/An%20image%20of%20a%20hand%20holding%20a%20smartphone%20with%20the%20Pinterest%20logo%20and%20app%20background_%20Image%20by%20FellowNeko%20%20via%20Shutterstock_.jpg)

High-growth tech stocks often live and die by institutional conviction. When a high-profile investor trims a position, it can spark fresh debate, even if the broader story hasn’t fundamentally changed. That’s especially true when the seller is Cathie Wood, whose Ark Invest funds have built a reputation for making bold, long-term bets on disruptive platforms.

Last week, Wood’s flagship exchange-traded funds (ETFs) reduced exposure to several names, including Pinterest (PINS). According to recent trade disclosures, Ark Invest funds sold shares of PINS as part of broader portfolio adjustments that included cuts to DraftKings (DKNG) and Teradyne (TER) while adding to AMD (AMD).

So, does Cathie Wood selling Pinterest stock mean it’s time for investors to follow her lead? Or could this be an opportunity hiding in plain sight? Let’s take a closer look.

Pinterest Faces Headwinds Amid Cautious Spending

Pinterest has grown into a global visual discovery platform with 619 million monthly active users, generating nearly all of its revenue from digital advertising. But like other ad-dependent tech companies, it’s operating in a cautious marketing environment. In its latest quarter, management flagged retail tariff pressures and signaled modest near-term headwinds as brands tightened budgets.

To navigate that shift, Pinterest is reorganizing its global sales team under new Chief Business Officer Lee Brown, aiming to deepen penetration in mid-market and international accounts, a move that could broaden its advertiser base but temporarily slow growth.

That uncertainty has been reflected in PINS stock’s performance. Shares rallied early in 2025 and approached $40 around mid-year, near the 52-week high of $39.93, before losing momentum later in the year. By year-end, PINS stock had retreated meaningfully from those levels and has struggled to recover so far in 2026, declining about 31% year-to-date (YTD). In short, we can say that Pinterest has lagged behind many technology peers as higher interest rates and valuation pressure have weighed on growth-oriented names.

Despite the underperfomance, investors have serious concerns about the company's valuation. Pinterest has an EV/EBITDA of 28, significantly higher than the sector median of 10, indicating that PINS stock is trading at a premium. Additionally, the price-to-sales (P/S) ratio of 2.67 times is more than double the sector median, suggesting the stock is considerably overpriced.

Cathie Wood’s Recent Pinterest Sale

Ark Invest recently disclosed that its funds sold a small stake in Pinterest. On Feb. 19, filings show the sale of about 15,894 shares worth roughly $2.6 million. This sale attracted attention because Cathie Wood's Ark Blockchain & Fintech Innovation ETF (ARKF) and Ark Next Generation Internet ETF (ARKW) have been notable holders of PINS stock. In practice, the sale was tiny, and the stock barely budged on the news. Still, some investors took it as a signal that Ark is trimming its positions in smaller ad-tech names.

For context, Ark Invest's flagship Ark Innovation ETF (ARKK) remains far below its peak. ARKK is still down roughly 50% from its February 2021 high, in contrast to the 79% gain seen by the Nasdaq Composite ($NASX) over the past five-year period. ARKK did rebound by about 35% in 2025, but Ark Invest's funds have lagged greatly over the longer term.

Wood’s funds have been taking profits and shifting into what they see as the next wave of winners. As Wood recently explained, the focus now is on attractive valuations and future optionality. Her pitch is that if investors believed in these names at higher valuations, they should love them even more now. In that light, the small PINS selloff is just one step in Ark’s ongoing portfolio turnover.

Pinterest Q4 Revenue Grows But Misses Expectations

Pinterest shares sank after the company's fourth-quarter report, as results showed continued revenue growth but missed estimates. Revenue was $1.32 billion, up 14% from Q4 2024. By region, U.S. and Canada sales were $979 million, up 9% year-over-year (YOY), Europe delivered $245 million, up 25% YOY, and the Rest of World reached $96 million, up 64% YOY. On a constant-currency basis, sales growth was 13%.

Meanwhile, net income came in at $277 million versus $1.84 billion in Q4 2024. The sharp 85% decline reflected a one-time tax benefit in last year’s quarter.

