Cincinnati, Ohio-based The Procter & Gamble Company (PG) manufactures and markets consumer products. With a market cap of $383.9 billion, the company’s product portfolio comprises conditioners, shampoos, blades and razors, toothbrushes, toothpastes, dish-washing liquids, detergents, surface cleaners and air fresheners, and more.

Companies worth $200 billion or more are generally described as “mega-cap stocks,” and PG definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the household & personal products industry. PG's 20+ billion-dollar brands showcase its market leadership and consumer trust. Strong brand presence across categories like Tide and Pampers drives shelf space and mindshare, fueled by strategic marketing and innovation.

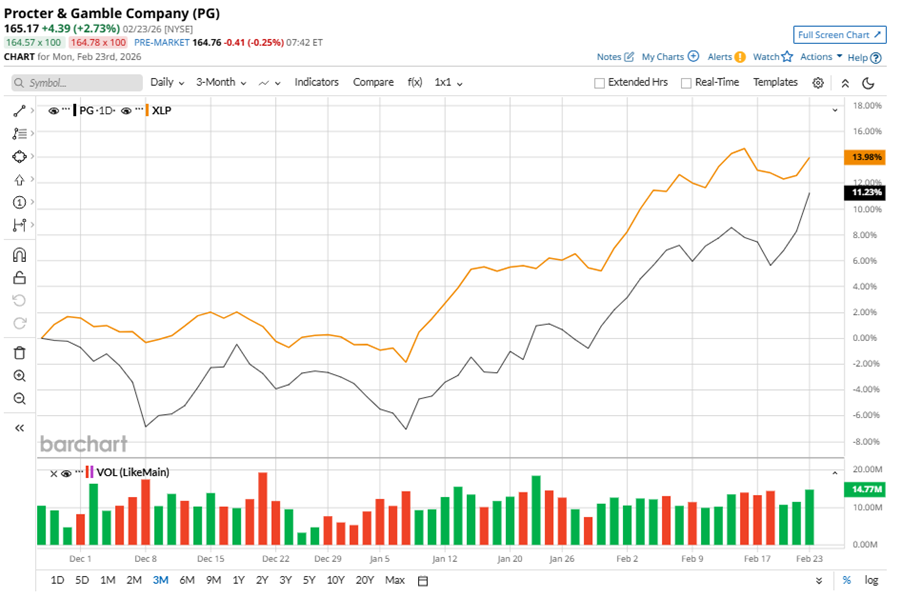

Despite its notable strength, PG has slipped 8.2% from its 52-week high of $179.99, achieved on Mar. 4, 2025. Over the past three months, PG stock gained 9.4%, underperforming the Consumer Staples Select Sector SPDR Fund’s (XLP) 14.2% gains during the same time frame.

Shares of PG rose 15.3% in 2026, outperforming XLP’s YTD gains of 8.3%, while the stock dipped 3% over the past 52 weeks, underperforming XLP’s 14.5% returns over the same time frame.

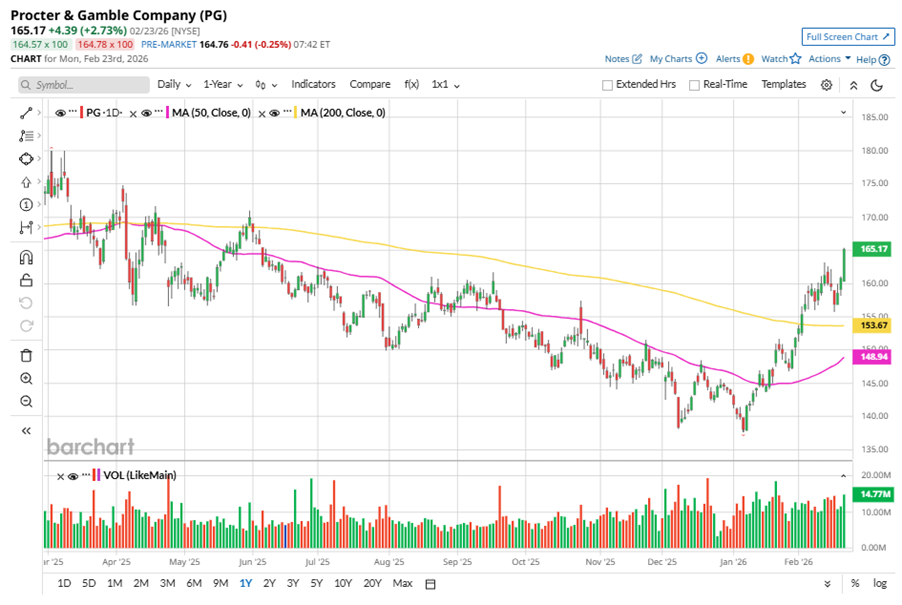

To confirm the bullish trend, PG has been trading above its 50-day moving average since mid-January, and it has been trading above its 200-day moving average since early February.

On Jan. 22, PG shares closed up more than 2% after reporting its Q2 results. Its adjusted EPS of $1.88 beat Wall Street expectations of $1.87. The company’s revenue was $22.2 billion, falling short of Wall Street forecasts of $22.3 billion. PG expects full-year adjusted EPS in the range of $6.83 to $7.09.

In the competitive arena of household & personal products, Colgate-Palmolive Company (CL) has taken the lead over PG, showing resilience with an 8.5% uptick over the past 52 weeks and 22.9% YTD gains.

Wall Street analysts are reasonably bullish on PG’s prospects. The stock has a consensus “Moderate Buy” rating from the 25 analysts covering it, and the mean price target of $168.36 suggests a potential upside of 1.9% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)