Tariff uncertainty refuses to die down, and just when it seemed that the U.S. was moving forward on trade deals with key trading partners, the Supreme Court voided President Donald Trump’s tariffs. President Trump, who has made tariffs a central focus of his economic and foreign policy, responded by imposing a new 10% global tariff, which he soon raised to 15%.

U.S. stocks fell yesterday, Feb. 23, although the decline wasn’t as severe as the one last year, when Trump’s sweeping “Liberation Day” tariffs spooked markets. Meanwhile, one asset class that has been shining under Trump’s presidency is gold, and the precious metal rose to a multi-week high yesterday amid all the uncertainty.

Gold Has Soared During Trump's Second Term

When Trump took office again last year, I had listed the SPDR Gold Trust ETF (GLD) as one of the two ETFs to buy in his second presidency. Gold has soared to record highs under Trump’s presidency, and to be honest, the pace of rise has taken me by surprise.

Gold mining stocks have fared even better, which is again not surprising as they are a leveraged play on the precious metal. Specifically, AngloGold Ashanti (AU) stock is up 45% for the year and has almost quadrupled over the 52 weeks.

Gold mining companies are using their free cash flows to reward shareholders in the form of higher dividends and share buybacks. AU has one of the most generous dividend policies in the gold mining space, and its trailing dividend yield is nearly 3%. While usually I would mention the forward dividend yield, in AU’s case, we don’t have a watertight forward dividend yield, as the payouts are variable and linked to the free cash flows.

AU intends to pay half of its free cash flows to investors as dividends and periodically tops up the regular quarterly dividend of 12.5 cents with true-up payments to reach its payout targets. AU was making these true-up payments annually, but last year it made a departure from this policy and announced true-up dividend distributions alongside its quarterly earnings beginning Q2 2025.

AngloGold Overshot Its Dividend Payout Targets Last Year

During the Q4 2025 earnings call, in response to a question over whether the company would be doing quarterly true-ups, AngloGold Ashanti CEO Alberto Calderon said that while the policy is still to do annual true-ups, the board will decide every quarter.

Last year, AU paid $1.8 billion in dividends, and the payout was significantly higher than the target as the company rewarded shareholders amid soaring gold prices. AU holds more cash and equivalents on its balance sheet than the debt it owes and had an adjusted net cash of $879 million at the end of 2025. In comparison, the company had an adjusted net debt of $567 million at the end of 2024, but thanks to the nearly $3 billion in free cash flows last year, it was not only able to pay record dividends but also further strengthen its balance sheet.

While the management did not explicitly say so, if gold prices continue to stay at these levels, the board might announce a higher payout in 2026 and continue with the quarterly true-ups.

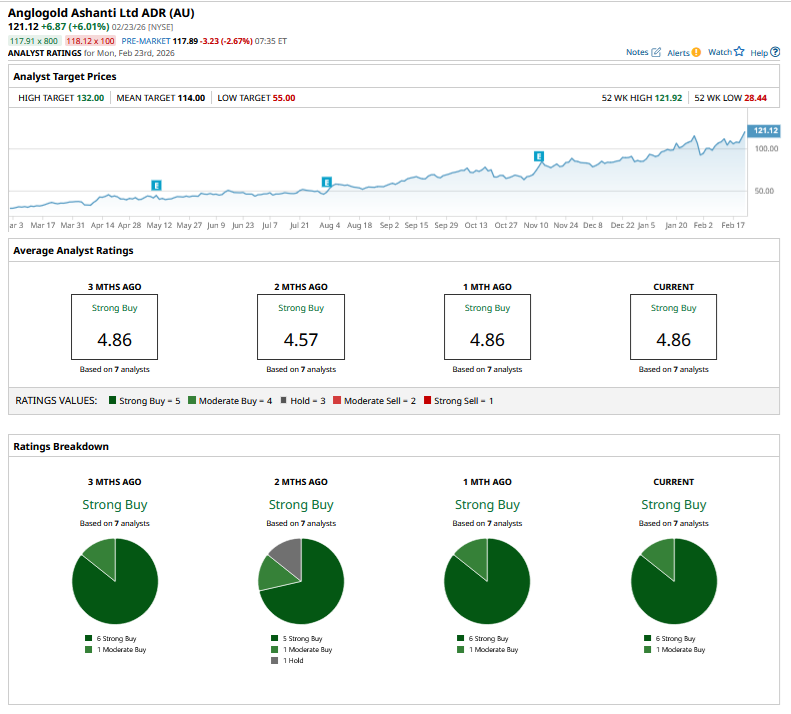

AU Stock Forecast

AU has a consensus rating of “Strong Buy” from the seven analysts polled by Barchart, but the stock has run ahead of its mean target price of $114. Even the Street-high target price of $132 is just about 9% higher than current price levels. Such anomalies are not uncommon when a stock goes parabolic, as AU has been for the last few months, as analysts' actions often lag the actual price action.

AU stock trades at a forward enterprise value to earnings before interest, tax, depreciation, and amortization (EV-to-EBITDA) multiple of 7.19x, which is similar to Newmont Mining (NEM), even as it trades at a significant discount to Agnico Eagle Mines (AEM).

AU has historically traded at a discount to some of the other gold miners amid concerns over its mining portfolio and relatively weak balance sheet. The company has, however, been addressing these issues and now has an impeccable balance sheet.

It has been optimizing its portfolio and sold stakes in some of its Tier 2 assets, which by definition have higher per-unit costs, while adding Tier 1 assets. Last year, 70% of AngloGold Ashanti’s production and 80% of reserves were from Tier 1 assets. The ratio of Tier 1 assets in its production mix has increased gradually as Obuasi has ramped up operations and could increase further as the production from that mine scales up in the coming years.

Overall, with gold remaining the pre-eminent “Trump trade” and a play on global uncertainty and geopolitical tensions, I find AngloGold Ashanti a good way to play the theme, and the generous dividend is only the icing on the cake.

On the date of publication, Mohit Oberoi had a position in: AU. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)