/Amazon%20pickup%20%26%20returns%20building%20by%20Bryan%20Angelo%20via%20Unsplash.jpg)

Big companies are often judged by market capitalization or headline growth, but revenue — the raw cash a business pulls in — is a blunt and revealing metric of scale. When a company starts to out-earn rivals at that scale, it can signal a structural shift in how industries and profits are being made.

In this backdrop, Amazon’s (AMZN) latest milestone grabbed headlines, as the company’s 2025 sales were about $717 billion, surpassing Walmart’s (WMT) $713 billion. This makes Amazon the top company by revenue in the Fortune 500, ending Walmart’s 13-year run.

That isn’t just a vanity stat. Much of Amazon’s lift comes from high-margin, rapidly expanding businesses beyond retail. Amazon Web Services (AWS) and advertising continue to drive outsized growth and profitability, giving Amazon a fundamentally different revenue mix than a store-led player.

Still, milestones come with caveats. Management’s big push into AI infrastructure, including a sizable capex program for data centers, has investors weighing near-term spending against long-term optionality, a dynamic that has pressured AMZN stock in the short term.

AWS Partnerships and Custom AI Chips Take Center Stage

Founded in 1994 by Jeff Bezos, Amazon has become unlike any other retailer. It dominates U.S. e-commerce with roughly 40% of online sales and has more than 180 million Americans subscribed to Prime. Beyond retail, Amazon is a leader in cloud, streaming media, advertising and logistics. This mix of businesses, from Alexa to AWS, gives the company unmatched scale and a diverse set of growth drivers.

Amazon is aggressively betting on AI. In late January 2026, reports surfaced that CEO Andy Jassy is leading talks to invest $50 billion in OpenAI. That would give AWS even closer ties to the ChatGPT-maker. Amazon is already OpenAI’s cloud partner, having invested billions in Anthropic.

Separately, Amazon announced a $35 billion investment in India by 2030 to boost AI, cloud, and exports. In the fourth quarter, Amazon also noted new AWS partnerships with OpenAI, Visa (V), BlackRock (BLK), the NBA and more, as well as the launch of AI chips and services. Bullish investors believe deeper AI integration could unlock fresh revenue streams for AWS and help cement Amazon’s leadership in enterprise AI services.

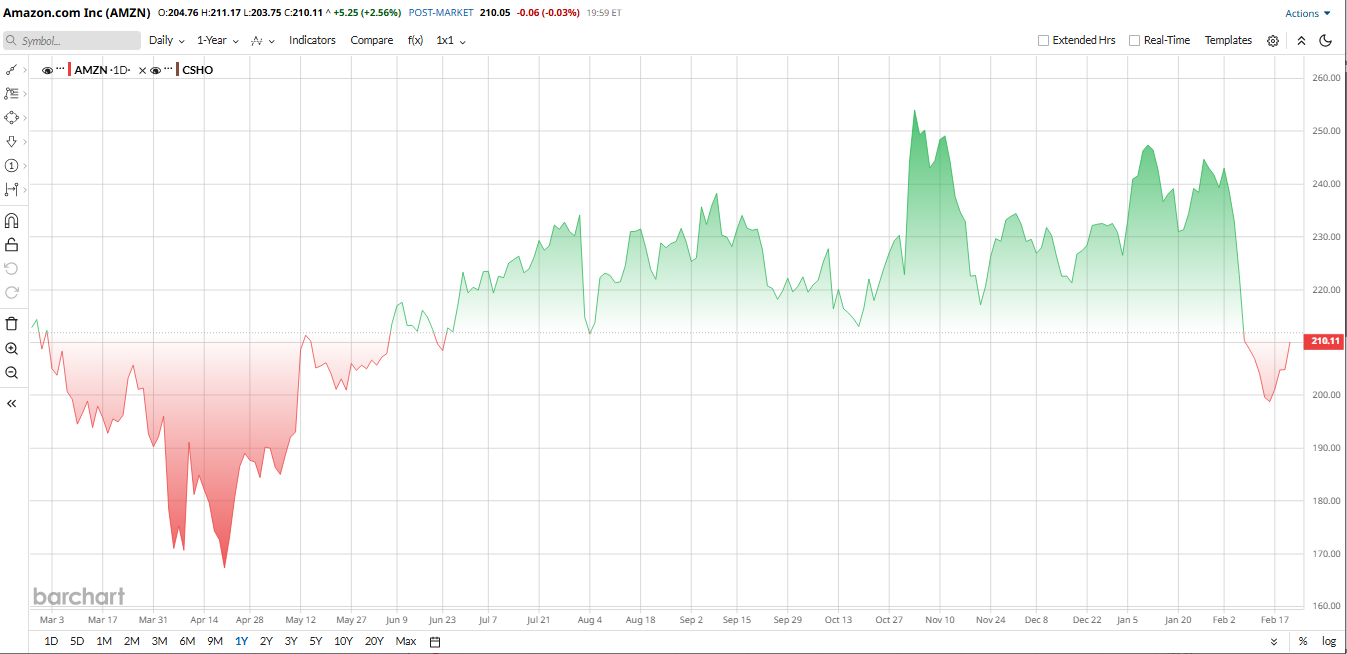

After a huge 44% jump in 2024, AMZN stock lagged in 2025. Shares are down about 1% over the past 52 weeks, trailing the broader market. Investors have been wary of Amazon’s heavy capital spending (AI and data centers) and mixed retail demand, which has kept returns modest.

