of-the-road approach with a “Hold” rating, and one analyst suggested “Moderate Sell.” While the stock currently trades above the mean price target of $724.82, the Street-high price target of $878 indicates an 16.34% upside.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)