New York-based Omnicom Group Inc. (OMC) offers advertising, marketing, and corporate communications services. With a market cap of $15 billion, the company’s agencies, which operate in major markets around the world, provide a comprehensive range of services, including traditional media advertising, customer relationship management (CRM), public relations, and specialty communications. The global leader in marketing communications is expected to announce its fiscal third-quarter earnings for 2025 on Tuesday, Oct. 21.

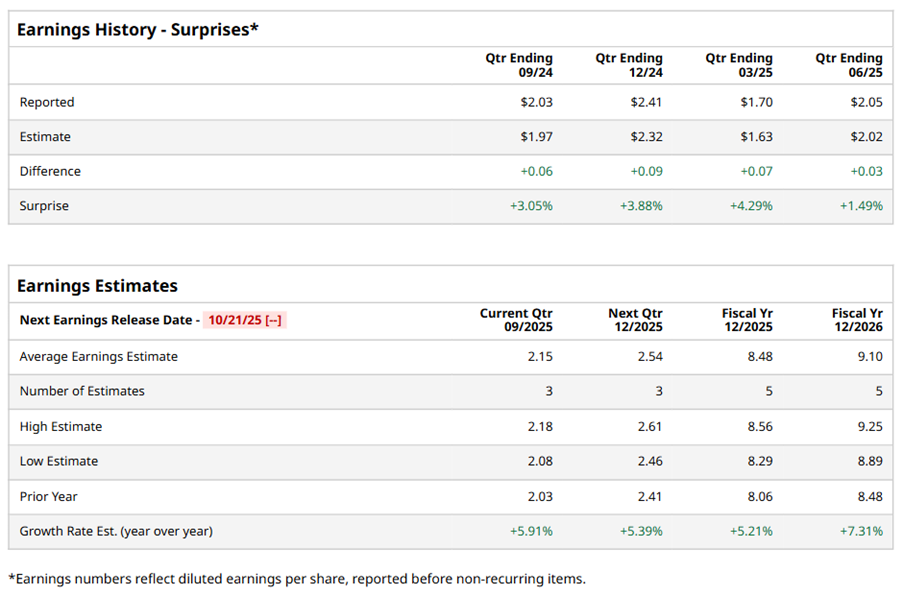

Ahead of the event, analysts expect OMC to report a profit of $2.15 per share on a diluted basis, up 5.9% from $2.03 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect OMC to report EPS of $8.48, up 5.2% from $8.06 in fiscal 2024. Its EPS is expected to rise 7.3% year-over-year to $9.10 in fiscal 2026.

OMC stock has considerably underperformed the S&P 500 Index’s ($SPX) 17.6% gains over the past 52 weeks, with shares down 24.7% during this period. Similarly, it considerably lagged behind the Communication Services Select Sector SPDR ETF’s (XLC) 29.1% gains over the same time frame.

On Jul. 15, OMC shares closed down by 2.6% after reporting its Q2 results. Its revenue stood at $4 billion, up 4.2% year-over-year. The company’s adjusted EPS increased 5.1% year-over-year to $2.05.

Analysts’ consensus opinion on OMC stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 11 analysts covering the stock, five advise a “Strong Buy” rating, and six give a “Hold.” OMC’s average analyst price target is $93.62, indicating a potential upside of 21.8% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)