Despite the underperformance, Amazon looks pricey on some metrics. Its trailing price-to-earnings (P/E) ratio is around 28.6 times, well above the 19 times median for broadline retail peers. Amazon's price-to-sales (P/S) multiple is roughly 3 times, also far above the 1.6 times industry norm. In short, AMZN stock carries a premium valuation. Bulls argue this is justified by faster growth, like with AWS and advertising, which are booming. But the bears says that on a forward EV/EBITDA basis, Amazon isn’t cheap either.

What Top of the Fortune 500 Means for AMZN

Amazon reporting $717 billion in sales versus Walmart’s $713 billion in 2025 is mostly symbolic, but it underscores the firm's rapid expansion. Fortune notes that Amazon's growth has far outstripped Walmart’s growth in recent years, with the company seeing a “cumulative annual growth rate about three times that of Walmart” between 2018 and 2025. Now with a market capitalization of around $2.2 trillion, Amazon is among the largest U.S. companies behind Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL) and Nvidia (NVDA).

For investors, the topline leadership is a confidence boost — it shows that Amazon’s Prime, retail, and AWS strategies are scaling massively. In practice, stock gains will still depend on profit and free cash flow, but this milestone reinforces the bull case that Amazon’s franchise continues to strengthen.

Amazon Beats Q4 Earnings Estimates

Amazon’s fourth-quarter performance was strong. Revenue jumped 14% to $213.4 billion, comfortably beating Wall Street’s $211 billion consensus. Every segment grew by about single to double digits during the quarter.

EPS was $1.95 versus $1.86 a year ago, a small year-over-year (YOY) rise that slightly beat expectations. In fact, Amazon has now beaten revenue forecasts for several quarters in a row. Q4 gross margin widened, helped by higher-margin AWS and ads. Amazon said advertising revenue grew 22% in Q4, while one-off deals helped margins, store margin was “brisk,” and AWS margins hit 35%.

CFO Brian Olsavsky noted that operating cash flow jumped 20% to $139.5 billion for the year, but free cash flow plunged to about $11.2 billion, down from $38.2 billion as capital spending surged. Amazon invested $50 billion more in property and equipment (partly for AI/data centers) and plans to spend about $200 billion in 2026.

Looking ahead, management reiterated solid Q1 guidance. Q1 2026 revenue is forecast around $173.5 billion to 178.5 billion, about by 11% to 15% YOY, implying another busy holiday sequence. CEO Andy Jassy’s remarks were upbeat. Jassy touted AWS’s 24% growth as the fastest in years and expects continued momentum as new data centers come online. Overall, Amazon’s results beat sales forecasts and showed broad-based expansion across cloud, ads, and retail, even if near-term profits dip due to reinvestment.

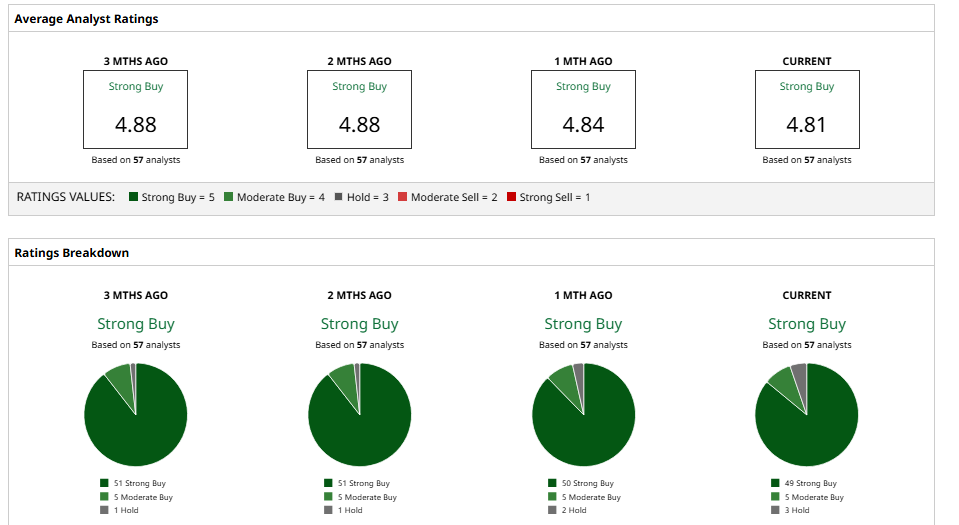

What Do Analysts Think of AMZN Stock?

Wall Street’s view on Amazon is mostly bullish. Morgan Stanley recently kept AMZN stock as its top pick, reiterating an “Overweight” rating and $300 price target. Goldman Sachs also maintained a “Buy” rating on AMZN, although the firm trimmed its target slightly to $280, noting that AWS margins and holiday sales beat expectations.

Meanwhile, Jefferies raised its price target to $300 from $275, citing accelerating cloud growth and attractive EV/EBITDA on 2026 forecasts.

In summation, most analysts see Amazon’s pullback as a buying opportunity. The consensus 12-month price target is $284.75, implying roughly 35% potential upside from current levels. The common theme is that Amazon’s unique scale in e-commerce and AI-driven cloud gives it room to run once investment headwinds settle.

The Bottom Line on Amazon Stock

Amazon's new status as the leading seller in the world is a headline that predominantly demonstrates the strength of its business model. Amazon is attracting positive projections with record sales and cloud growth that's picking up the pace. Current investors in the company will pay attention to the question of whether this scale can eventually translate into bigger profits, but the large-scale picture already gives them the confidence in the long-term narrative.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)