/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)

In 2025, Robinhood Markets (HOOD) wasn’t just another fintech stock; it was one of the standout performers on Wall Street. After years of volatility and skepticism following its 2021 IPO, Robinhood’s shares soared meteorically over the year, amid renewed optimism.

The S&P 500 Index ($SPX) financials sector has kept pace with the broader market and ranks as the fourth-best performing sector. Within this group, Robinhood Markets topped the list with 215% gains year-to-date (YTD). Behind the headline gains were improving fundamentals that transformed HOOD from a meme-era darling into a serious fintech contender in the eyes of many investors.

However, with broader market uncertainties on the horizon, let’s analyze whether this red-hot run still has room to run or if caution is warranted.

About Robinhood Stock

Headquartered in Menlo Park, California, financial services company Robinhood is known for its mobile-first brokerage platform that democratizes access to investing by offering commission-free trades of stocks, ETFs, options, cryptocurrencies and more to retail investors. The company has grown into a large-cap stock with a market cap of around $106.2 billion.

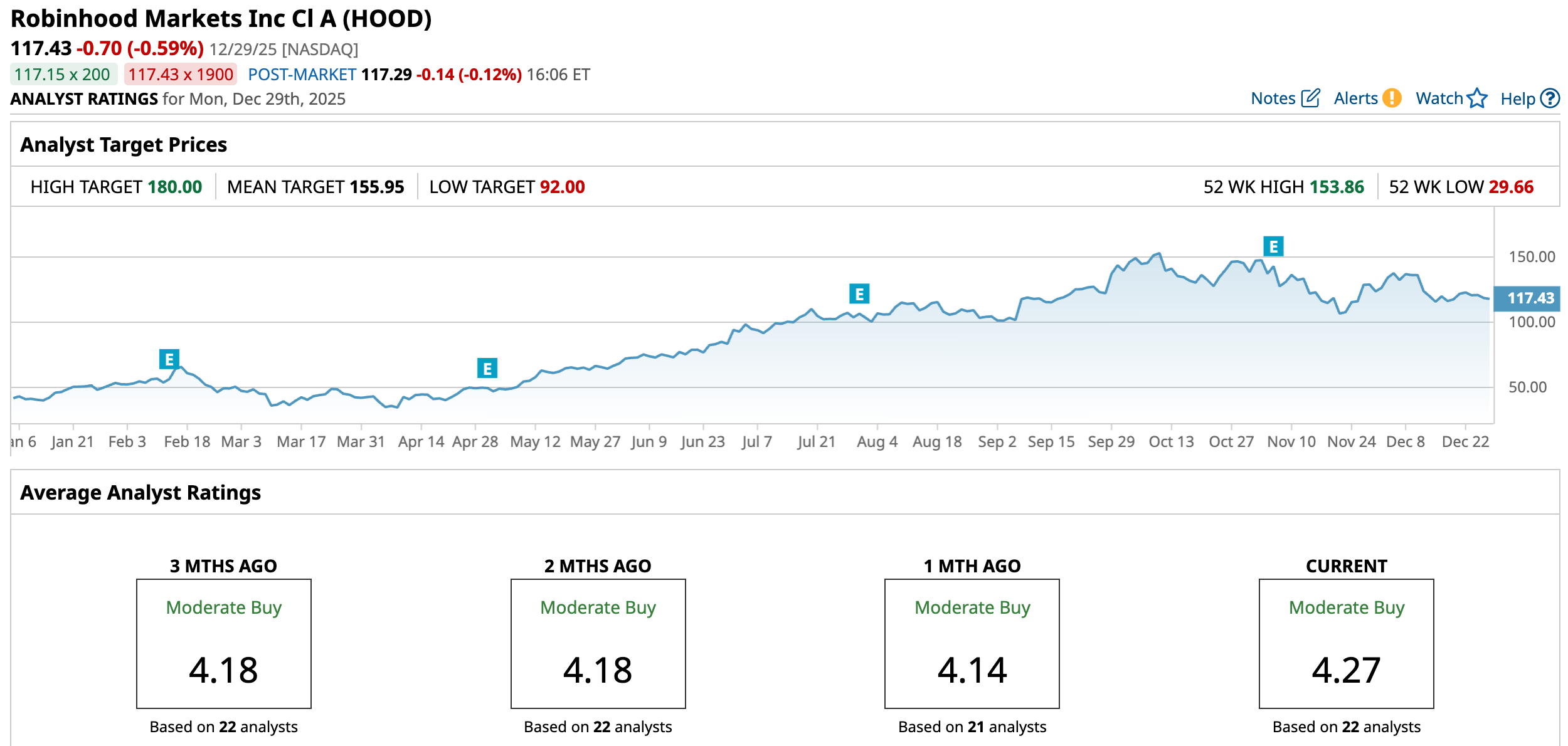

In 2025, Robinhood’s stock price delivered a standout performance that captured investors’ attention, turning one of the most closely watched fintech names into a top market performer. The stock has registered a peak of $153.86 on Oct. 6, while the total past 52-week return stands at 200.21%, underscoring strong upward momentum. And, its 215% YTD gain is far outpacing the broader S&P 500 17.48% gains.

The stock’s rally reflected renewed investor confidence tied to booming trading activity, expanding revenue streams, and major milestones like its inclusion in the S&P 500 and rapid subscriber growth. While the stock is down 31.2% from its 52-week high, it is one of the most compelling stories in the financial sector this year.

The stock is currently trading at 60.48 times forward earnings, which is higher than the sector median.

