/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

After Intuit (INTU) announced that it had launched an AI partnership with Anthropic, it was clear that the deal will be positive for INTU and that Wall Street is pleased with the agreement. However, given the Street's current skittishness towards software stocks, the significant threat that AI poses to Intuit over the long term, and the fact that INTU stock is still not especially cheap, the shares should be sold at this point.

About INTU Stock

Based in Mountain View, California, Intuit specializes in providing accounting and tax-preparation software to businesses and consumers. Changing hands at a forward price-earnings ratio of 24 times, the stock has a market capitalization of $109.75 billion.

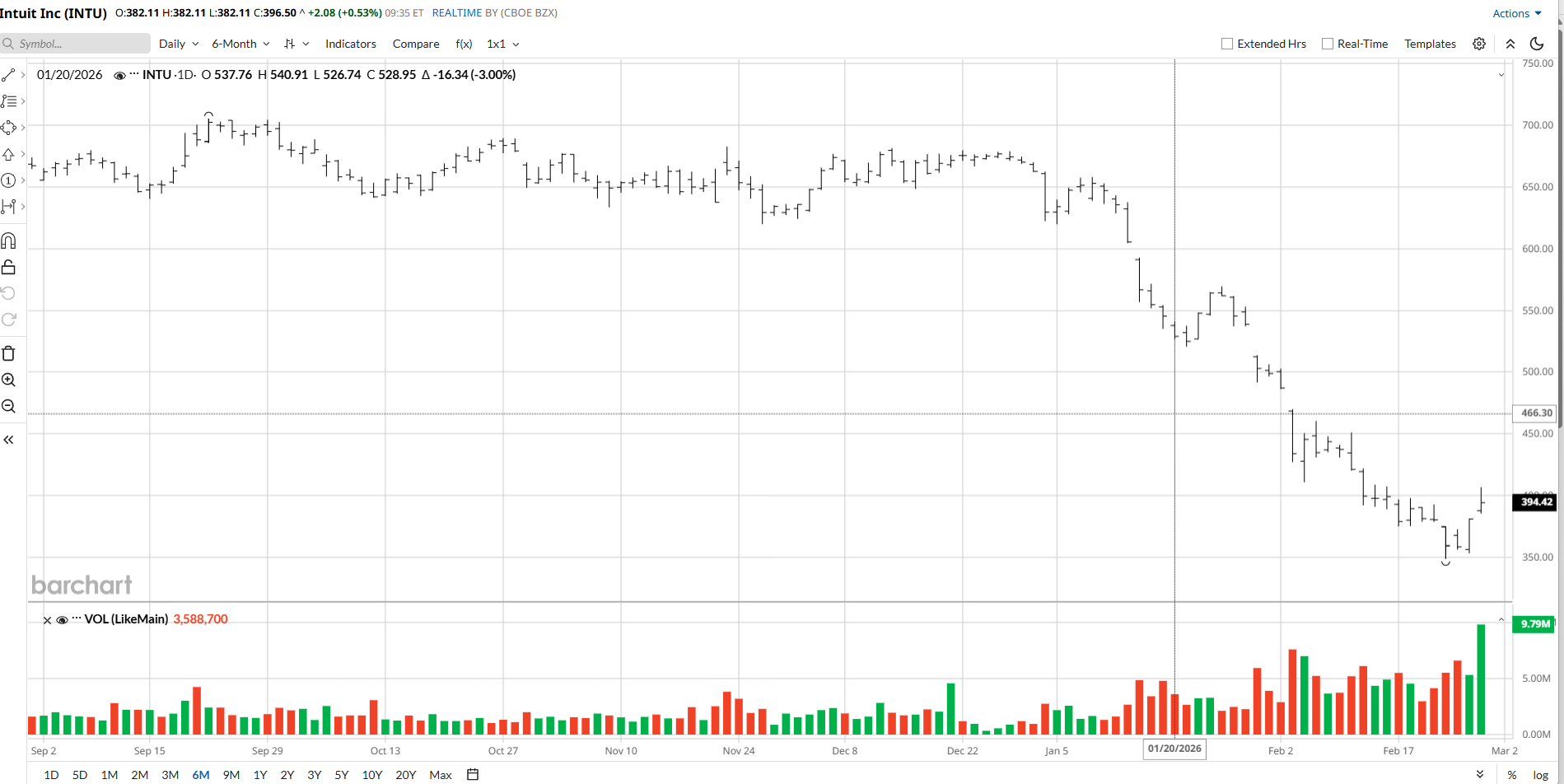

As of the morning of Feb. 27, the shares had slumped 20.6% in the previous month, while they had retreated 37.5% over the preceding three months.

In the company's fiscal second quarter that ended in January, its revenue advanced 17% versus the same period a year earlier to $4.7 billion, while its operating income jumped 44% year-over-year (YoY) to $855 million.

Intuit's Deal With Anthropic

Under the agreement, Intuit will look to provide AI agents to medium-size businesses. Further, Intuit's customers will use Anthropic's technology to create their own AI agents, and Intuit's software will be migrated into Anthropic's offerings.

The agreement is positive for Intuit, if for no other reason than that the deal will likely, in the short-to-medium-term, prevent Anthropic from aggressively looking to take market share from INTU, as the AI start-up is doing to other software makers. Additionally, the agreement will likely be positive for Intuit's brand, as Anthropic appears to be acquiring an image as an AI powerhouse. And finally, given Anthropic's vast experience with AI agents, the deal should indeed help Intuit develop meaningfully more effective AI agents.

Meanwhile, the Street appears to be upbeat on the arrangement, as INTU stock rose from $359.55 on Feb. 23, the day before the transaction was announced, to $394.42 as of the market close on Feb. 26.

Finally, there are multiple reasons why the Street's worries about AI supplanting software companies are probably exaggerated.

Worries About AI's Threat to Software Makers Are Overdone

First, AI needs huge amounts of data in order to function. In fact, according to one study, “42% of enterprises need access to eight or more data sources to deploy AI agents successfully.” Another publication noted that “AI agents are only as good as the data they’re trained on.” Moreover, the agents don't need just any data; they need “the right data.” Consequently, for years Anthropic and its competitors will probably have difficulty obtaining sufficient data to ensure that their agents' conclusions are always or nearly always accurate. Indeed, AI systems are known for sometimes relying on faulty data.

One point related to the previous issue is that, certainly in the near-to-medium term, many companies just won't feel nearly as comfortable relying on AI agents as they do depending on the software that they have used for many decades. After all, the public has not been aware of AI agents for very long, and, as I noted above, they've been known to occasionally make mistakes.

In light of these realities, I do not expect Intuit's business to get disrupted for at least a few years.

The Street's Worries About Software and the Long-Term Threat

One concept that I've learned over the years is that it takes a very long time for many on the Street to give up their misconceptions. For example, it took nearly all of both 2022 and 2023 for most investors and analysts to internalize the idea that rising interest rates would not produce a nasty recession, and, despite all of Tesla's (TSLA) many problems and struggles, its valuation still remains sky-high.

Therefore, even if there is not significant evidence supporting the “all software companies may be doomed soon” theory that has gripped the Street, it could easily take a year or two for Intuit and its peers to rally.

But on the other hand, in two or three years, after Anthropic and other AI companies have had time to greatly improve their agents and access more data, they could pose a fairly large threat to Intuit and many other software firms.

Valuation and the Bottom Line on INTU Stock

Intuit is not very cheap, as the shares are changing hands at a forward price-earnings ratio of 24 times.

Given this point, along with the two threats that I outlined in the section above, I recommend selling INTU stock.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)