/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

Nvidia Inc. (NVDA) stock has been flat over the last 3 and 6 months, despite market turmoil. As a result, an unusually large tranche of NVDA puts has traded at a 17.6% lower strike price. Investors love the 6.38% short-put play yield over the next 7 months.

NVDA closed at $181.93 on Tuesday, March 16, well below its pre-earnings Feb. 25 peak of $195.56, but up from a recent low of $171.88 on Feb. 5. But Barchart shows that NVDA stock has been relatively flat over the last 6 months.

Shorting OTM NVDA Works

I discussed Nvidia's underlying value and ways to play it in two recent Barchart articles. In a Feb 27 Barchart article, I showed how NVDA could be worth between $263 and $295, +44.5% to 62% more ("Nvidia's Massive Free Cash Flow Margins Could Push NVDA Stock 45% Higher.")

And, in a follow-up March 1 Barchart article, I showed that it makes sense to sell short out-of-the-money (OTM) put options in one-month expiry periods. I also discussed buying in-the-money (ITM) longer-dated calls ("Nvidia Stock May Be Oversold - What is the Best NVDA Play?)

So far, that has worked out. For example, the April 2 expiry $165.00 put option premium has fallen from $5.15 to just $1.25 as of March 17, with just 16 days left.

This put contract is likely to expire worthless, allowing the investor to keep the whole 3.12% yield for one month (i.e., $5.15/$165.00). It turns out that some investors are now looking to short longer-dated put option contracts.

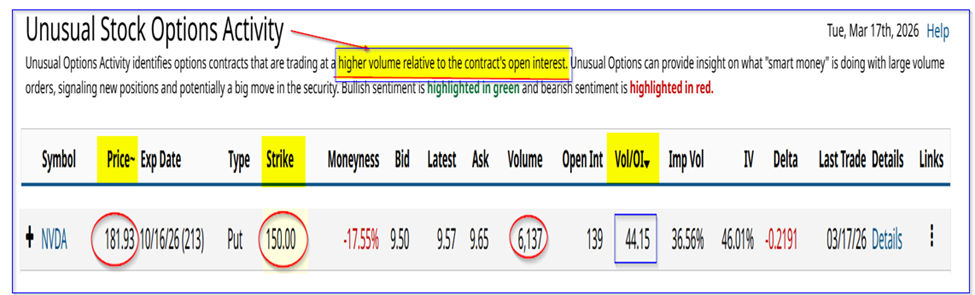

Unusual Short-Put NVDA Volume for 7 Month Contracts

This can be seen in the Barchart Unusual Stock Options Activity Report. It shows that over 6,100 Oct. 16 expiry put contracts have traded at the $150.00 strike price. That strike price is 17.6% lower than Tuesday's close, and the period is 213 days away.

The premium received at the midpoint by short-sellers is $9.57, giving the short-sellers of these puts a whopping 6.38% yield over the next 7 months (i.e., $9.57/$150.00 = 0.0638).

This means that an investor who secures $15,000 with their brokerage firm can immediately collect $957 in their account by entering an order to “Sell to Open” this contract.

Moreover, the institutional investors who are likely the initiators of this trade as a short-put play have a much lower potential breakeven buy-in point:

$150.00 - $9.57 = $140.43 breakeven

That's over $40 lower than today's price, i.e., -22.8% below $181.93, and would only occur if NVDA fell to $150.00 or lower on or before Oct. 16.

In effect, it sets an attractive value entry point and allows the potential investor to make income while waiting. Existing NVDA investors can also make income on their holdings.

For example, over the next 7 months, a 6.38% yield collected now works out to almost a 1% monthly yield:

6.38% / 7 = 0.911% per month, or 91% of 1% monthly

This assumes NVDA stock remains above $150.00 until Oct. 16. However, even if it doesn't, the lower breakeven allows existing investors to lower their average buy-in cost, if the put option contract is assigned.

The bottom line is that this out-of-the-money (OTM) short-put play is a great investment for potential Nvidia investors and existing shareholders as well.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)