Strong Q3 Results

Robinhood released its third-quarter 2025 earnings on Nov. 5, reporting one of its strongest quarters in company history and substantially outperforming year-ago results. The company posted record total net revenues of $1.3 billion, doubling with a 100% year-over-year (YOY) rise. This remarkable expansion was driven by broad-based growth across Robinhood’s diversified revenue streams, including transaction-based revenue, net interest income, and subscription services.

Transaction-based revenues alone jumped about 129% YOY to $730 million, with crypto revenues up more than 300% and equities and options also showing strong gains. Net interest revenues climbed 66% from the prior year to $456 million, reflecting growth in interest-earning assets and securities-lending activity. Other revenue categories roughly doubled YOY, driven by Robinhood Gold subscriptions.

Profitability improved sharply too, with net income soaring 271% YOY to $556 million and EPS increasing about 259% to $0.61, comfortably above analyst expectations.

Funded customers expanded by roughly 10% to 26.8 million, while total platform assets surged significantly to about $333 billion, with net deposits hitting $20.4 billion in the quarter.

Also, the company provided preliminary November 2025 operating data. Funded customers stood at about 26.9 million, up by 2.1 million YOY. Total platform assets were around $325 billion, up 67% compared with November 2024, while net deposits reached around $7.1 billion, supporting continued asset growth.

Analysts tracking Robinhood project the company’s EPS to climb 82.6% YOY to $1.99 in fiscal 2025 and grow another 20.6% to $2.40 in fiscal 2026.

What Do Analysts Expect for Robinhood Stock?

Earlier this month, Mizuho reaffirmed its “Outperform” rating and $172 price target on HOOD, citing accelerating momentum in its prediction markets business.

Meanwhile, Cantor Fitzgerald maintained an “Overweight” rating, but lowered its price target to $152 from $155.

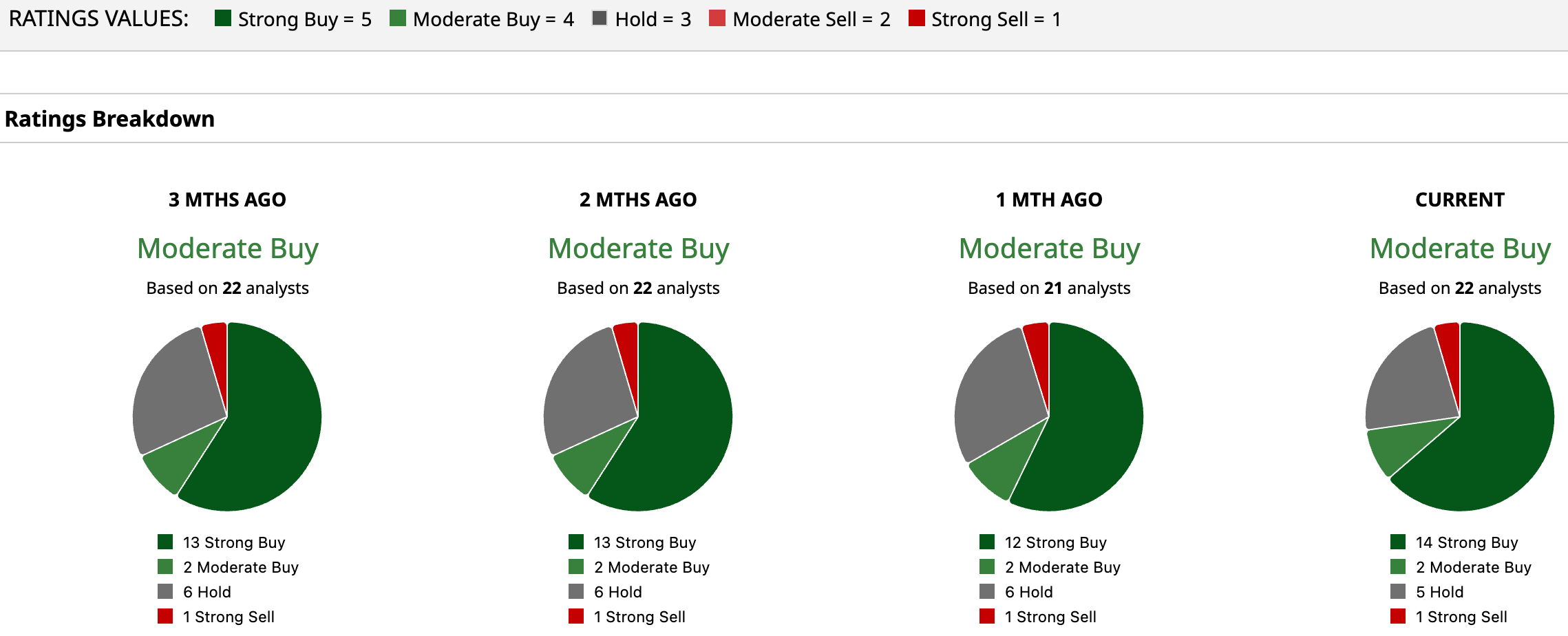

Wall Street’s outlook on Robinhood remains fairly optimistic, with the stock carrying a consensus “Moderate Buy” rating. Of the 22 analysts currently covering the stock, 14 rate it a “Strong Buy,” two assign a “Moderate Buy,” five analysts recommend “Hold,” and just one carries a “Strong Sell” rating.

The average price target of $155.95 implies roughly 33.12% upside from current levels, suggesting continued momentum. Plus, the most bullish forecast calls for $180, which indicates a potential rally of as much as 53.28% from here.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)