Vulcan Materials Company (VMC), headquartered in Birmingham, Alabama, produces and supplies construction aggregates. Valued at $37 billion by market cap, the company’s principal product lines are aggregates, asphalt mix, concrete, and cement.

Shares of the largest producer of construction aggregates have underperformed the broader market over the past year. VMC has gained 1.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 12.3%. In 2025, VMC stock is up 9.6%, falling behind the SPX’s 12.5% rise on a YTD basis.

Narrowing the focus, VMC’s underperformance is apparent compared to the Invesco Building & Construction ETF (PKB). The exchange-traded fund has gained about 9.1% over the past year and 20% gains on a YTD basis.

On Oct. 30, Vulcan Materials shares dipped 1.7% after the company released its third-quarter earnings. The company posted $2.29 billion in revenue, up 14.4% year over year, with adjusted EBITDA rising 26.5% to roughly $735 million as margins expanded. Aggregates shipments climbed around 12% to 64.7 tons, supported by robust demand from public infrastructure projects, while pricing improved and unit cash costs declined. Management highlighted solid operational performance and reaffirmed full-year guidance, projecting adjusted EBITDA between $2.35 billion and $2.45 billion.

For the current fiscal year, ending in December, analysts expect VMC’s EPS to grow 11.8% to $8.42 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on one other occasion.

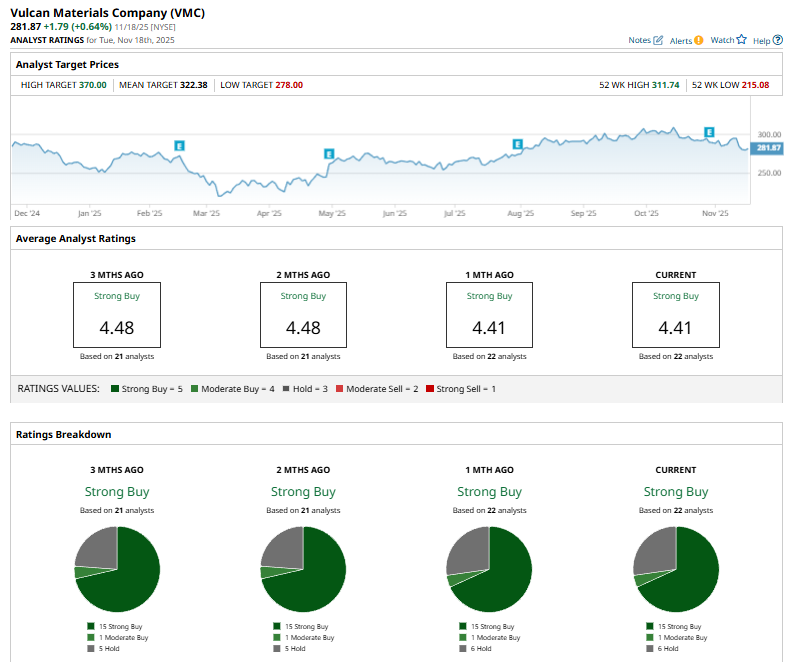

Among the 22 analysts covering VMC stock, the consensus is a “Strong Buy.” That’s based on 15 “Strong Buy” ratings, one “Moderate Buy,” and six “Holds.”

The configuration has been consistent over the past three months.

DA Davidson analyst Brent Thielman raised his price target on Vulcan Materials to $330 from $315 on Nov. 4 and reiterated a “Buy” rating following the company’s Q3 earnings beat. He noted that profitability remains strong, and while the surge in Q3 volumes shouldn't be viewed as a sustained trend given current market conditions, he still sees earnings growth into FY26 as achievable, supported by disciplined costs and incremental aggregates pricing.

The mean price target of $322.38 represents a 14.4% premium over VMC’s current prices. The Street-high price target of $370 suggests an upside potential of 31.3%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)