Free cash flow and liquidity remain solid. Operating cash flow increased 54% YOY to $391 million, and free cash flow climbed 52% to $380 million. Cash and equivalents at the end of December 2025 totaled about $969 million, with another $1.5 billion in short-term securities. Notably, the company repurchased roughly $927 million of stock in 2025, enhancing shareholder returns.

CEO Bill Ready emphasized Pinterest’s strategic evolution. Ready highlighted record engagement, with more than 80 billion monthly searches on the platform, and pointed to AI and commerce as central growth drivers. “AI is changing how people discover […] We are not satisfied with our Q4 revenue performance and believe it does not reflect what Pinterest can deliver over time,” he said during the earnings call, signaling both near-term caution and long-term confidence.

In terms of guidance, Pinterest forecast Q1 2026 revenue of $951 million to $971 million. For 2026, analysts are currently modeling revenue of about $4.75 billion and EPS of around $0.62. These estimates have edged lower since the Q4 call, reflecting a more cautious outlook on digital advertising demand.

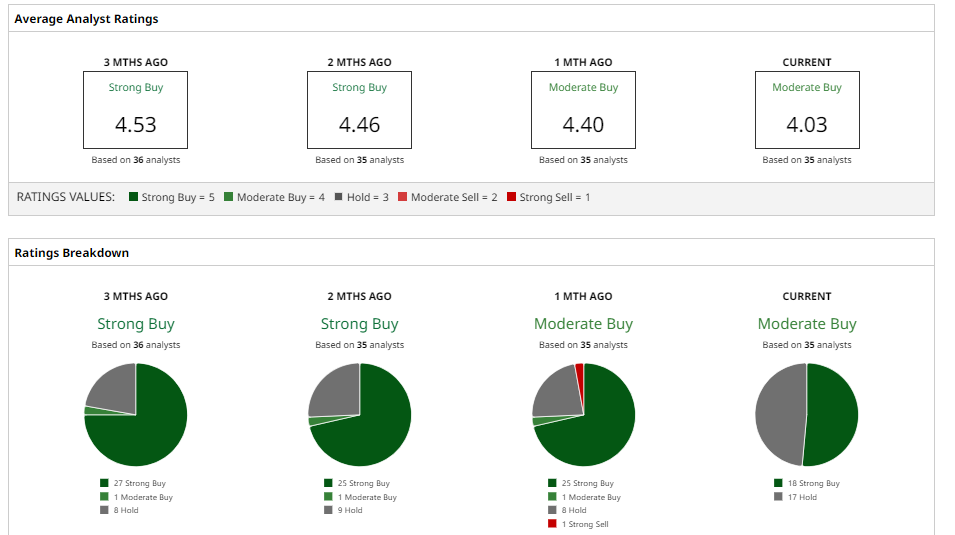

What Do Analysts Think of PINS Stock?

Wall Street analysts have a consensus "Moderate Buy" rating on Pinterest, with a 12-month average price target of $24.42 suggesting potential upside of roughly 37% from here.

Separately, some bullish firms point to the company’s growth and unique user base, while others caution on valuation and margin pressure. In 2026, a number of firms revised their outlooks on PINS stock, including Morgan Stanley, which maintained an “Overweight” rating and increased its price target to $35 from $32 due to its AI-driven engagement and ad-efficiency gains. Goldman Sachs also retained a “Buy” rating but reduced its target to $23 from $32, citing weaker-than-anticipated revenue.

Barclays, however, reduced its outlook, dropping its target to $25 from $36 and assigning a grade of “Equal Weight.” The firm believes the ad market is becoming a tougher undertaking. Other banks remain cautious, too, with JPMorgan and RBC Capital both reducing their targets to $20 and $17, respectively.

The Bottom line

Pinterest remains a fast-growing niche platform with a unique user base and solid 2025 results, but valuation remains demanding, given modest profitability and the ongoing threat of AI-related risks and regulatory challenges, which could undermine Pinterest's business model. That said, Cathie Wood’s sale of PINS stock reflects Ark Invest’s broader rebalancing rather than a fundamental sell signal. Investors should weigh the company’s continued user and revenue gains and new AI/shopping features against the uncertain ad outlook and premium price. As always with high-growth tech, PINS stock looks fully priced for perfection — any stumble in growth or monetization could disappoint.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)